My Christmas Wish List

We are currently approaching one of my favorite times of the year; the Holidays!

I obviously like this period of the year because of the magic that surrounds my children. This year, we had to tell our oldest son (he is 10) that Santa is well… Mom & Dad! He kind of knew about it, but it was still fun to pretend

There is also another reason why I like the Holidays so much; it’s the time of the year where I put everything on hold and think about my future. Each year, I spend a few moments to just think. It could be a morning while my kids are playing around and I’m sitting alone with my coffee and a note pad or an entire day at the spa. I take the time to look back at the past 12 months and think of how I want the next 12 to happen. This year has been great;

I’ve finally built a real business on solid ground,

I’ve finished my year with a great bonus at work,

I’ve worked out on a regular basis (now working out 5 times a week!),

I’ve announced to my boss that I’m taking a sabbatical,

Not too bad, but I’m really looking forward to next year as I will start my RV trip! We work on this project pretty much every weekend. We try to do 2-3 hours per weekend so it doesn’t become too much of a burden. So far, we have done a great deal of things, and there is still lots to do! There are a few things that could happen in the next 12 months to make my life easier. These are on my Christmas Wish list:

One Website

This year, we bought Dividend Monk in March. This was a great addition to our website portfolio as it integrates perfectly into our business model with our other investing website. On top of it, we now own the copyrights to one of the best dividend investing books; The Dividend Toolkit. Dividend Monk has been a great cash flow generating machine, similar to a dividend paying stock ;-).

I wish I could buy another website before heading out on my RV trip. This would solidify my cash flow while I’m the road. I wish I had been aware that Jason wanted to sell his blog; Dividend Mantra. The site has been sold to some “marketing professionals” and they have yet to “restart” the blog. I’ve enquired about the possibility of buying it back from them but I haven’t heard anything back yet. This is why it is still on my wish list!

One Tenant

A few months ago, we decided not to sell our house. The market is very slow right now and I would not make much money out of the sale. Plus, once I come back, I would be stuck with no house and very limited financing options since I would be left with no proof of income for 2016-17. If I rent my house, this will support a part of its cost and free up more money for our trip. We will be putting the house for rent early in 2016, probably even in January.

Free Cash Flow

To use financial terms, I’d like to generate some free cash flow towards the end of 2016. The idea once we start travelling is to cover our expenses from our website. The worst case scenario implies I take money out from my retirement investment account. However, the best case scenario is the opposite. There is a possibility where I could generate extra cash flow and would then be able to invest this money in dividend stocks. I’m far from this reality today, but it’s not impossible that my hard work leads me to a situation where the company generates between $8,000 and $10,000 per month. In this situation, I would be able to invest in the stock market and secure my financial independence.

A Family

My last wish and most important is not something I want, but something I want to keep. I want to keep my incredible wife by my side and my three awesome kids. I have so much fun with them that I would like to spend each hour of my life surrounded by them. This is another reason why we have decided to put our busy lives on pause in order to spend more time as a family. I hope we will be all safe and sound so we can appreciate this trip.

What’s on Your Christmas List?

Come on! It’s not too late to write Santa a letter, what is on your Christmas Wish List?

… And we Thought the Canadian Economy Depended on Oil

The economy is like my wife, it will never cease to surprise me

I’m somewhat surprised by the Canadian economy vs how the market reacts. The Canadian GDP recently escaped its “technical recession” (2 quarters of decreasing GDP in a row) during the third quarter. We can’t say the market followed this great news:

I’m not surprised the Canadian market is down this year, yet I am surprised the Canadian economy is growing regardless of the very poor performance of the resources sector.

Both the oil and mining industries lead the biggest losers in the stock market this year. In fact, I don’t think that I can recall seeing the price of any commodity in the green this year. It’s pretty much a big black hole where everything has fallen into the ocean abyss. This will end, eventually! However, there is a very interesting phenomenon happening in the meantime; the Canadian economy isn’t slowing down.

