In September of 2017, I received slightly over $100K from my former employer which represented the commuted value of my pension plan. I decided to invest 100% of this money into dividend growth stocks.

In September of 2017, I received slightly over $100K from my former employer which represented the commuted value of my pension plan. I decided to invest 100% of this money into dividend growth stocks.

Each month, I publish my results. I don’t do this to brag. I do this to show you it is possible to build a lasting portfolio during an all-time highly valued market. The market will inevitably go down, as it did in 2020. But I continued to enjoy cashing consistent and growing dividends despite that negative market action! And, most importantly, I stayed fully invested in the market and have enjoyed the market recovery in 2020 that has continued into this new year of 2021.

Performance in Review

Let’s start with the numbers as of January 1st, 2021.

- Portfolio value: $192,029.01

- Dividend paid: $3,886.33

- Average yield: 2%

- 2020 performance: +20.3%

- SPY=18.17%, XIU.TO = 5.27%

- Dividend growth: +7.7%

Total return since inception (Sept 2017): 76.75%

Annualized return (since September 2017): 19.15%

SPDR® S&P 500 ETF Trust (SPY) annualized return (since Sept 2017): 15.83%

iShares S&P/TSX 60 ETF (XIU.TO) annualized return (since Sept 2017): 8.04%

Webinar: Where to Invest in 2021?

2,000+ investors saw this webinar already.

- KM: “Amazing webinar! Thanks very much!”

- Cheryl: “With thanks, I’m impressed!”

- Harley: “Thank you for your passion Mike.”

- Roberta: “I’m such a huge fan of DSR! Well done, Mike.”

WATCH THE REPLAY

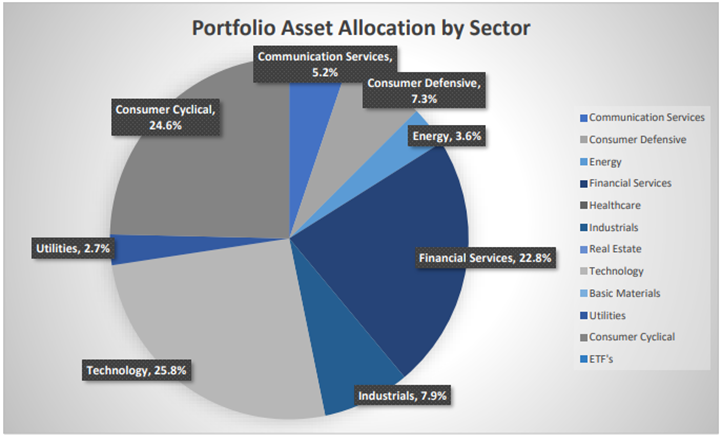

Sector allocation calculated by DSR PRO

2020 has been quite a ride to say the least. I remember back in March when my portfolio dropped to $126,417.48 for my April 6th update (imagine if I had run the numbers on March 23rd!). The portfolio has jumped back about 50% since that date. Here are a few observations on how I got there:

- I never thought my portfolio would drop that much (from $161,419 on January 3rd, 2020).

- At no time was my portfolio value lower than my initial invested amount ($108.6K).

- While I wasn’t smiling back in March, I stayed fully invested during the entire rollercoaster.

- Two of my companies suspended their dividend (Disney (DIS) and CAE (CAE.TO)).

- They both ended the year in positive territory (DIS even outperformed the S&P 500!).

- Two companies didn’t increase their dividend this year (Lazard (LAZ) and Hasbro (HAS).

- I must put them on my watchlist (potential sell ahead).

- My substantial exposure to technology (26%), consumer cyclicals (25%) and financial services (23%) explain a big part of my performance.

- I call this the “Tech stocks rule lesson”.

- On the Canadian side, Intertape Polymer (ITP.TO +57.35%), Magna (MG.TO +33.23%) and Sylogist (SYZ.V +26.20%) are my top performers.

- I only have two losers with Enbridge (ENB.TO -14.98%) and Andrew Peller (ADW.A.TO -9.7%). I averaged down on ADW.A.TO this year.

- I sold Lassonde (LAS.A.TO) in March for a great loss (about 40%).

- Lose as little money as possible and you’ll have good total returns (this is the “Lassonde lesson”)

- On the U.S. side, Apple (AAPL +83.72%, UPS (+46.78%) BlackRock (BLK +44.63%), Microsoft (MSFT +42% and Texas Instruments (TXN +30.6%) are my top performers.

