Every quarter, my team and I review our Dividend Stocks Rock portfolios. We use our portfolio booklets (you can find mine here) to analyse a few points such as:

- Our current sector allocation (ideally less than 20% per sector)

- Each holding’s weight in our portfolio (ideally an equally weighted portfolio)

- Each holding’s ratings (PRO rating and Dividend Safety Score to make sure we are on the right track)

When we reviewed our retirement portfolios, the first thing that came to my mind was…

Our U.S. portfolio beat its benchmark (Vanguard Dividend Appreciation ETF (VIG)) by almost 5% and our Canadian portfolio outperformed its benchmark (iShares Canadian Select Dividend ETF (XDV.TO)) by 14% since inception. This is a most credible performance considering that both the S&P 500 and the TSX 60 have been lagging dividend growth ETFs. In other words, Dividend Stocks Rock!

Source: Ycharts, data between July 31st 2018 and February 19th 2020 (before the bell).

Surprisingly, our retirement portfolios are among the best performing portfolio models we have over the past 12 months (you can check our Dividend Stocks Rock portfolios). How can we explain that a group of stocks selected for their relatively higher yield and lower volatility (for some) outperform a bull market? I can think of a few points:

- Some stocks were temporarily showing a higher yield (and the market caught up to it).

- A low interest rate environment pushes more income seeking investors toward high yielding stocks.

- Following a meticulously crafted dividend growth investing plan works.

But, enough with the self praise and let’s now discuss what we do from this point forward. After all, the whole purpose of those portfolios is to generate between 4% and 5% yield. The retirement portfolio should generate enough income from its yield that you don’t have to sell shares to cover your needs for income. This is the definition of a stress-free retirement. Last time I checked, the U.S. retirement portfolio fell behind and now shows a yield of 3.91%!

This brings me to the following question:

Should You Sell Your Winners to Generate More Income?

I like to manage the portfolio models the same way I manage my money. If you look at my pension plan portfolio, you will notice how similar my holdings are compared to our DSR picks.

In my portfolio, I would never sell a stock simply because the yield has gone under an arbitrarily set percentage. In fact, when that happens, I smile! It means that share prices are up! But the retirement portfolios case is a bit different. After all, it’s a portfolio model using real life data, but not invested with real life money!

At DSR, we want to make sure it appeals to our members looking at the portfolio for the first time. If we let the U.S. portfolio go that way, chances are it will show a 3% yield in a couple of years. At that point, there is no interest in following this model for your own retirement. For this reason, we have initiated 5 trades for the U.S. portfolio and 2 for the Canadian portfolio. We sold our interests in certain lower yielding stocks (that have appreciated nicely), and improved our overall average yield by selecting alternative companies with more generous current dividend payouts.

Now, let’s imagine it’s a real portfolio for a real retiree at this moment. Would you sell your winners to pick higher yielding stocks? This could be a smart and economic idea. Since you are seeking the highest income possible to cover your needs, this process gives you a nice pay raise? By selling your winners, you would have more capital to invest in the higher yielding companies. This is a smart technique to re-allocate your capital in order to reach your income goal.

Dividend growth investing is all about keeping your stocks for the long haul if possible and enjoying the power of compounding interest. But, when you reach retirement, other priorities become more important. Active portfolio management could significantly improve your income as you cash in on your past best ideas. Once you retire you are not after growing the largest portfolio possible anymore because you transition to being all about maximizing your capital to generate the highest income possible.

Here’s an example of what we did in February:

Sell Blackstone (BX)

Blackstone has made investors happy with the announcement of its imminent conversion into a corporation (it was a limited partnership before). The stock returned about 82% in this portfolio since its inception.

Source: Ycharts

Blackstone is a complex beast. BX could look like another asset manager offering a generous dividend yield to shareholders. Well, it is more complicated. Since Blackstone keeps a cut on the profit realized on its investment, both revenues and earnings go up and down from one quarter to the other. Moreover, the strong dividend payment is also based on performance. Still, the company shows steady assets under management growth and benefits from its good reputation. Their decision of converting BX into a corporation (it was a limited partnership) in 2019 pleased investors as taxes paperwork just got a whole lot easier. This also boosted everybody’s return as shares surged.