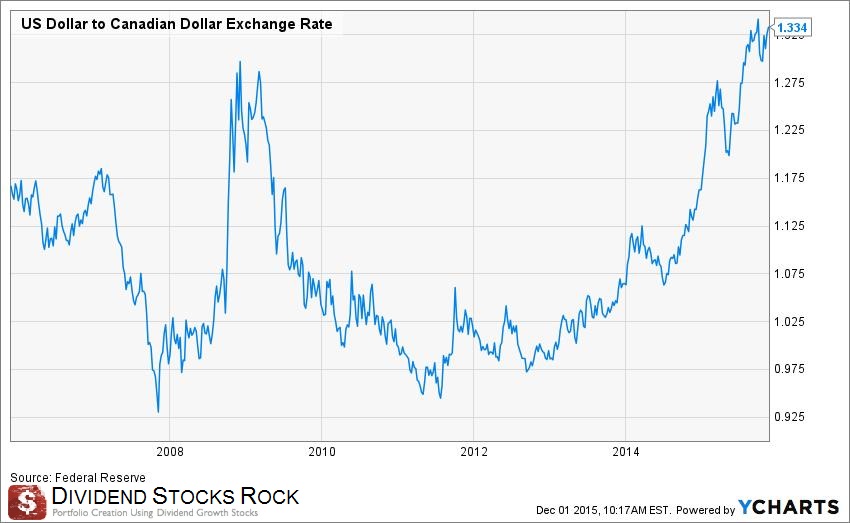

When Canadian GDP dropped for 2 quarters in a row, we all expected this. It was only normal to see an economic slowdown since the bulk of our systems revolve around resource related industries. But other factors kicked in and brought the Canadian economy back on track. The main factor I can see to explain this is the currency exchange rate with our southern neighbors:

Since 2012, the CAD is losing steam against the USD. It became quite obvious during 2014. The CAD hasn’t been that cheap over the past 10 years! Eventually, this weighs in for Americans as they are starting to see the advantage of “buying Canadian”. Manufacturing industries are slower to move their money from one place to another as compared to the oil exploration industry. However, we can clearly see that Canadian manufacturers now ship more goods to the US.

We also expected Canadian consumers (that are already indebted up to their neck) to slow down their credit cards. Roughly 60% of the Canadian economy relies on its consumers. With major budget cuts in Alberta in the oil sand industry, we expected increasing unemployment and decreasing consumer goods purchased. Well Canadian employment showed resilience and other jobs in other industries were created at the same time as many workers lost their well-paid jobs in northern Alberta. Let’s not put the rose-colored glasses on yet, a job lost in the oil industry is not replaced with the same quality in the service or manufacturing industry. Still, the point is that we expected the worst for Canada this summer and we are experiencing the best case scenario instead.

Is it Time to Get Back to Canadian Stocks, eh?

As we are now in December, I’m currently working on my “Best 2016 Dividend Stocks Book” and I think we might be surprised with Canadian stocks in 2016. There has been lots of money that have been made in the US market over the past 7 years and I think it will continue in 2016. However, I also think the Canadian market will benefit from this drop in the market in 2015 to bounce back next year. Just look at how the Big Five have reacted so far in the market:

Interesting enough, they all show negative returns besides the CIBC but they all posted stronger profits than last year. Considering their healthy dividends, Canadian banks might show a great entry price at the moment to fill-up your portfolio with a fresh high dividend yield around 4%.

The Canadian banks were penalized this year as we expected loan loss reserves to rise and the economy to slow down. Once again, banks benefited from a stronger than expected economy and were able to pull out a few more bucks in profit. I wrote a complete report on banks for Seeking Alpha earlier this summer. I think it’s time to re-read this article and find some interesting picks among banks!

There are Lots More than Banks in Canada!

As you know, I recently bought Canadian Railway (CNR.TO) and I’ve found several other great Canadian companies to buy in the upcoming months. The market being down by roughly 7-8% this year while the economy is showing resilience makes me think there are several opportunities on the stock market. It’s up to you to find them (it’s like an Easter Egg Hunt! Hahaha!).

You know I will share some of my favorite stocks for the year shortly, but I want to hear from you first; what is on your watch list these days?

Cash Flow To Freedom

Since the beginning of the year, I have been talking about my newest big project: leaving for a 1 year trip in an RV. The countdown is now official; we are leaving on June 11th 2016. Therefore, we only have 7 months left before we leave. Over the past few months, I’ve made several modifications to my finances in order to fund this project. I’m sharing this information with you as I want to show you that anybody can do it. It’s not a matter of money, it’s a matter of determination.