- I only have one loser (Hasbro HAS -7.8%). I bought VF corporation (VFC) during the March collapse. It is now in positive territory in my portfolio (+16% plus dividend).

- I did very few transactions during this mayhem. I trimmed a few Apple shares since it was too big in my portfolio and bought more ADW and VF corporation. Small adjustments that were positive but keeping my AAPL intact would have been even better!

- Managing your sector allocation (and risk exposure) is more important than short term results (I call this the “Apple lesson”).

Since it’s the beginning of the year, I’ll comment on my overall sentiment for each of my holdings.

Let’s start with my CDN portfolio. Numbers are as of January 4th, 2020 (before the bell):

Canadian Portfolio (CAD)

| Company Name | Ticker | Market Value |

| Alimentation Couche-Tard | ATD.B.TO | 7,461.36 |

| Andrew Peller | ADW.A.TO | 6,141.28 |

| National Bank | NA.TO | 5,731.20 |

| Royal Bank | RY.TO | 6,275.40 |

| CAE | CAE.TO | 7,054.00 |

| Enbridge | ENB.TO | 6,554.31 |

| Fortis | FTS.TO | 5,148.00 |

| Intertape Polymer | ITP.TO | 7,242.00 |

| Magna International | MG.TO | 6,307.70 |

| Sylogist | SYZ.V | 4,920.60 |

| Cash | 988.94 | |

| Total | $63,824.79 |

My account shows a variation of +$7,524.40 (+13.36%) since the last income report on November 6th.

I usually discuss what happened in my portfolio in the following section, but since it’s my year-end review, I’ll briefly comment on each stock.

Alimentation Couche-Tard (ATD.B.TO)

With almost half of its profit coming from fuel sales, investors are worried about the electric car (EV) trend. This is greatly exaggerated. In Norway, EV jumped from 0% to 14% of all cars between 2011 and 2019. Fuel sales volume dropped by only 4% during that time. One factor to consider is Couche-Tard’s wide network. The company is adding many of their super charger stations across this network to help the transition. ATD can also count on its experience acquired in Norway to manage the shift in other countries. After what we saw in 2020, I think we have a very good idea of how ATD can do in a world where gasoline sales decline. More about Alimentation Couche-Tard in this video.

Andrew Peller (ADW.A.TO)

Andrew Peller has been quite a disappointment this year. The stock lagged the market (big time) and the company posted mediocre sales growth (2.1% for the first 6 months of their FY2020 vs last year). Andrew Peller finally launched a new e-commerce platform (www.thewinesshops.com) which should help sales growth.

As I’m trying to stay positive, I’d argue that ADW decreased their marketing (advertising, promotions, etc.) to preserve cash in 2020. This resulted in EBIDTA growth of 4.7% for their last quarter and 4.2% for the year. The disappointing sales growth is partially explained by the lack of investment in marketing. Let’s see if ADW can get back into growth mode in 2021. I’ll follow this one closely.

National Bank (NA.TO)

Smaller than the other Canadian banks and not favorably considered by many investors, NA is swift and agile like a ninja. The company counts on strong performances from capital markets and wealth management to grow their business. In the past few years, they have successfully expanded their business into the U.S. and a part of Asia (ABA bank in Cambodia).

Going forward, I think NA will continue to perform well and outperform the other Canadian banks. And, therefore, it remains my number one pick in this industry. More on Canadian banks in this video.

Royal Bank (RY.TO) (RY)

Over the past 5 years, RY did well because of its smaller divisions acting as growth vectors. The insurance, wealth management, and capital markets divisions are pushing RY revenues higher. Those sectors combined now represent over 50% of total revenues. During the COVID-19 pandemic, these are also the same segments helping Royal Bank to stay the course. Royal Bank also made huge efforts into diversifying its activities outside of Canada. While 2020 was a difficult year for banks, RY managed to post a total return of 6.5%. That’s good for the second-best performing bank during the pandemic.

I like that RY is less tied to the Canadian mortgage industry than other big banks. This may limit the impact of a possible housing bubble on RY’s overall business.

CAE (CAE.TO) (CAE)

I can’t believe CAE has recovered from its brutal March drop. The stock traded as high as $41 in February and as low as $14.50 less than a month later. As I have repeatedly mentioned throughout the year, CAE’s strength resides in its engineering team and management’s ability to shift its business toward new opportunities.

