Financials – Interest Rates & Central Banks

It seems that, after all, the FED was a prognosticator on how best to save the US economy by using unconventional tools. At one point in time, we even thought the FED was playing Dr. Frankenstein by using quantitative easing (QE) to supercharge the stock market. While they could have created an unstoppable monster, it seems that it has worked well so far.

Now, it’s time for Mario Draghi, President of the European Central Bank (ECB) to play on the same playground. On March 10th, the ECB not only reduced its interest rate to zero, but also boosted its QE operation from 60 billion euros to 80 billion euros.

“The Governing Council expects key interest rates to remain at present or lower levels for a long period of time and well past the horizon of our net asset purchases,” Draghi said. Based on the current view, “we don’t anticipate it will be necessary to reduce rates further.”

In Canada, we are patiently waiting for the first Liberal Government’s budget to see how the new government intends to revive the ailing Canadian economy. So far, we have the natural resources and energy sectors that are struggling in a massive way. The latest oil price increase should put a small Band-Aid on this heavy wound. On the other hand, we have the service and manufacturing sectors taking the lead to pull the Canadian economy’s head right above water. Here’s what we can read from the Bank of Canada’s latest statement on interest rates:

“Prices of oil and other commodities have rebounded in recent weeks. In this context, and in light of shifting expectations for monetary policy in Canada and the United States, the Canadian dollar has appreciated from its recent lows. With these movements, both the price of oil and the exchange rate have averaged close to levels assumed in the January MPR.

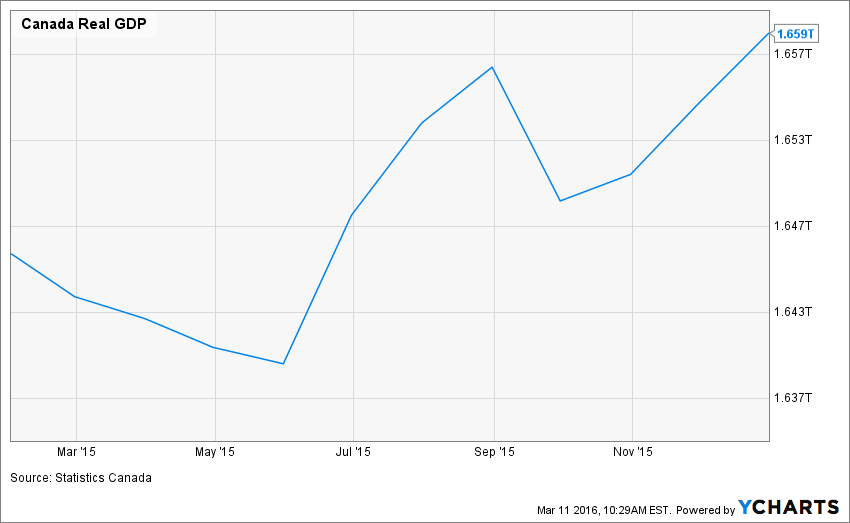

Canada’s GDP growth in the fourth quarter was not as weak as expected, but the near-term outlook for the economy remains broadly the same as in January. National employment has held up despite job losses in resource-intensive regions, and household spending continues to underpin domestic demand. Non-energy exports are gathering momentum, particularly in sectors that are sensitive to exchange rate movements. However, overall business investment remains very weak due to retrenchment in the resource sector.”

source: Ycharts

As you can see on the above chart is that we are not in recession, but we are not in a growing economy either. The Canadian economy is growing slowly, but we are closer to call it stagnation more than anything else.

In the US, we have a FED ready to pull the trigger on an interest rate hike once again in the upcoming months. With the unemployment rate below the 5% bar, the FED is navigating with a global economic stagnation situation and a US economy pushing further. At one point or another, we will see other interest rate hikes in 2016 if the US economy continues to create jobs.

“I still think they are going to raise rates in March,” said Gus Faucher, a senior economist at PNC Bank. “I don’t want to oversell it, but I think that while what goes on overseas has an impact on the U.S. economy, what’s much more important is what goes on domestically.”

We now have Japan at 0, Europe at 0, Canada at its lowest interest rate ever (0.50%) and the US that just increased their rates in December. On one side, this is quite a signal that the economy can’t grow by itself at the moment and needs an urgent boost of liquidity. On the other side, it may prepare the table for a very strong bullish market. Those who are currently benefitting from this low interest rate environment will definitely create value in the upcoming years. Who else better than companies of the financial industry to do that?

Canadian Banks: Are they worth it for Americans?

As a Canadian investor, banks are now trending at very low levels meaning they pay a very high yield for such a stable sector. As of March 11th 2016, here’s how much 7 banks were paying in yield:

| Company Name | Ticker | Yield |

| Roybal Bank | RY.TO | 4.41% |

| TD Bank | TD.TO | 4.01% |

| CIBC | CM.TO | 4.87% |

| BMO | BMO.TO | 4.31% |

| ScotiaBank | BNS.TO | 4.65% |

| National Bank | NA.TO | 5.23% |

| Canadian Western Bank | CWB.TO | 3.81% |

As you can see, you can easily buy any bank and earn over a 4% yield. Even better, all the above banks are expected to raise their dividend year after year. Some of them even raise them twice a year. This sounds like a bargain for most investors and if you are looking to build a solid core portfolio, I think that Canadian banks should be part of it.