I didn’t win the lottery;

I didn’t save up for 5 years;

I didn’t benefit from a special program offered by my employer;

I’m not super frugal, I actually need close to $6,000/month to live;

Maybe I’m just a bit crazy…

The reason why I can make this project happen is mainly because I focus most of my efforts towards cash flow generation. We rarely hear about cash flow when we talk about personal finance; this is more a business related term.

When you look at a business’ financial statements, one of the most important points is not the revenues or the earnings; it’s the cash flow. The rest could be pure accounting fairy tales; but you can’t play around with the cash coming and going through your bank account. This is literally the blood fueling the business. If there is none, the business won’t run for very long.

Leaving Classic Personal Finance Concepts Behind

When we talk about personal finance, we often talk about budget, assets, liabilities and net worth. If I had used these concepts to do my project, I would have to set a budget to determine my savings ability. Then, I would created an “RV project investment account” and invested in it monthly. The project alone requires around $3,000 per month for 12 months or $36,000 for the full year. Add a few extras and you get to $40,000. Since I decided to rent a villa in Costa Rica, add another 12K… and finish the calculation to a $52,000 budget.

How many months, read years, will I have to wait before leaving? Probably something in between 5 and 10 years. In 10 years, my oldest son will be 20, my daughter 18 and the youngest 14… I highly doubt they would leave with us! This is why I had to find another way to finance my project. Here comes the concept of cash flow generation.

What is the Difference when Focusing on Cash Flow Generation

Over the years, I’ve realized I’m not the best guy at being frugal. I have a taste for nice things and while I’ve stopped buying stuff just for the sake of it, I still spend a decent amount of money on quality items. For example, I find it more important to buy lots of vegetables, fruit and natural products to cook healthy food than eating peanut butter and cereal each morning (I drink green juice for the record ). However, buying these fresh products is not about being frugal.

While I suck at frugality, I’m an ace when it comes to generating money. Since the beginning of the year, I have worked very hard to create a cash flow generating machine that will sustain my lifestyle while I’m gone. This machine is my online websites. Through my blogs and membership website Dividend Stocks Rock; I have the ability to generate additional cash flow no matter where I live. All I need is a laptop and an internet connection!

The main difference with cash flow generation is that you focus on the future money coming in instead of waiting to have it in your pocket beforehand. Then again, this is another concept that is being far away from any “sound personal finance advice”. But this is how a business works; it doesn’t wait 5 to 10 years to fund its projects; it invests right away and works on their cash flow to finance the project as it goes. I agree with you; it is definitely riskier than waiting to have your money in the bank account to finance your project. But this is the kind of move that puts me under pressure to perform and this is when I am at my best!

Going From $500 To $3,000/month in 12 months

Back in January of last year, my cash flow ability was around $500/month with my online company. We had a rough period in 2012 and 2013 and we have spent the whole year of 2014 to “rebuild” a very large part of our company. Basically, what happened in 2012 what that Google hit most of our blogs by a major deranking it their search engine. The bulk of our business model was based on selling text links and making money through Google Adsense. The business revenue model collapsed by 80% in the span of 3-4 months. The funny thing is that I almost quit my job in 2012 to live full time from my online company… It was a blessing to have not done this!

We then spent several months on building a stronger business that doesn’t rely on selling text links (something that Google truly hates! hahaha!) and doesn’t even require Google traffic at all. Going through such a modification takes lots of time, effort and energy. The worse part is that it doesn’t always generate results!

Fast forward to early 2015, we are now back to positive and had the ability to roughly generate $500/month in cash flow. This “cash flow” is not the definition of my cash flow in my business financial report, but the money I can take away from the company without hurting it. In other words; the dividend I feel I can pay myself with! at $500/month, we didn’t started to pay ourselves dividends (I work with a partner in this company). We started to pay off our corporate debts instead in order to make sure the company was in stellar condition when I will leave in 2016.

Slowly but surely, we have worked on increasing our revenue and managing our expenses closely. When I look at the months of October and November, I now realize that I am now generating $2,000 per month that could be paid through dividends. This amount will “magically” increase to $3,000 as my Virtual Assistant will stop working for a one year maternity leave…This is perfect timing as I will have more time to do her work and I will not have to hurt the financial structure of my company to pay for my trip.

Since I’ll be working full time on the company, my partner and I agreed I would take the full amount from the company to fund my RV project. Yes… I have the best partner in town! At $3,000/month, I’m almost covering all my expenses. In fact, the rest of my expenses aren’t linked to my trip, but to the fact that I’m keeping my house while I travel.