The company has thrived thanks to mandatory training for many civilian pilots, solid contracts from the defense industry, and growth coming from its healthcare division (they even signed a contract for 10,000 ventilators!). Once the storm passed, CAE has resumed its acquisition mode this fall by adding many small competitors to its portfolio. CAE is set for a bright future, and it’s a keeper!

Enbridge (ENB.TO) (ENB)

In a few of my latest updates, I’ve discussed the possibility of selling all or part of Enbridge. My investment thesis was built around buying a cheap pipeline (back in 2018) that will thrive in a healthy economy. I was right until we got the pandemic! I’ve recently reviewed the entire company in this Youtube video. This video was recorded after Enbridge released its latest investor presentation.

What has changed my mind? First, their interest in diversifying their business model towards more natural gas and renewable energy. Second, how they intend to grow the distributable cash flow (DCF) going forward (e.g. through various projects that are not necessarily linked to more liquid pipelines). And third, by how they intend to keep their dividend growth streak alive.

Fortis (FTS.TO) (FTS)

When I think of Fortis, it goes like “boring, but amazing”. This utility is well-known for its reliable business model and predictable dividend increases. Did you know Fortis has successfully increased its dividend yearly for the past 47 consecutive years?

With an investing plan of $19.6B between 2021 and 2025, the company’s growth will not stop anytime soon. The best part is that Fortis will find most of its capital funding from its own cash from operations (61%). Management has also confirmed a 6% dividend growth guidance through 2025. More on Fortis in this video.

Intertape Polymer (ITP.TO)

This is another company that made more than one subscriber doubt my sanity. ITP lost more than 50% of its value (from $17 to $7) during the initial pandemic crisis only to finish the year at $24. While part of the ITP business went through a tough time, the tape for e-commerce shipping boxes and food packaging surged.

During their latest quarter, management increased their guidance for 2021. The company improved their free cash flow by 202% for the first nine months of 2020 while adjusted EPS went up by 29%. Oh, and did I mention the 7.5% dividend increase? Intertape Polymer grows through multiple acquisitions. With more cash flow and long-term debt being paid down, you can bet the company will look to make a few moves in the coming years.

Magna International (MG.TO) (MGA)

Magna is not only a dominant player in the car parts manufacturing business, but it is also the only car part maker able to build an entire car from its own parts. The company has been proactive by shifting part of its business into electric cars and hybrids. Magna has signed a partnership with Fisker to provide the framework for platform sharing and manufacturing cooperation. The company has the resources and expertise to support electric car companies as it still supports “classic” car brands.

Sylogist (SYZ.V)

Let’s make it simple for this one: no debt + recurring revenue = dividend growth. This small cap flew under the radar of many analysts as it requires additional research to fully appreciate their business model. For example, many have asked me about the crazy PE ratio of 148 and the incredible payout ratio of 539%. Here’s the full explanation for those phenomena:

The high payout ratio is due to an adjustment they made last year regarding the company’s management compensation (they went from cash bonuses to stock options). The last cash payment generated an important impact on earnings.

The executives agreed to relinquish their current cash bonus entitlement for the one-time cash payment of $12 million. Doing so immediately added, based on annualizing the fiscal 2019 nine-month results, $2.2 million of after-tax cash flow resulting in a 17% improvement in operating cash flow before non-cash working capital adjustments, and improved after tax profitability by 21%. The payment is non-dilutive to shareholders and, on an after-tax basis, is less than 4 times the Company’s annual trailing cash flow associated with the bonus payments. In addition, a higher percentage of cash flow growth will now accrue to shareholders. This transaction will result in a one-time charge to earnings in Q1 of fiscal 2020.

Here’s my US portfolio now. Numbers are as of January 4th, 2020 (before the bell):

U.S. Portfolio (USD)

| Company Name | Ticker | Market Value |

| Apple | AAPL | 12,738.24 |

| BlackRock | BLK | 10,101.56 |

| Disney | DIS | 8,153.10 |

| Gentex | GNTX | 7,973.55 |

| Hasbro | HAS | 4,302.84 |

| Lazard | LAZ | 4,314.60 |

| Microsoft | MSFT | 13,345.20 |

| Starbucks | SBUX | 9,093.30 |

| Texas Instruments | TXN | 8,206.50 |

| United Parcel Services | UPS | 6,230.80 |

| VF Corporation | VFC | 5,124.60 |

| Visa | V | 10,936.50 |

| Cash | 753.08 | |

| Total | $100,520.79 |

The US total value account shows a variation of +$9,746.25 (+10.74%) since the last income report on November 6th.