Now, for Americans, those who bought Canadian Banks in 2015 thinking the storm was over, many were hit by the currency exchange rate. At the moment, the USD has lost steam compared to the CAD and I believe this issue is behind us. In other words, Canadian banks are worth a look for both Canadian and American investors. The Big 5 (the biggest 5 banks) all trade on the NYSE under the “same ticker” (just take out the “.TO”).

I did a filter in the financial sector and I’ve pulled out all companies showing the following criteria:

- Dividend yield between 2% and 10%

- 5 year dividend growth positive

- 5 year revenue growth positive

- 5 years EPS growth positive

I decided to cover 6 CDN and 9 US dividend stocks in my most recent DSR premium newsletter. I’m sharing 2 of them here.

Canadian Western Bank (CWB.TO)

source: Ycharts

Based in Alberta, Canadian Western Bank went through its golden years since the 2000s with the exploitation of the oil sands in Northern Alberta. Now things are a little bit more difficult, pushing the stock price down by roughly 8% over the past 12 months. The good news in all this is that its dividend yield has never been so attractive, nearing the 4% bar (currently 3.81%).

While the market fears the worst in terms of credit deterioration for CWB, results so far have been surprisingly positive. CWB also managed to post loan book growth of 3% in its latest quarter. Even though the Alberta economy is seriously slowing down, CWB shows strong resilience.

Now that we see rising oil prices again, it might be the perfect time to enter a position in CWB if you are willing to take on more volatility in your portfolio. Still, this is a risky play.

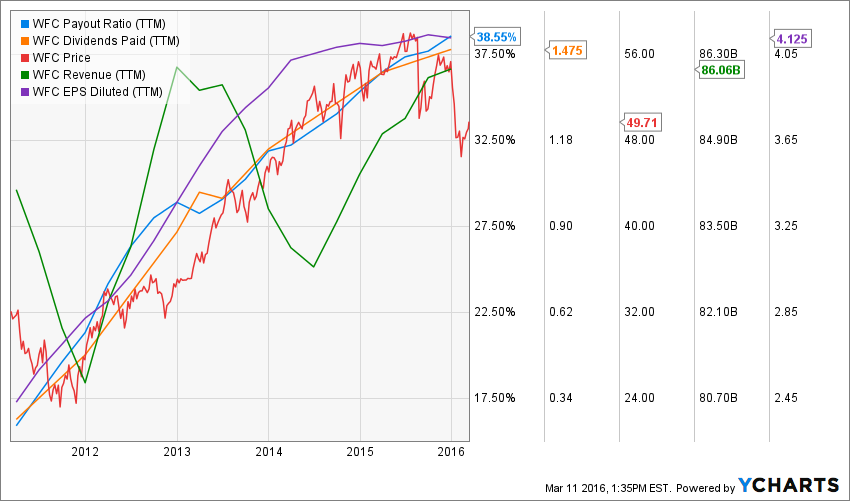

Wells Fargo (WFC)

Wells Fargo is a company offering financial services. It operates through 3 different segments: community banking, wholesale banking & wealth and brokerage & retirement. Wells Fargo is part of the famous Warren Buffett portfolio. WFC is one of the first banks to climb out of the 2008 financial meltdown.

The WFC business model is clean and simple. Most of its business comes from classic banking activities; savings and loans. The company has over 1 trillion in deposits and shows a very strong position to benefit from a rising interest rate.

The company has a strong history of risk management and its loan portfolio is well balanced between commercial (49%) and consumer (51%) loans.

We have a strong bank that is well situated on a nearly impossible-to-replicate competitive advantage. This ensures dividend growth for several years.

A Challenge! Can You Do It for a Month?

this whole project is making me crazy…

Now that I’ve passed the cap of the last 100 days before leaving for my one year RV trip, I’m starting to get seriously excited! It has been quite a challenging journey with my wife and children over the past 18 months and we haven’t even left yet!

Organizing such a trip is not only about setting up an itinerary and getting your gear ready for the big adventure. It’s not like packing your suitcase for a week in a five star hotel either. Organizing this trip starts with a journey within yourself. Over the past 18 months, I have changed my vision of several things. I gave more thought on how I live and how I really want to live. I have had to confront several of my fears and most of my beliefs.

Do I need all this stuff to be happy? I know I don’t, so why do I keep them?

More recently, I’ve discovered an enlightening truth; I’m working too hard keeping myself healthy all to destroy the work over the weekend.

It sounds a bit controversial but as hard as I workout every morning, 5 days a week, I also tend to enjoy drinking wine and having great meals on the weekends. It kinds of defeat the purpose. This is how I can run 6 km in 30 minutes, and still sport a good cushion hiding a potential six pack.

