David Vs Goliath Challenge – how a $25B market cap stock can beat a $202B market cap stock?

Both Companies show strong customer loyalty, but only one evolves in an Oligopoly

One company is trading at a 10% discount, the other at a 10% premium

Last week, I wrote a stock analysis for Seeking Alpha on Verizon (VZ), you can read the analysis here. While I was writing this article, I kept comparing this telecom giant vs one of my holdings; Telus Corporation (T.To or TU on the NYSE). While both companies get the bulk of their income from mobile services and both companies pay healthy dividend, VZ is worth 8 times the market capitalization of TU. Still, I prefer the “small cap” even if the dividend is lower. Since Telus could be very attractive for US investors as it trades on the NYSE, I thought it was worth making a real comparison between both companies.

Business Model Comparison

Verizon

Verizon shows an impressive profile with 109 million retail customers and covers more than 95% of the US population. What is even better than having lots of customers? Keeping them! Verizon has earned very high customer loyalty throughout the years and is known for great customer service. Unfortunately, its strength is also in the middle of one of its main weakness; the cost of maintaining such a high quality network. Last year, VZ spent $10B alone to maintain this network. This represents 14% of their sales. While the company generate lots of cash flow, a good chunk is used up in operating this great business model.

As technology evolves quickly, VZ also invests in other avenues. It has recently bought AOL (AOL) for 4.4 billion. The main idea behind this transaction is to integrate AOL’s advertising platform into the new VZ video mobile service. Many says it’s a risky move as VZ bought a declining giant to enter in the arena with many others; Google (GOOG) and Facebook (FB), the masters of online advertising.

Telus

Telus has been providing communication services for over 100 years. The business has evolved greatly over the past 20 years. We can now divide Telus business model into two segments:

Wireless services

This is now the bread and butter of the company. Telus is known for keeping its clients and shows a high profit margin per customer with a growing client base (up 3.8% to 8.1 million), Telus wireless services assure an interesting growth for the future. They also cover all Canada’s important part:

Wireline Segment:

Telus not only provides wireline phone services but also internet connection and TV cable services. While the wireline phone business is slowing down, Telus compensates by adding other wireline services to its wireless customers. This explains why the internet and TV services are growing this fast.

Telus is “protected” by a strong oligopoly in Canada. While the Government has many times expressed the desire to open the door to other competitors, many of them have decided to ignore the Canadian market knowing it would cost lots of money to break the oligopoly. VZ finally decided to ignore the Canadian opportunity in 2013 and bought back its shares of Verizon Wireless from Vodafone (VOD) instead.

In other words; Telus is still playing against players of its own size while Verizon has to compete with much bigger players on its playground.

Verizon & Telus vs 4 Dividend Investing Principles

Throughout my investing years, I’ve read much financial research and learned from my own experience. In order to build a solid dividend growth portfolio, I came up with 4 dividend investing rules being part of my 7 investing principles. I will use my 4 dividend investing rules to compare both companies. In order to compare apples to apples, I’ve used TU stats instead of T.TO. All data is coming from Ycharts.

Principle #1 High Dividend Yield Doesn’t Equal High Returns

It is well known that high dividend yield stocks often provide smaller growth perspectives. After all, if a company pays a high yield, it’s not a free lunch; there is something behind it. Financial research has proven the 1st quartile dividend yield stocks show smaller returns than the 2nd dividend yield quartile stocks. Let’s take a look at how both companies yield over the past 10 years:

As you can see, VZ is a better dividend payer than Telus. However, this also leads me to think that VZ is less likely to perform on the stock market over time. You can see how both stock prices have evolved over the same period:

Since 2009, there is a net advantage for Telus. Let’s dig deeper to see why the Telus stock grew twice as fast as VZ.

Principle #2: If There is One Metric; It’s Called Dividend Growth

My favorite metric to analyze any company is and will always be dividend growth. The reason is simple; a company constantly increasing its dividend must first generate growing sales and expects growing earnings. If both conditions are not met, the company’s dividend payment will be jeopardized and payment growth will quickly stop. Then again, let’s compare both companies:

Telus has shown one of the strongest dividend growth performances over the past ten years on the Canadian stock market. While Verizon’s growth is respectable, Telus is definitely in another league in terms of dividend growth stocks. The stability of the Canadian market doubled with TU’s ability to generate high profits from its customers opens the door for higher dividend payments.