Apple (AAPL)

Apple has surprised the market once again. Great Depression or not, AAPL found ways to generate more cash flow. 2020 results were okay, but the future looks bright. With many iPhone owners switching to more powerful smartphones to enjoy 5G, AAPL should be in a great position to grow through the next several years. Its service division is also thriving. During their latest quarter, they reached an all-time high in sales of $14.5B (consensus was $14.12B).

While those numbers look good as we are in the middle of a recession, the 29% revenue decrease in China caught investors’ attention. In other words, the business did very well everywhere but in China. Let’s hope this trend changes with the hope of smoother commercial relations between the U.S. and China.

BlackRock (BLK)

BlackRock counts on several growth vectors. You may think of them as the largest ETF creator with their iShares series. While their ETF business is thriving and this trend is not about to end, BLK is offering a lot more than those most popular investment vehicles.

BlackRock supports advisors with a complete platform called Aladdin. This platform is more than a simple portfolio management tool. It is a goldmine of financial data combined with artificial intelligence to help portfolio managers, advisors and institutional clients to optimize their investment decisions. In a world where retirement planning becomes the responsibility of everyone, such a tool is priceless. Aladdin is still in its early days of growth as it is being used by only 20% of portfolio managers, 23% of U.S. pensions and 17% of the top 250 insurers.

BLK is part of my tops picks for the year 2021. Find out about more companies that will crush 2021 in this article.

Disney (DIS)

Would you have believed that Disney could outperform the S&P 500 with all their parks and cruises closed and with no blockbuster movies? DIS pulled another magical trick with its streaming business. During the latest quarter Disney Plus hit 73.7M subscribers which easily outpaced expectations for 65.5M. ESPN Plus subscribers were 10.3M, vs. an expected 9.19M. Now, the company plans to reach 230M-260M subscribers by 2024.

Disney expects to be spending $14B-$16B a year by 2024 on content creation. I an assuming the dividend won’t come back right away (that’s $3B/year). But at this point, I prefer management keep the money and grow the business. Don’t worry for the long term as Disney said it expects to pay the dividend again.

Gentex (GNTX)

Gentex is the perfect example of the type of business you want in your portfolio if you are looking for growth and safety. GNTX has focused in a small niche market where it dominates the playground. Thanks to its 1,000+ patents, the company claims an over 90% market share in the auto-dimming mirror business.

Gentex has expanded its auto-dimming technology to aerospace and automotive industries. It also works on improving connectivity and sensors in cars. On top of that, it shows a stellar balance sheet with virtually no debt ($25M long term debt). This means it can manage through any storms and might become an interesting candidate for an acquisition. The company also benefits from being the first to offer this high-quality product. This leads to higher margins for early adoption and puts Gentex #1 in automakers minds for future orders.

Hasbro (HAS)

I’m willing to give Hasbro a break until I get the company’s results from the Holidays. Management has “forgotten” to increase the dividend in 2020 and I don’t like that. I understand they have a big bite to swallow (Entertainment One) and this should open the doors to future growth.

There is a natural fit between the eOne cartoons portfolio and Hasbro’s toys portfolio. We can see how content and toys go hand in hand (i.e., Disney’s business model). The company has ample liquidity and should continue to pay its dividend on top of growing its business. After a good recovery in the second half of 2020, the stock is still far from its peak price of $125/share back in 2019. My patience has limits, but we can afford to wait for a clearer view.

Lazard (LAZ)

If you have been following me for a while, you know that I really like Lazard for its unique expertise in mergers & acquisitions (M&A). With 50% of its business coming from financial advisory services (M&A and corporate restructuring), Lazard is an asset manager (the other half of its business) that has gone through several crises with great success. However, you must be ready to pay the price for having a stock with a high volatility index! The stock lost more than 50% of its value during the March crash and has recovered from it completely since then.

The last dividend increase happened in 2019 and there was no special dividend in 2020. Management had this “tradition” since 2014 (dividend increase + special year-end dividend). Like Hasbro, I’ll wait to see how things go for a quarter or two before making a final decision on this firm.

Microsoft (MSFT)

Microsoft was obviously one of my best performing stocks in 2020 with a total return of over 40%. The company seems to have everything lined-up for growth regardless of what happens with the virus. If the pandemic gets under control, MSFT will thrive with its cloud business as the economy rebounds. If we have a long winter (as I expect), MSFT products will support Corporate America’s efforts to work remotely.