I took the first week of March off for our kids’ spring break. It was the perfect occasion to give some more thought about the way I live. Over the past couple of months, we have made several efforts to keep our budget low looking forward to travelling a complete year abroad. But there is one major expense that keeps rising on the top of our budget and this is food and wine. Our grocery budget has been a concern for a while as it is very important for us to eat healthy throughout the week. Therefore, our grocery bill includes mainly fruit, vegetables and fish. Three items that are not very cheap to say the least. We don’t eat prepared food, but eating fresh has its price. There is no way for us to cut on our health for the sake of financial freedom or saving more money. Still, we face this money management issue.

But now that I’ve had more time to think, I realized something; I eat way too much. Actually this is not true; I didn’t realize this just a few weeks ago. But for many years, I was hiding behind the fact that I’m working out. By working out 4-5 days a week, I always gave myself the right to eat and drink whatever I wanted over weekends. As I really enjoy cooking and eating, this was my way to reward myself for my weekday efforts. But as you probably know, if I want to burn my plate of red curry duck with a bottle of wine, I will have to run four hours just for this meal. Then, if I eat 2-3 meals like this over the weekend, I completely annihilate my weekdays’ effort. This is where I had to step up and take some serious decisions.

Here’s my Challenge; no wine (or anything else) for the next 30 days

I decided to cut out my wine consumption to a big zero for the next 30 days. My challenge actually started on March 4th (so I’m halfway there!). The point of cutting wine so drastically wasn’t the fact that I felt like I’m becoming an alcoholic (far from it), but a good meal comes with a good bottle of wine. Therefore, if I can’t cut the wine, I’ll cut some good meals (or at least, I won’t serve myself twice!).

I’m doing this challenge to prove to myself I can change my life habits. My goal is not to stop eating or drinking over the weekends, but I have the feeling that if I can cut everything down to zero, it will be easier to bring back a more acceptable level afterwards (such as one decadent meal per week).

I’m highly motivated to achieve my challenge because I have several reasons to do it:

It will help me keep a low budget before I leave for my trip;

It will create new life habits that will make my trip even more fun;

I’m working lots of hours right now, healthy food will keep my energy level very high;

I will spend 10 months out of 12 in T-shirt by the beach, I would rather look fit if I want to be in the pictures!

I think this is the main key to achieve any challenge: you need to focus on the benefits and the benefits must be bigger than the effort you make.

I’ve always worked out with the goal of being fit at one point in my life. When I was a kid, I was the chubby loner and I want to get rid of this picture. Due to my love relationship with food, this dream has always slipped through my fingers. I’m now giving myself the next three months to change my life habits in order to start my journey with a fresh new body.

What would be difficult for you to avoid in the next 30 days?

I think we become greater people when we learn to control our impulses. We all have our little demons. I’m curious to know what is yours?

8 Canadian Dividend Stocks that Are Buys Right Now

The stock market is definitely not a place for the faint of heart. At one point in time this February, the S&P 500 dropped by more than 10% (-10.51% on February 11th, 2016). On the Canadian market, the TSX dropped by more than 15% since its highest point in 2015. Now that we have been hearing more discussion about oil production stabilization from major oil countries, it seems both markets are on their way to recovering a good part of their drops. This is also a great opportunity to chase down bargains and make a few purchases. While the best timing might already be behind us, there are still good opportunities in this crazy market.

Recently, I reviewed 6 companies that raised their dividend within the first 2 months of the year. A reader of mine highlighted that only one company was Canadian (CNR.TO or CNI on the US market). This is why I decided to discuss a few great buy opportunities on the Canadian market in this article.

Royal Bank (RY.TO)

source: Ycharts

At the moment, Royal Bank is my favorite Canadian Banks. I even bought 29 shares to complete my children’s tuition fund in February. The reason why I bought RY.TO (RY for the US ticker) instead of buying another Canadian bank is linked to how RBC generates its revenues.

The company is a leader in capital markets and wealth management. Two sub-sectors poised for strong growth in the upcoming years. As Canada’s population is aging, fortunes are passing from the older generation and this new generation will face many challenges. This is why wealth management will become a priority for many families. The capital market sub-sector is more volatile than classic savings and loans activities. However, it is also a great source of growth for many banks. RBC has developed quite an expertise in this field.

At the same time, I tend to favor a bank that is less linked to classic savings and loans at the moment. Economic growth perspectives are inexistent for Canada in the upcoming two years mainly because of the oil industry. This will be a long period when consumers won’t borrow more than what they show on their balance sheet at the moment.

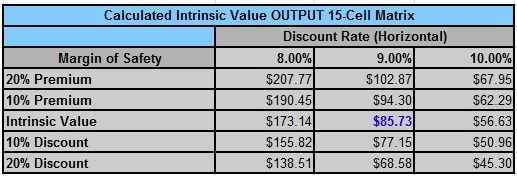

In order to be very sure of my purchase, I also use a double stage dividend discount model. After all, what really matters for me is the value of a company considering how much it will pay me back in dividends in the future. I didn’t go crazy with the dividend increase rate with a 6% growth rate for the first 10 years and I dropped it to 5% afterward. Here’s what my calculations look like:

| Input Descriptions for 15-Cell Matrix | INPUTS |

| Enter Recent Annual Dividend Payment: | $3.16 |

| Enter Expected Dividend Growth Rate Years 1-10: | 6.00% |

| Enter Expected Terminal Dividend Growth Rate: | 5.00% |

| Enter Discount Rate: | 9.00% |

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 8.00% | 9.00% | 10.00% |

| 20% Premium | $144.36 | $107.93 | $86.09 |

| 10% Premium | $132.33 | $98.93 | $78.91 |

| Intrinsic Value | $120.30 | $89.94 | $71.74 |

| 10% Discount | $108.27 | $80.95 | $64.57 |

| 20% Discount | $96.24 | $71.95 | $57.39 |

Source: Dividend Monk Calculation Spreadsheet

Finally, if I was looking at a smaller bank, I would probably go for Canadian Western Bank (CWB.TO). This bank is mainly based in Alberta and has benefitted from the oil boom. The bank has since then suffered from the oil bust and this may be the right time to enter in a position in a riskier play.

If you are interested in other banks, I’ve already covered the other members of the Big 5 at Seeking Alpha.

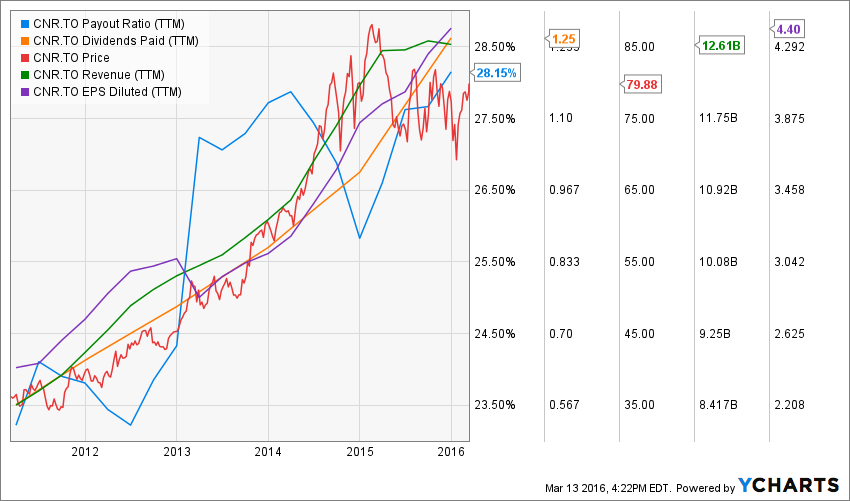

Canadian National Railway (CNR.TO)

source: Ycharts

It is no secret to anybody following this blog or being a member of Dividend Stocks Rock; I think Canadian National Railway (CNR.TO) offers a very good buying opportunity. I even purchased some shares myself towards the end of 2015.

If there is only one reason to buy CNR.TO (CNI if you look for the US ticker), it is probably the fact that there are no other railway operators in North America with such low operating margins. We all know how costly it is to build, manage and maintain railways each year while truckers don’t have to pay a penny to construct highways. This is where Canadian National Railway has become the top of the line railway operator with an operating margin of 54% last quarter. In comparison CP.TO is at 59.8%, CXV at 71.6% and UNP at 63.2%.

But if you need more reasons, here are plenty:

- 5 year revenue growth of 11.22% CAGR 5 year EPS growth of 14.64% CAGR 5 years dividend growth of 15.40% CAGR

Very low payout ratio of 27.39%

Since CNR evolves in a fairly stable and predictable market, I will use a discount rate of 9%. As for dividend growth, I use a 10% rate for the first 10 years and reduce it to 7% to be more conservative. The 10% dividend growth for the first 10 years seems aggressive at first, but considering the company increased it by 15% CAGR over the past 5 years, I think that using 10% for the first 10 years is a fair assessment:

Source: Dividend Monk Calculation Spreadsheet

Source: Dividend Monk Calculation Spreadsheet

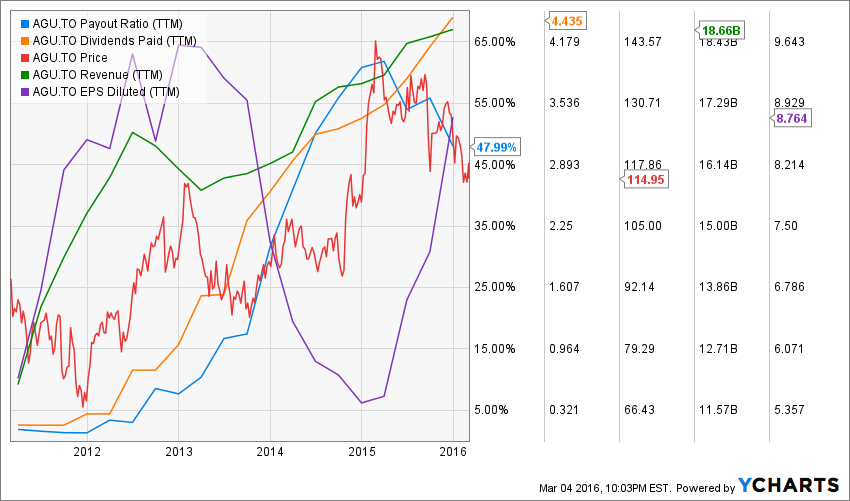

Agrium (AGU.TO)

source: Ycharts

Agrium is another of my recent buys for my retirement portfolio. This stock is also part of my Canadian Growth Dividend Portfolio beating my benchmark by over 10% since its creation (you can see my performance here).