We have decided to rent it instead, but this part isn’t done yet. I will put the house for rent in March next year, leaving me roughly 3 months to rent it. If it doesn’t work, we will leave anyway and assume the cost. This will add pressure to our budget, but I have remortgaged the house and put some money aside to cover for the expenses generated by my house.

Final Thoughts

It took me a year of working evenings and nights on my blogs while I work full time at my day job, but it was worth it. After a year of hard work, I can see that my online business will cover most of my expenses while I’m living the dream of my life.

I’m not done yet as my next goal is to bring this cash flow generation machine to $6,000/month to cover for my entire lifestyle and finally reach financial independence at the age of 36. I like that idea; retiring at 35 and reaching financial independence at 36… All that because I’ve quit relying on classic personal finance principles

From Cash to Dividend Stocks: Building a Retirement Portfolio Step by Step

December 07, 2015

Warning; this article is massive and contains lots of great info

A couple of weeks ago, I received an email from one of my readers. He was in a delicate situation: he was 100% cash and wondered where to start in order to build his retirement portfolio. We exchanged a few emails and I agreed with him that many investors are in the same boat: they got out of the market at one point and are now sitting on the sidelines wondering how they can re-enter without making big mistakes. When you see a few hundred thousand in your retirement account, the last thing you want is to see it disappear because you entered the market right before the next crash. In order to give you the full picture, I asked the reader if I could share his email. He agreed and I decided to call him Caleb, my third child’s name for privacy purposes. Here’s the email from Caleb:

Thanks for the articles, very informative! I wanted to reply to you to let you know how my investing is going…it’s not to tell you the truth.

Not that I don’t want to…I need to. But I’m stuck. I have 600K+ in investment cash (self directed IRA), sitting in money market. I’m just too spooked with the market, economy, gov’t shutdowns, budget deals, geo-political BS, interest rates, the Fed, all the uncertainty! And I know its not good to be sitting on the sidelines, I have to get my money working.

So here’s the dilemma, how to I get back in? What would you do in my situation. And I can guarantee you, there are many other investors out there like me in the same boat.

My wife and I are in our mid 50’s, we have great jobs, 401K’s, so forth. I know what to do in the 401’s, I’m just stuck on what to do to get re-engaged with my IRA.

I am interested in managing my own portfolio, a percentage (say 20%) with Covered Calls. And I think it would be prudent to include dividend investing as well.

So I’ll stop there and get your thoughts…how would you approach my situation.

Thanks!

Caleb

First Question: When Do I Get Back In?

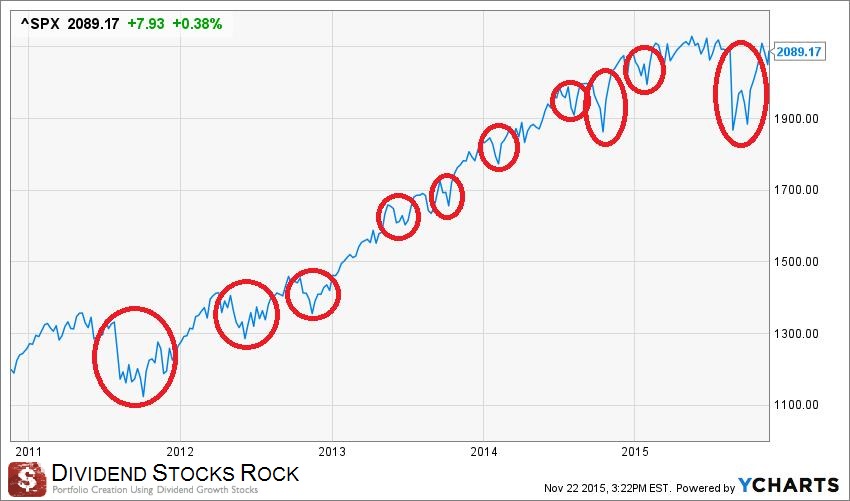

Whenever you take the decision to sell your stocks to avoid a market crash or further losses, you also enter very dangerous territory. You enter in an environment of doubt where you will never be certain when is the best time to invest again. If you exited the market back in 2008, you are probably in a situation where you wonder when it’s time to get back in. While we went through one of the best bull markets ever on the stock market over the past 5 years, there were many occasions with drops to make you wonder even more about the “perfect entry point”:

As you can see, there were 10 spots where the market dropped enough to make you double guess your decision to enter or leave the market. But what is the most important point? The S&P 500 was at 1,200 five years ago and it is at 2,090 today. In other words; someone who hesitated due to short term events, left lots of money on the table. As Caleb mentioned in his email; there is always a good reason to not invest. Since 2008, we had:

The US Government printing money like there is no tomorrow (QE1, QE2 and QE3)

US Government budget saga

Greece default saga

Germany going through recession

Oil price falling and forcing Canada to drop interest rates again

China building ghost cities and showing mid-single digit growth rates

China (again!) stock market collapse of 43% during summer of 2015

China (still!!!) with their heavy leverage strategies and shadow banking

France terrorist assaults

And I’m pretty sure I forgot half a dozen others reasons not to invest over the past 7 years. On the other hand, the past 7 seven years have been some of the most prolific years on the stock market. The thing is that there will always be a “good” outside reason to not invest. But the reason why we all invest is not because we think Governments will do a good job with our economy or because war will end and we will live peacefully. The reason why we invest is because companies make money. And they do it regardless of what is happening in the media. Therefore, the real question is not when do I back in, but rather how do I get back in?

How do I get Back In?

The short answer would be “as soon as possible”, but it doesn’t make sense to invest $500,000 in the stock market over the span of a month. Therefore, you need a reinvesting plan. Mathematically, you would be better off investing as soon as you can in order to build a strong portfolio and benefit from the power of dividend growth. But if you have gotten out of the stock market in the first place, it is because your fear of being burnt by the stock market is greater than missing a dividend payment. Therefore, I would suggest you invest 1/6 of your cash each month over a period of six month. Investing over a longer period of time will make you second guess each of your moves and you will be striken with paralysis by analysis.

By investing a sixth of your money each month, it gives you enough time to build a strong portfolio and not buy everything you see as you were in the middle of Black Friday. If you are unlucky and hit a bear market, you will not lose everything in the first month!

Now that we know how much we will invest, we need to know in which stocks we will invest right?

Which Stocks do I Buy?

Before you make your first purchase, you need to know where you are going. The first step is to build a list of interesting stocks, a list of companies that you want to be included in your portfolio, a list of companies that fit your investing criteria. Such a list can be built from scratch if you like spending lots of time playing with stock screeners and reading financial statements. If you are want to peruse some pre-screened lists, you can always check the following resources across the web:

The dividend champion list (Dave Fish)

The aristocrats list (Sure Dividend)

The Canadian dividend all-star list (Dividend Growth Investing and Retirement)

The Canadian aristocrats list (Dividend Earner)

Or from my website:

10 Dividend Growth Stocks for a Rock Solid Portfolio

My own Buy List

20 Strong Dividend Growth Stocks from the Rock Solid Ranking

The bottom line is to make a list of enough companies that should be part of your portfolio and not from the same sector as well as you want to build a portfolio out of your list. In an ideal world, you would need stocks in the following sectors:

Consumer defensive – usually part of any core dividend growth portfolio

Consumer cyclical – gives an additional push when the economy is doing well

Industrials – there are some very good and stable companies in the industrial sector

Technology – you might be surprised, but there are some hidden gems in the techno industry paying dividends.

Healthcare – here again, there are a few big pharma that will boost your returns

Communication Services – telecoms are often the most cited as dividend growth stocks

Financial Services – they have experienced bad press since 2008, but they have starting to pay good dividends since then

Utilities – not the best place to find growth, but definitely a good place for steady dividend payments

Real Estate – there isn’t much growth perspective with REITs, but still, you can get high dividend yields here

Basic Materials – more volatile and risky

Energy – same here

MLP’s – Master Limited Partnerships could be an interesting beast to add to your portfolio, I suggest you read Dividend Monk’s Guide to MLPs to fully understand how they work.

There isn’t a perfect asset allocation and the one shown in the graph above is just to provide an image of sector allocation and it’s not close to what I’m using in my own model. The main idea is not to have more than 20% of a specific sector in your portfolio in order to avoid high volatility.

When Should You Buy The Stocks on Your Watch List?

If you are like Caleb, chances are you are not convinced as to when to invest in the stock market… period. Having a watch list is the first active step to building your retirement portfolio. However, a list of stocks won’t do much if you don’t start investing at one point.