Its cloud-based suite of products is perfect for anyone (or any business) working remotely. I love the subscription-based model as it ensures stability and predictability. MSFT is one of the rare businesses showing a perfect dividend triangle during this crisis. Is it overvalued? I honestly don’t care, and I would buy shares of MSFT any day of the year.

Starbucks (SBUX)

After getting hit in the face by the pandemic and forced to close many restaurants during the lockdowns, Starbucks is on track for growth again. The company closed underperforming restaurants but continued its growth plan throughout 2020. Between September 2019 and 2020, SBUX opened a net total of 1,404 restaurants (mostly international). The company opened 480 net new stores in Q4 alone.

SBUX main growth source is coming from China. The company currently enjoys solid growth as Luckin Coffee (LKNCY) has its fair share of legal problems. China has also controlled the virus rapidly, enabling many Starbucks stores there to reopen quickly. Finally, its loyalty program members increased by double-digits during the last quarter to be 19.3 million total users in the U.S. Thanks to the app, SBUX knows how to adjust its business (location, hours, menus, etc.) according to their consumers’ behavior.

Texas Instruments (TXN)

Tech is hot these days and so is the automotive industry. What better holding than a business offering analog chips to industrial and automotive players? TXN enjoyed sales growth from the automobile market rebound and additional growth demand from personal electronics. The company offers best-in-class products to those industries and counts on a massive team of sales rep to knock on the doors of opportunity.

The company is also investing massively in R&D to maintain its edge over their competition. It enables TXN to secure more customers and generate additional cross-selling opportunities as its sales teams are out in the field to push revenues to higher levels.

United Parcel Services (UPS)

I must admit, I keep having mixed feelings about UPS. On one side, the company is the leader in parcel delivery, it’s a solid dividend grower, and the e-commerce trend (supporting more deliveries) isn’t about to fade away. On the other hand, UPS faces stiff competition and Amazon (AMZN) is going all-in on building its own delivery fleet. We are talking about planes, trucks (electric!) and camels (okay, maybe not the last one).

UPS had an amazing year and it is still a very good “defensive” stock against the pandemic. If there will be future lockdowns, UPS won’t have to worry about competition. There is plenty of business for everyone. But the party will end one way or another. Do I still want to stick around and clean-up the mess? I am not certain on the answer to that question at this time.

VF Corporation (VFC)

When you look at how VF transformed Vans into a multi-billion-dollar brand over the past decade, you can imagine how they may boost Supremes’ revenue trends ($500M with a double-digit potential for growth). Supreme also counts more than 60% of its sales coming from online. This business will integrate seamlessly into VF’s direct-to-consumer selling platform.

Supreme has a profile highly like Vans’ in terms of growth potential and gross margin (roughly 60%). VF counts on using its expertise to grow Supreme through its international markets, new stores and digital sales.

I bought VF in the middle of the March crisis based on the principle that this “brand manager” will survive the storm and make some serious acquisitions in the process. Lucky for me, this is exactly what happened. I expect to see my shares continue to go up once the virus gets weaker.

Visa (V)

For a rare moment, Visa didn’t publish double-digit growth during the pandemic. However, this situation is temporary. As the economy hits pause, so to are millions of transactions. At the same time, using Visa’s network to make payments will be crucial in a world where we must stay home more often. The stock quickly recovered from March’s drop and got back to its uptrend.

As there is a clear trend toward electronic payments, Visa has already built its network to enjoy this strong tailwind. Visa is the largest player in an industry where size matters. It’s ability to follow (and create) trends in money transfer will be crucial going forward.