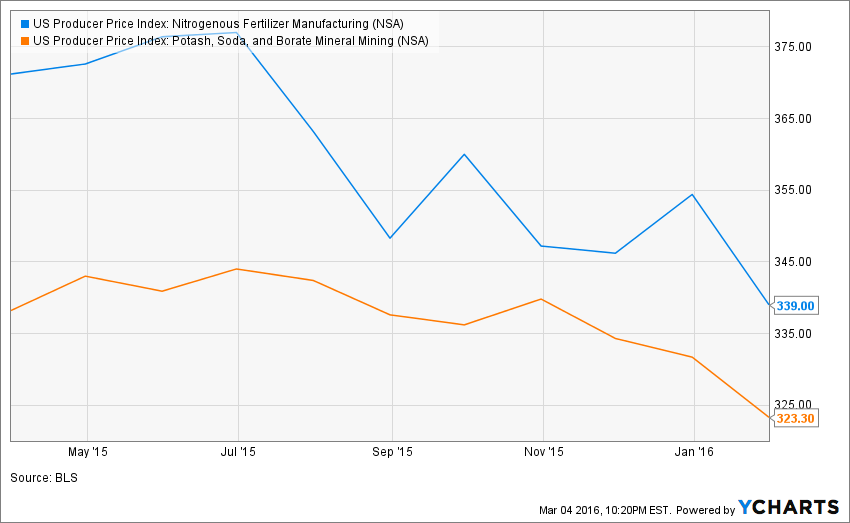

AGU.TO (AGU for US investors) is another stock taking a serious beating being -15% over the past 12 months or so. The price of potash dropping, global economic slowdown and less demand coming from emerging markets contributed to making AGU a great buy opportunity at the moment.

The company isn’t without risk as I just highlighted them. However, its retail business (it also sells many products to farmers on top of fertilizer) enables the company to support rougher period. Compared to Potash (POT.TO or POT) which recently cut its dividend by 34% early in 2016, AGU increased its payout from $0.99 to $1.21 within 2015 through a dividend increase each quarter of the year. Now we are talking about a confident management team! The best of all is that AGU’s payout ratio remains in control around 50%.

With the Chinese Government announcing various plans to boost up its economy, we can expect a potash price rising in the upcoming years and AGU will head to the top again.

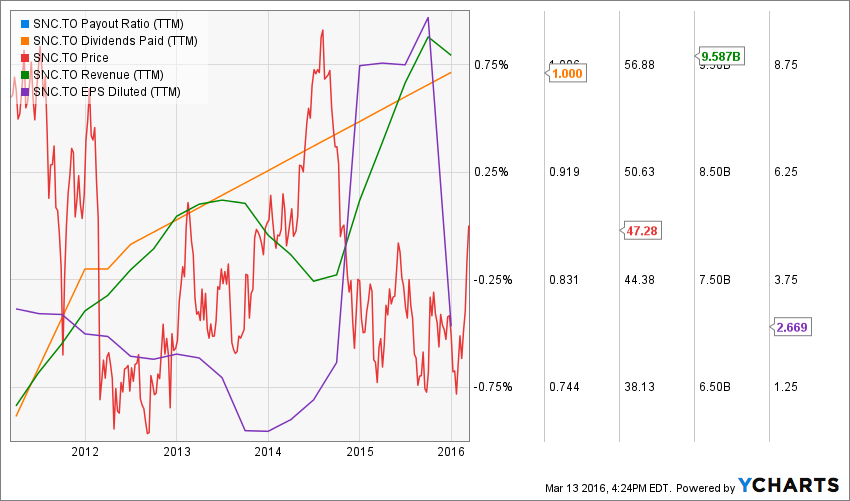

SNC Lavallin (SNC.TO)

source: Ycharts

Do you remember me selling my shares of Scotia Bank (BNS.TO) to buy SNC Lavallin last year? Let’s go back in time and read this article again. I was somewhat challenged by readers (and that’s what I like to be honest) but I was rather called out for profanity on Seeking Alpha (they picked up my article and republished it on their site). I like making bold moves when they make sense. SNC.TO isn’t a big part of my portfolio, but I found (and still find!) more value into SNC right now than BNS. It’s been almost a year and I have proven to be right so far:

SNC is up 19.96% since I wrote my article and BNS is down 6.26%. This excludes dividend payments, but still, it would come down to the same result; SNC is seriously doing better than BNS.

The company published better than expected results in their most recent quarters leading analysts to increase their target for the engineering firm. This is the main reason why the stock is up so high recently. Not to mention the future looks brighter than before: At the end of 2015 SNC had a $12 billion backlog, and in the first 60 days of 2016 added $1.3 billion contract at the Darlington Nuclear Generating Station and an $800 million contract in the Middle East for its oil and gas division.