To be honest, I would probably buy any company on my watch list at any moment if I had more money to invest. The rationale behind this though is quite simple; a good company remains a good company, even when it is overpriced. Sure, in an ideal world, we would always buy companies at their lowest point ever and see them climbing sky high right after we made the purchase. However, we know it doesn’t work this way.

A few years ago, I bought both Lockheed Martin (LMT) and Disney (DIS) at their 52 week high points. Both show incredible returns so far. Therefore, they were trading high, but they simply continued to go higher. Waiting for these stocks to drop would have had me lose lots of money and I would have probably never bought them. This is the risk with waiting; never buying the stock you should have bought in the first place.

This is why I also use stock valuation methods to determine if a company is trading at a discount or not according to my calculation. I won’t lie to you; stock valuation is halfway between science and magic. The numbers you put in is based on your assumptions for the future. Therefore, your calculations are only as good as your assumptions.

I personally use two methods to determine a stock value. The first one is quite simple; I look at the stock PE ratio over the past 10 years to see how the market values the company on average. This gives me a rough idea if the company is overvalued or not.

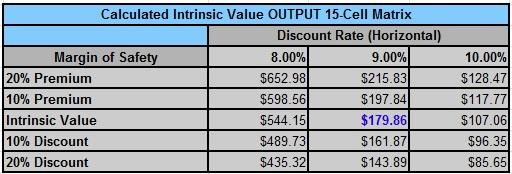

Then, I use a double stage dividend growth model (called DDM) to value the stock as a dividend paying machine. I like the Dividend Monk’s calculation spreadsheet as it gives 15 variations of results depending on a margin of safety (or premium) of 10 and 20% along with 3 different discount rates. Here’s an example:

When the value is good, I pull the trigger and buy the stock. In an ideal world, I like to have positions not exceeding 5% of my total portfolio. Depending on the amount invested, the maximum stocks I would hold would be around 30 for a 500K+ portfolio. Most professional managers don’t go over 50-60 and several of them keep to 30-40 holdings. This makes it easy to follow each company with the attention it deserves.

Why I Talk Solely about Dividend Growth Stocks?

The short answer would be: “because I’m The Dividend Guy, DUH!” But there is a smarter answer. Because a dividend growth stock is the perfect tool to design a retirement portfolio. Dividend growth stocks will provide both security and steady payments at the same time. A strong portfolio with sound companies will also grow throughout time and if you build your dividend portfolio today in your 50s as Caleb and his wife are, you will benefit from the power of compounding dividend growth for a good 30-35 years (life expectancy is getting close to 85 in North America).

A company can be called a dividend growth stock when it is obvious that management has been and will continue to increase its dividend payouts for several years. These companies are usually able to generate continuous revenue, earnings and cash flow increases. Do you think such companies lose a lot of value on the stock market over time? Nope, they gain value at the same time they grow their dividend. During a bear market, all you have to do is to ignore the noise and focus on your dividend payment. If you have made the right picks, your payments will increase… even during tough times.

What about Covered Call ETFs?

Caleb also mentioned the thought of using 20% of his portfolio to invest in covered calls. If you have been a long time reader of this blog, you know I’m not a big fan of covered call ETFs and I would not put a penny in such investment vehicle anymore. They sure pay a juicy dividend yield at first and the theory seems to make sense. But in the end, you are not buying anything that will make you rich. You can read about my own adventure in covered calls here:

The Pros and Cons of Selling Covered Calls on Dividend Paying Stocks

Covered Call ETF High Income, Low Risk?

Covered Call ETF Vs Pure Dividend Stocks

Enough said about Covered Call ETFs, they are just a good idea on paper. They are nowhere close to be comparable to dividend growth stocks.

Final Thoughts – Want to Go Further?

All right… I think I’ve exceeded your patience by now with such a long article. However, I really wanted to give you a complete picture of what I would do if I was in Caleb’s shoes. I’m wondering what would you do?

Since Caleb was nice enough to write me an email with a detailed question, I gave him a free access to Dividend Stocks Rock for 6 weeks. I think this site with the real life portfolio models with active trading along with the newsletter (including a monthly buy list) will help him build and manage his portfolio.

Since you didn’t have this chance, I wanted to leave you with the free guide I wrote about building a retirement portfolio. I hope you will like it!