My entire portfolio updated for Q4 2020

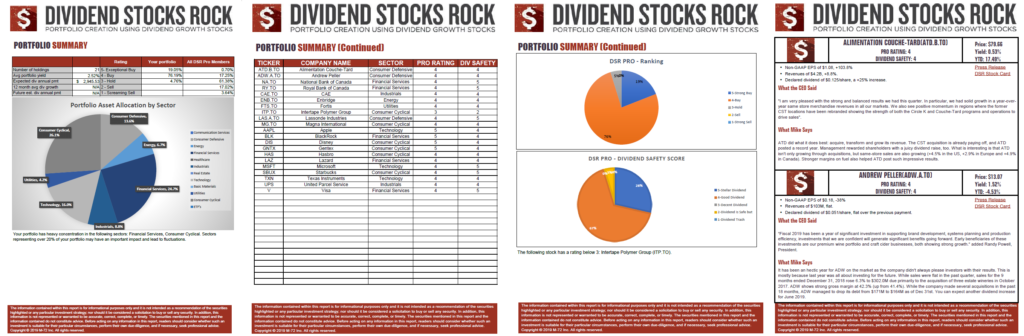

Each quarter, we run an exclusive report for Dividend Stocks Rock (DSR) members who subscribe to our very special additional service called DSR PRO. The PRO report includes a summary of each company’s earnings report for the period. We have been doing this for an entire year now and I wanted to share my own DSR PRO report for this portfolio. You can download the full PDF giving all the information about all my holdings. Results have been updated as of December 19th, 2020.

Download my portfolio Q4 2020 report.

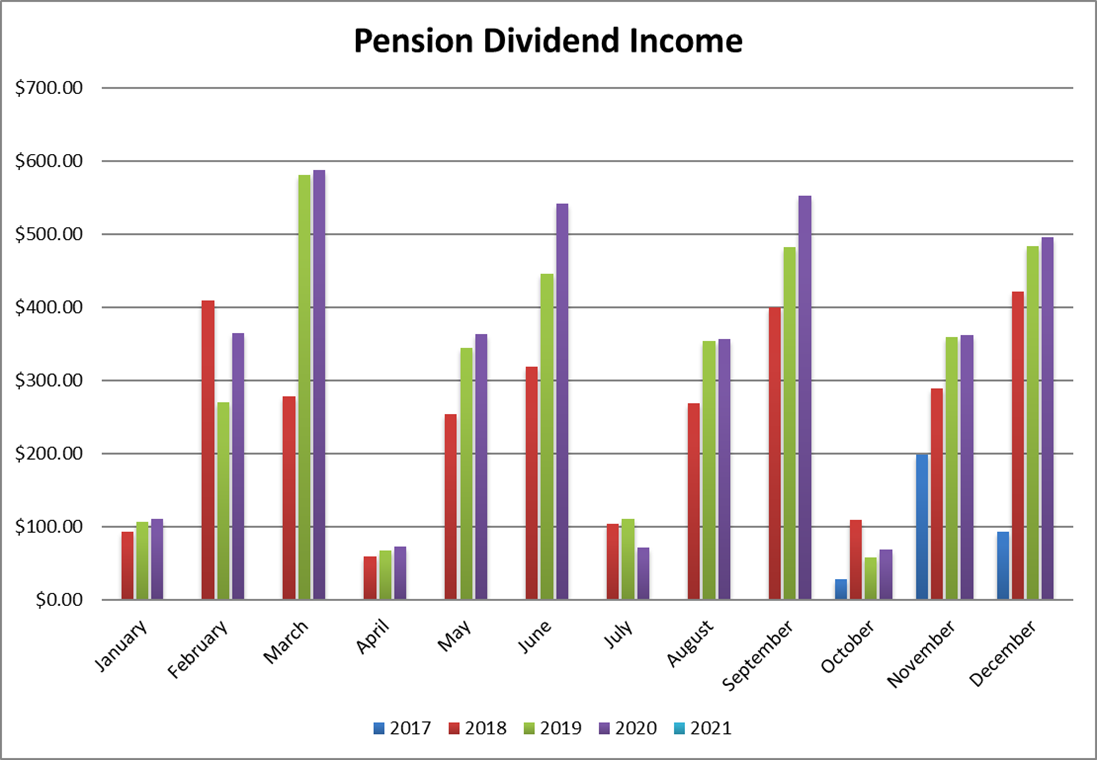

Dividend Income: $496.24 CAD (+3% vs December 2019)

The last two months of the year has been slightly better than last year. Nothing to write home about, but an increase is an increase. Since I missed my November income report, I’ve combined both months here.

Here’s the detail of my dividend payments.

Dividend growth (over the past 12 months):

- National Bank: +4.4%

- Royal Bank: +2.85%

- Fortis: +5.77%

- Enbridge: +9.7%

- Magna Intl: +5.9%

- Sylogist: +164% (I increased my position since last year)

Dividend growth (over the past 12 months, continued):

- Alimentation Couche-Tard: +40%

- Apple: -17.55% (I sold some shares earlier this year)

- Texas Instruments: +13%

- Hasbro: 0% (I need to check that!)