Gluskin & Scheff (GS.TO)

source: Ycharts

Gluskin & Scheff has taken a serious beating over the past 12 months. The stock is currently down by over 25% since January 2015. At least, the company paid $1.59 per share in dividends in 2015. This translates to a 7.81% yield based on the current stock price. You know that I’m far from being a fan of high dividend yield. However, Gluskin & Scheff high dividend yield is linked to its semi-annual special dividend based on performance fees. While it makes the dividend yield fluctuate, it doesn’t impact its payout ratio that much as the special dividend is paid according to how good management was.

While some analysts were expecting a special dividend as high as $0.56 per share, they were disappointed to see a special dividend at $0.10. This is on top of its quarterly dividend of $0.25. In 2015, the company paid a total of $1.575 per share for a yield of 8.70% based on a stock price of $18.11. The first dividend of 2016 is then $0.35 compared to $0.83 a year ago. Assets under management (AUM) are not doing so well with a reduction of 1% for $75 million of net outflows. However, the company shows a higher AUM in December 2015 ($8.307B) compared to December 2014 ($8.220B). As I previously mentioned, the stock price has taken a beating for the past 12 months and I think it is unjustified. The “hole” in their revenue ($69M vs $58M this year) is due to a drop of $10M in performance fees. It is hard to expect the company to outperform in such volatile markets when the Canadian market suffered in 2015. On the other hand, this makes GS a great contender for an acquisition by a larger wealth management firm…

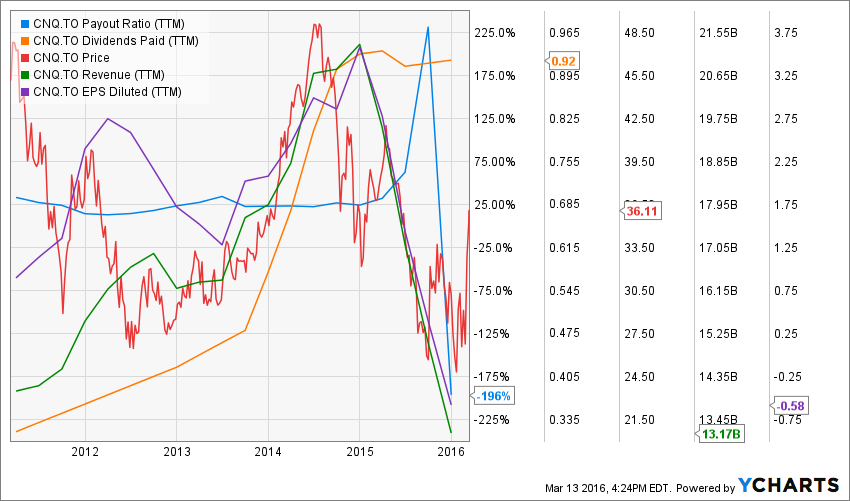

Canadian National Resources (CNQ.TO)

source: Ycharts

CNQ is one of Canada’s largest oil & gas exploration and production companies. The company shows a strong history of adapting to this ever changing environment and allocating capital accordingly. In order to support its cash flow, the company recently sold its third-party royalty assets to PrairieSky Royalty (PSK.TO) for $1.8 billion dollars. The Horizon oil sands project is expected to generate substantial and continuous cash flow for the company, securing at the same time its dividend payment even considering a very high payout ratio. As you can see, we are currently focusing on cash flow generation to support dividend payments rather than use a more classic metric in the payout ratio. Over the long run, this analysis is not sustainable (a company must make a profit at one point if it wants to keep increasing its dividend). However, while facing many headwinds, what remains the most important thing to analyze is a company’s ability to generate cash flow. This is the heart and blood of the company. CNQ is in a very good position to generate cash flow at the moment.

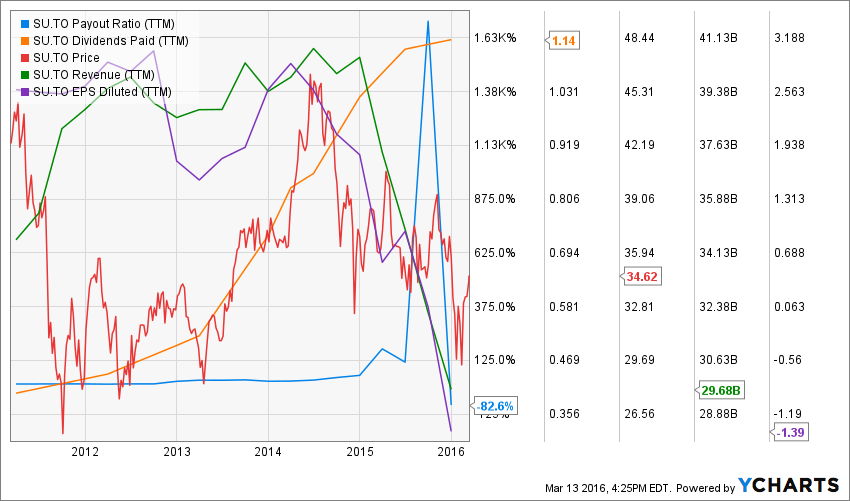

Suncor Energy (SU.TO)

source: Ycharts

Suncor Energy is Canada’s leading integrated oil and gas producer, generating superior refining margins and strong price realizations, which help offset higher-than-average operating costs at some of its upstream operations. Similar to COS, Suncor is sitting on a huge oil sand resource. It has the ability to produce barrels of oil for decades. This asset leads to low-cost plateau production. Such activity will continue to generate a consistent cash flow, securing future dividend payments despite a current payout ratio that is out of the norm. Suncor has become an integrated oil company with an enviable portfolio of oil sands assets. This is why its stock price hasn’t been affected too much over the past 2 years compared to its peers (only -10%). The company keeps pushing towards the top as they recently tried to acquire COS.TO with a hostile bid. Both companies finally agreed toward the end of January to a $4.2 billion deal.