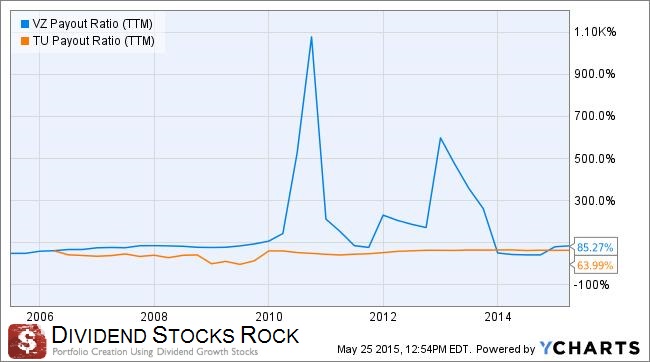

Principle #3: A Dividend Payment Today is Good, A Dividend Guaranteed For the Next 10 Years is Better

Strong dividend growth is appreciated by all dividend investors, but one must remain cautious about the sustainability of the payment. By looking at how a company manages its dividend payout ratio over several years, it will be easy to see if the dividend will remain over time.

Once again, Telus shows greater stability in its dividend payout ratio. It is even more impressive considering how fast TU’s dividend payment grew.

Principle #4: The Foundation of Dividend Growth Stocks Lies in its Business Model

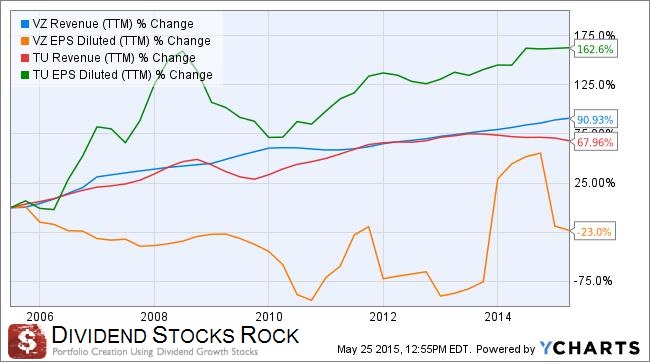

I’ve previously reviewed both companies’ business models. Let’s see how both businesses translate in term of revenues and earnings:

VZ shows a greater ability to increase its revenue but has a hard time generating bigger profits. TU revenues seems to stagnate over the past three years and it will be interesting to see how the company intend to keep growing in the future as earnings won’t continue to rise if revenues are not growing. Still, TU seems the more profitable.

Valuation Model

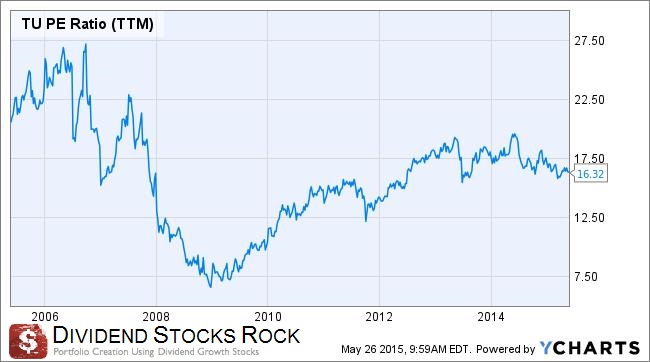

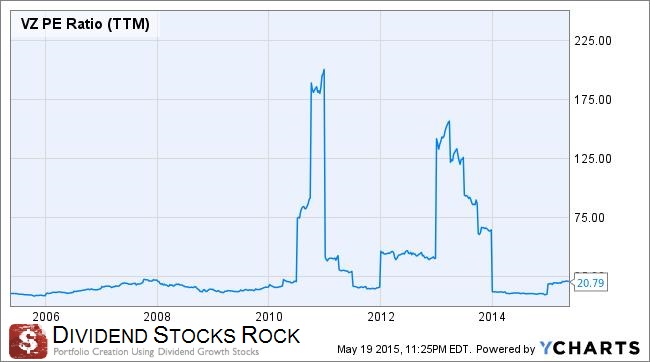

So far, it seems to be that Telus is more appealing than Verizon. However, it doesn’t necessarily mean it’s the right time to buy either stock. This is why we will take a look at how both companies are valued. I will use two techniques to determine the correct valuation. The first one will take a look at the 10 year history PE ratio to see how the market sees both companies and the second technique is the dividend discount model (DDM) to look at the company as a dividend machine. DDM calculations are done with a two stages dividend growth spreadsheet provided in the Dividend Monk Toolkit.

Telus Valuation:

Verizon valuation:

Final Thoughts

After looking at both valuations, Telus doesn’t only show the strongest dividend growth profile, but also the best valuation. TU shares seem to trade on a relatively low PE ratio considering the current market and shows a 10% discount using the Dividend Discount Model. On the opposite hand, VZ shows a hectic PE ratio history doubled with a $10 premium when compared with the DDM valuation. I guess that if the VZ move to buy AOL leads them into another league, earnings will follow and the stock might fly higher. At the moment, I still prefer Telus for more stability even if the cloud of more competition is hanging over its head. Penetrating the Canadian market is a quest by itself and not many foreign companies are willing to do so. It’s also a plus if you buy TU with USD since the Canadian dollar is quite weak recently!

Disclaimer: I hold shares of Telus (T.TO / TU).