- Lazard: 0% (I need to check that!)

- Starbucks: +9.8%

- Visa: +6.7%

- UPS: +5.2%

- Microsoft: +9.8%

- VF Corp: new this year

- BlackRock: +10%

- Currency factor -1.5%

Canadian Holdings November payouts: $121.60 CAD

- National Bank: $56.80

- Royal Bank: $64.80

Canadian Holdings December payouts: $283.01 CAD

- Fortis: $50

- Enbridge: $130.41

- Magna Intl: $35.42

- Sylogist: $52.13

- Alimentation Couche-Tard: $15.05

U.S. Holding November payouts: $188.15 USD

- Apple: $19.68

- Texas Instruments: $51.00

- Hasbro: $31.28

- Lazard: $47.94

- Starbucks: $38.25

U.S. Holding December payouts: $167.19 USD

- Visa: $16.00

- UPS: $37.37

- Microsoft: $33.60

- VF Corp: $29.40

- BlackRock: $50.82

Total payouts (December): $496.24 CAD

*I used a USD/CAD conversion rate of 1.2754

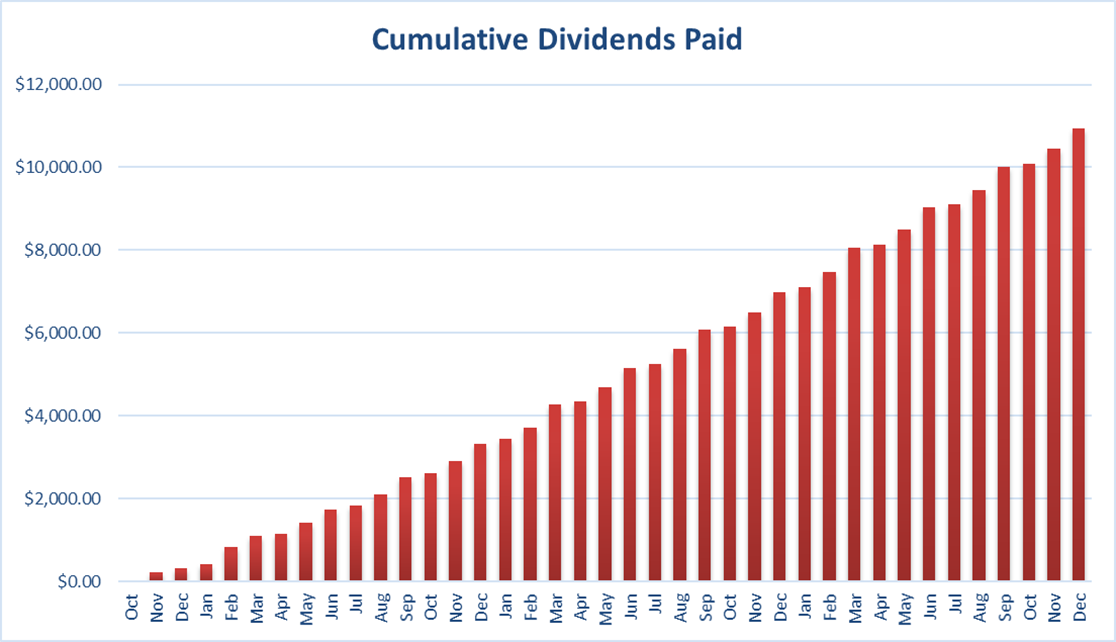

Since I started this portfolio in September 2017, I have received a total of $10,937.21 CAD in dividends. Keep in mind that this is a “pure dividend growth portfolio” as no capital can be added into this account other than retained and/or reinvested dividends. Therefore, all dividend growth is coming from the stocks and not from any additional capital.

Final Thoughts

There is no doubt 2020 was a wild ride. But when you think about it, not much has changed from an investor’s perspective.

- Find leaders in each sector.

- Make sure they have what it takes to thrive.

- Make sure they increase their dividend each year.

- Stick to your strategy.

Those simple rules worked in 2020 as they have over the past decades. I’m confident they will also work for us in 2021!

I’ll keep a close eye on UPS, Lazard and Hasbro in the first three months of the year. This is where I may make some trades in my portfolios.

Cheers,

Mike.

The post How Staying Fully Invested Turned Out for Mike’s Portfolio – December Dividend Income Report appeared first on The Dividend Guy Blog.