I’m sure there is more! Now it’s your turn!

All right, I think I’ve shared enough for today. What do you think of my picks? Which other stocks do you have on your radar?

disclaimer: I hold shares of RY, CNR, AGU, GS, SCN in my Dividend Stocks Rock portfolios.

The opinions and the strategies of the author are not intended to ever be a recommendation to buy or sell a security. The strategy the author uses has worked for him and it is for you to decide if it could benefit your financial future. Please remember to do your own research and know your risk tolerance.

New Purchase: Agrium

While I’m done with my children’s tuition fund, I had a few dollars uninvested left in my retirement portfolio. Agrium (AGU) has been on my watch list for a while and I decided to enter in a position on February 26th. Please note that Agrium is trading on the TSX as AGU.TO and on the NYSE as AGU. All figures in this article is in Canadian dollars to avoid any confusion.

I purchased 13 shares of Agrium (AGU)

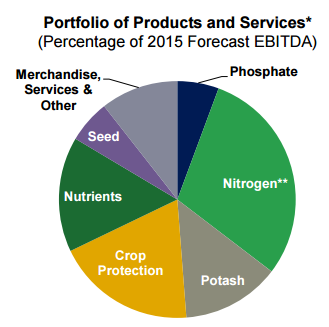

Agrium is the largest global retail and distributor of crop inputs. It is also the leader of agricultural nutrients providing farmers with all they need to improve their production. The company shows a less dependent link to potash prices as it counts on other products such as:

Source: Agrium investor presentation May 2015

This is probably the reason why Agrium saw its profit jump by 24% in 2015 while Potash (POT) saw theirs down by 17%…. No wonder Potash cuts its dividend while Agrium’s dividend payment is safe with a payout ratio under 50%.

Investment Thesis

The fact that the ratio of arable land per person is continuously declining puts constant pressure on farmers to become as efficient as possible. The first solution for farmers is to improve their production with additional fertilizer. A second solution is to protect the crops they own and make sure their land is protected from any catastrophe that would affect their production. The consumption of meat in emerging markets will continue to increase in the upcoming year putting additional pressure on farmers to become even more productive. Agrium retail business will continue to overcome the drop in commodity prices for Potash and Nitrogen.

source: ycharts

Another interesting opportunity for Agrium is the fact that the retail agriculture market is highly fragmented. A leader such as Agrium can then easily swallow smaller competitors and ensure continuous growth in the upcoming year. Not to mention the low price of commodities have been hard for many of AGU peers. Being bigger in such markets will lead to improved bargaining power with suppliers and farmers.

Finally, with a 4%+ dividend yield and a relatively low PE ratio (12.31), the stock shows a great entry point at this time.

Risk

I didn’t put an enormous amount of cash into AGU just yet. In fact, this company represented roughly 2.5% of my portfolio at the moment of buying. The reason is quite simple; the high commodity price volatility hurts the company profit and cash flow from time to time. Also, the health of Agrium’s nitrogen business is closely tied to the cost of natural gas. If natural gas prices rise, it would create additional pressure on margins.

This is a volatile stock compared to most dividend growth companies. For example, AGU dropped by 20% while the TSX dropped by only 13% over the past 12 months.

Valuation

As I previously mentioned, I think AGU’s low PE ratio is a very good entry point at this time:

I usually use a 10 year PE ratio history to make my mind on what multiplier is used by the market, but the anomaly of 2007 (the PE ratio went up close to 200) makes it impossible to analyze on such long period. On the other hand, the enormous drop to a PE ratio near 8 in 2012 is related to the potash price collapse. Since 2014, the stock hasn’t been any cheaper.

In order to have a better idea of what AGU’s intrinsic value is, I use a double stage dividend discount model (DDM). This enables me to use a 8% dividend growth rate for the first 10 years and reduce it to 7% afterward. I also use a 11% discount rate considering the high volatility of commodity prices:

| Input Descriptions for 15-Cell Matrix | INPUTS |

| Enter Recent Annual Dividend Payment: | $4.84 |

| Enter Expected Dividend Growth Rate Years 1-10: | 8.00% |

| Enter Expected Terminal Dividend Growth Rate: | 7.00% |

| Enter Discount Rate: | 11.00% |

I’ve updated my calculations with the most recent dividend increase in December at $1.211 (CAD) per share:

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 10.00% | 11.00% | 12.00% |

| 20% Premium | $225.19 | $168.38 | $134.32 |

| 10% Premium | $206.42 | $154.35 | $123.13 |

| Intrinsic Value | $187.66 | $140.32 | $111.93 |

| 10% Discount | $168.89 | $126.28 | $100.74 |

| 20% Discount | $150.13 | $112.25 | $89.55 |

Source: Dividend Monk Calculation Spreadsheet

As you can see, the company is trading at almost a 20% discount (which is where its price was 12 months ago). This is an opportunity I couldn’t ignore.