Or click here to donwload!

Or click here to donwload!

New Purchase CNR

Earlier this week, I announced that I sold my position in Black Diamond. While their dividend wasn’t at risk, management decided to cut it by 38% to improve the company’s cash flow for the future. While I can appreciate why management took this decision, it goes against my 7 investing principles. This is not without any regret, but I’ve pulled the trigger on BDI.TO and quickly replaced the company by a stronger dividend payer.

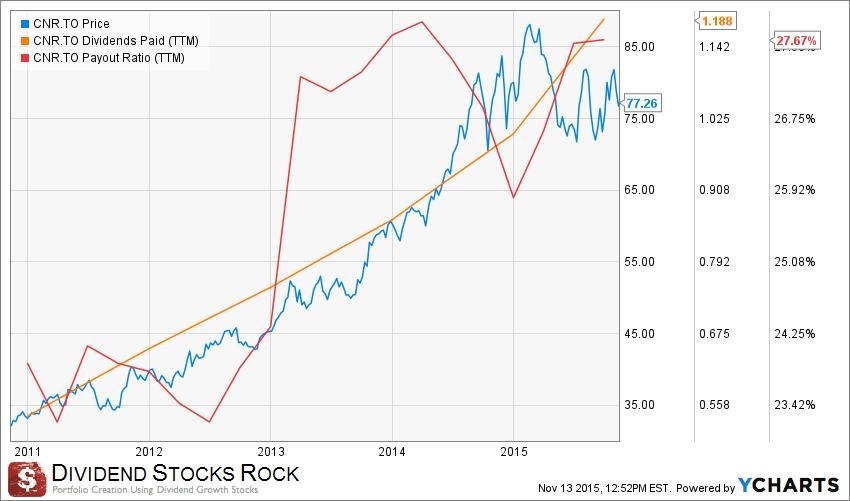

I Bought 42 Shares of Canadian National Railway (CNR.TO) at $77.35

Canadian National Railway owns and operates the largest railway in Canada and also operates in the USA. The company’s transportation activities are well diversified among 7 different industries:

Petroleum & chemicals, metals & minerals, forest products, coal, grain & fertilizers, intermodal and automotive.

In other words; whatever needs transportation across a long distance, CNR has the knowledge and the capacity to do so.

I must admit CNR didn’t blink on my dashboard for a while because its dividend yield is relatively low. At a 1.62% yield, we can’t talk about a “strong” dividend payer. However, after digging further, I realize how strong the company’s fundamentals are. The company shows incredibly strong metrics:

5 year revenue growth of 11.22% CAGR

5 year EPS growth of 14.64% CAGR

5 years dividend growth of 15.40% CAGR

Very low payout ratio of 27.39%

So for those who will tell me CNR dividend yield is too low, imagine that if you had bought it 5 years ago, your dividend yield based on your cost of purchase would be 3.60% today:

Such strong dividend growth rate usually comes at the expense of a higher payout ratio. As you can see, the company has maintained its payout ratio between 23% and 28% for the past 5 years.

I like the business structure as the company is built to generate a consistent cash flow:

The management team makes sure to use a good part of this cash flow to maintain and improve their railways (their biggest expense) at the same time as rewarding shareholders with generous dividend payments.

CNR has a very strong economic moat as railways are virtually impossible to replicate. Therefore, you can count on increasing cash flow coming in each year. Plus, there isn’t any better way to transport most commodities than by train.

Valuation

In order to determine CNR’s stock valuation, I use a double stage dividend discount model. This helps me attribute a fair value to the company considering its dividend growth capacity.

Since CNR evolves in a fairly stable and predictable market, I will use a discount rate of 9%. As for dividend growth, I use a 10% rate for the first 10 years and reduce it to 7% to be more conservative. The 10% dividend growth for the first 10 years seems aggressive at first, but considering the company increased it by 15% CAGR over the past 5 years, I think that using 10% for the first 10 years is a fair assessment:

According to my calculation, I bought the company with a 10% margin of safety (meaning the company’s intrinsic value should be around $85). This is a very good purchase considering the current market. In light of my analysis, I could say that the CNR dividend yield is low due to the strong interest from shareholders for such a well-managed company.

This holding will be part of my “core portfolio” and I intend to hold it for several years… if not forever!

© Copyright 2013 Adividend