Cashing this gain, we wanted to keep our money invested in the financial services sector. We sold BX now paying ~3.2% and we found a great way to pick another asset manager offering a 7% yield.

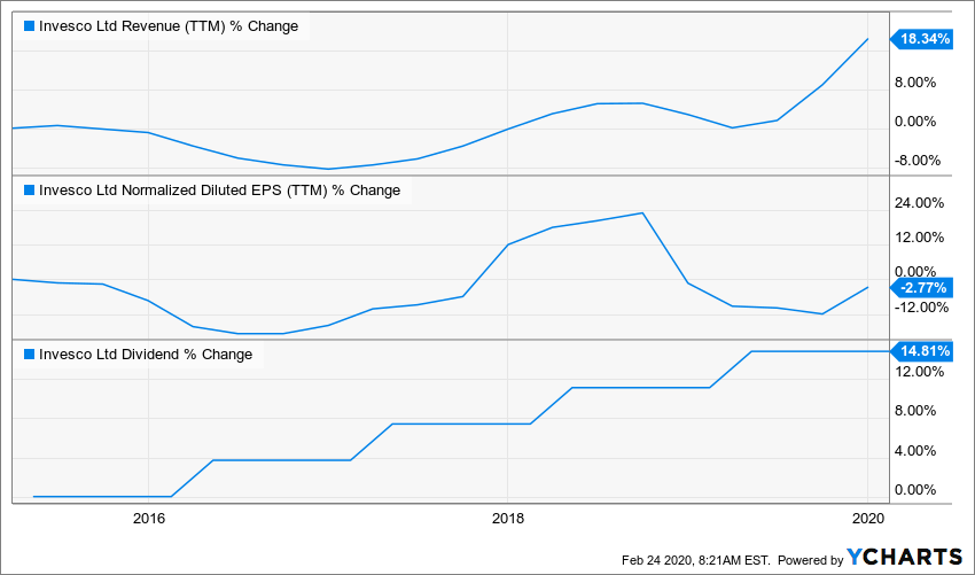

Buy Invesco (IVZ)

Clients investing with IVZ (not its shareholders, but its clients), do it because Invesco’s portfolio managers have shown they can beat their peer over the long haul. Any downturn in the stock market will reinforce this position as people want to hang out with winners. I like the way management uses its cash. The company generates over $1 billion in cash flow but will use most of it to finance its ETFs purchases instead of going overly generous with shareholders (through dividend raise or stock repurchase). I like when management thinks about its business growth first. OppenheimerFunds deal will increase Invesco’s AUM to nearly $1.2T and put IVZ on the map right behind companies like Vanguards and BlackRock.

Source: Ycharts

It’s Groundhog Day for Invesco as the financial firm didn’t meet the market’s expectations when it published its latest earnings on January 29th. Revenue jumped, but it’s all coming from the OppenheimerFunds integration.

“The integration of OppenheimerFunds has significantly strengthened our ability to meet client needs and achieve strong operating results on behalf of shareholders, including a 15.6% increase in net revenues and a 38.1% growth in AUM year over year.”

What the market didn’t like is the $14B of long-term net outflows. Q4 ended with assets under management of $1.23T, up 3.5% vs. the end of Q3; average AUM of $1.20T increased 1.0% Q/Q. The AUM growth comes only from the acquisition.

President and CEO Marty Flanagan expects increased clarity on Brexit and the U.S.-China trade deal to “help us build on the positive net flows we saw throughout 2019 in our business outside the Americas”.

You’ll have to be patient with this one, but IVZ shows both payout and cash payout ratios under control and a juicy ~7% yield. This could be a very good trade for an income seeking investor.

5 Income Stocks all Retirees Should Have in Their Portfolio

I know that some investors will tell me there are incredible opportunities with a “safe” dividend payment and a 11% yield. But I’d like to have this conversation once we hit a bear market and your company cuts its dividend to see its shares tumble.

Therefore, my goal was to pick among companies that are slightly more generous than others. Just by using a 4-6% yield condition in my stock screener, I dropped the number potential companies to about 1,000 candidates (for both US and Canadian market). I then I applied my investing process to screen all of them and came up with my top 5 retirement stocks. Download them here for free:

The post Generate More Income With This Smart Trade appeared first on The Dividend Guy Blog.