What do you think? Are you one of investors who preferred Potash not so long ago?

disclaimer: I own shares of AGU

My Magic Recipe to Overcome Any Obstacle

There are ten good reasons I am never going to make it…

You probably know by now that I’m a man of passion and projects. I’m still pretty young (34) but I’ve overcome many obstacles in my life. I wouldn’t say I have done something extraordinary, and I have accomplished many things people around me thought impossible to realize. Thought… that’s what they used to say.

You can’t do that… not now… not you… you’ll have to wait…

I don’t know about you, but I have the impression of hearing these excuses a thousand times. But each time I have heard this in my life, it was like someone just pressed the wrong button. If I was told it was impossible; this was just the reason for me to go ahead and do it. Over the past 15 years, I’ve done many things I’ve been told I shouldn’t / couldn’t do, such as:

- Getting a brand new car and leaving the folk’s nest without a source of income (my dad told me I didn’t have the guts);

- Quitting my first job (and getting stuck with the car and apartment payments) without a new job in sight;

- Getting a job where everybody speaks English except me (I’m French Canadian...);

- Going from a “head office job” directly to a high position in a “field job” (I was told I needed to “take additional classes”);

- Making money with a finance blog (back in 2006, people were laughing at me!);

- Changing jobs, completing my MBA and doing my CFP title all in the same year (all right, this one was just crazy!);

- Telling my boss I will now work 4 days (30 hours) a week with the same paycheck (in a job where people usually do 50 hours/week);

- Telling my boss I’m taking a sabbatical to travel (in a job where the word “sabbatical” is synonymous with “career suicide”).

All these moves (and more) were not something I was supposed to do. They weren’t supposed to be done in our “industrial” world. But all these moves have made me a better person and I have been rewarded with a “better” life. However, each time I plunged, it felt wrong.

Maybe it’s because we are raised this way, we are being told to:

Be a good boy and listen in class;

Work hard to get good marks;

Head for a good position in a good company;

Work harder to get promotions;

Wait until your boss retires;

Work even harder to get his job;

Retire with a full pension plan.

I’m not laughing at this “career trajectory” as I’ve followed it to the letter…. until I realized what I was doing wasn’t right for me. I’ve always tried to keep an open mind for new projects. I think that the routine is not for me ;-).

Excuses, excuses, excuses…

After writing about my final itinerary the other week, I realize that many readers envy my project and find themselves unable to achieve their own dream (regardless if it was similar to mine or not). The main reason is because we tend to focus too much on the reasons not to do something instead of focusing on the ways to do it.

I can’t go to the gym, I am too tired;

I can’t take a sabbatical, I have bills to pay;

I can’t eat healthy at home, I arrive from work too late;

I can’t travel, I have young kids and they can’t miss school;

I can’t read a good book; I am too busy working, cleaning or… resting!

When we first thought of our travel project, we also make sure to cite all these excuses to not do our trip. Then, I started to think about it differently…

Here’s my Magic Recipe to Overcome Any Obstacle!

A recipe is usually a list of steps to follow along with a list of ingredients to use. In this case, the recipe is quite easy as it includes only 2 words:

WHAT IF?

Two simple words forming a simple question: what if?

When I was a kid, I was a big Marvel Comic Book fan. For those who are like me, you’ll surely remember the marvelous X-men series: “The Age of Apocalypse”. Along the side of the series, there was one that was lots of fun called “What If?”. This was a series where writers were totally wild and could do whatever they wanted. They could think of any possible alternate reality without any constraints.

This is exactly what I’m trying to do when I plan my projects from now on. I put all the obstacle aside and start thinking “what if it was possible? How would I do it?”

This is the moment when you start working on your project instead of worrying about what is impossible to achieve. By working on your project and thinking how you would do things if they were possible, you will open your brain to find solutions. Then, solutions will appear one after the other and you will not even have to think about it.

This is how we figured out how to finance our trip, how to take care of our house while away and how to travel for one year with our kids.

Two years ago, I didn’t have the money to travel…but I started working harder on my websites.

I wasn’t able to sell my house without losing money… but I found someone to rent it and cover my costs.

I didn’t know how to travel for one year with a limited budget… then we found that traveling in a RV was cheap… and fun!

By putting all the reasons why you can’t do something aside, you open yourself to a world of possibilities. This is the same rationale used when you brainstorm. All ideas are good ideas at this point. One crazy idea could eventually lead to something that makes sense. Can you believe that the idea of travelling came from a family of 5 that left Canada to go to Mexico by bicycle? We started to imagine ourselves with a tent on our back and three kids whining after doing 20km…. and here we are with a fully planned trip two years later!

What is your trick to overcome obstacles? Have you tried the “what if” method before?

© Copyright 2013 Adividend