Yesterday, I posted my review of the earnings for both BMO and Scotiabank. My one word was “meh!” This time, both banks have reported flat earnings and pretty good results. What’s happening?

BMO earnings were down around 20% and ScotiaBank was down roughly 47%. Then National Bank and Royal Bank were minus one or flat. There is something wrong. Let’s dig a little deeper and see what’s really hiding behind these reports.

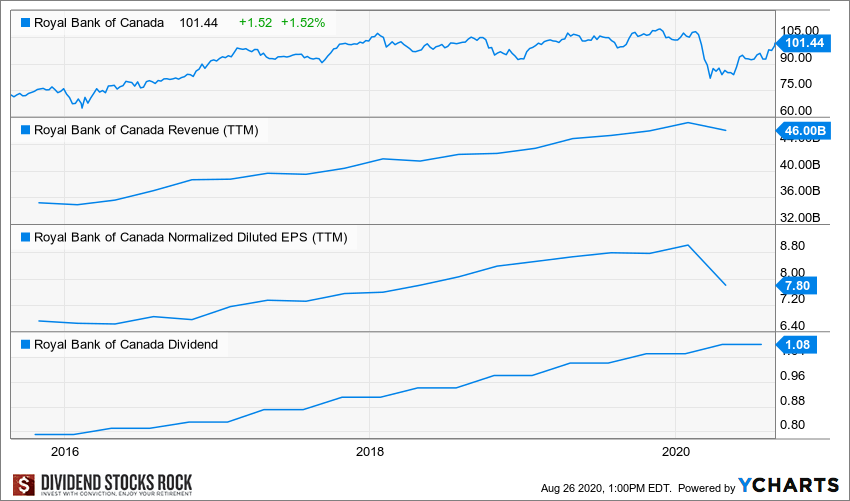

Royal Bank (RY) (RY.TO)

Business Model

Royal Bank is the largest bank of the group by market cap (it battles with TD) and provides various financial services to individuals as well as commercial and institutional clients. RY has a strong position in the personal and commercial banking sector (46% of its revenue). In 2015, RY bought City National, a Los Angeles-based bank focused on high net worth clients. The transaction opened US doors and another growth vector: wealth management.

What’s the Story?

“We continue to navigate these uncertain times from a position of strength and stability. Our robust capital and liquidity position, diversified business model, prudent approach to risk management, and technology capabilities provide the foundation to enable our people to continue supporting clients, providing advice and creating more value today and over the long-term,” said Dave McKay, RBC President and Chief Executive Officer. “RBC has a proud history of helping our clients thrive and communities prosper. Since the onset of the COVID-19 pandemic, RBCers have shown their unwavering commitment to delivering on our Purpose by enabling the re-emergence of our economies and supporting our clients with empathy and dedication.”

Source: RY Press Release

Basically, CEO is telling you “COVID-19 has unknown impacts on the economy, but we’re good banks, so trust us.” What caught my attention was that he mentioned that he’s focusing on prudent approach to risk management. That’s really Royal Bank’s type of statement, saying they’re pretty much sitting on their throne and wait because they’re the biggest bank across Canada along with TD.

Now let’s dig into the numbers.

- Net income $3.2B, -2%

- Adjusted EPS $2.20, -1%

- CET ratio is at 12 (+30 points)

Business as usual, right? But it’s kind of weird during a pandemic crisis! That’s when you find out why. Provision for credit losses is at only 675 million, versus 2.83 billions in April. They were quite aggressive back in April, but they just add another 700 million as provision for losses, which is not too much…

Interesting enough, 7% of RY total loans are vulnerable to COVID-19 economy impacts. BMO and Scotia Bank were between 4% and 5%. Even with more risk exposure, RY chooses to go with a smaller provision for credit losses. Is it a sign that something is wrong or is it just good accounting? We should follow that in the next quarters.

Also, less than 50% of Royal Bank business is concentrated in the classic personal and commercial banking. RY relies a lot more on capital markets, wealth management and insurance to make money, and this is paying off.

Investment Thesis

Over the past 5 years, RY did well because of its smaller divisions acting as growth vectors. The insurance, wealth management, and capital markets push RY revenue. Those sectors combined now represent over 50% of its revenue. During the COVID-19 pandemic, these are also the same segments helping Royal Bank to stay the course. Royal Bank also made huge efforts into diversifying its activities outside Canada. Canadian banks are protected by federal regulations, but this limits their growth. Having a foot outside of the country helps RY to reduce risk and to improve growth potential. Royal Bank shows a perfect balance between revenue growth and dividend growth. It’s a keeper.

Potential Risks

After the 2018 financial market crash, the bank put its focus on growing its smaller sectors. While wealth management should continue to post stable income, the insurance and capital markets are more inclined to hectic returns. As the largest Canadian bank, Royal Bank could also get hurt by a bearish housing market. There are some general concerns around Canadian Banks and how they manage their provision for credit losses. RBC loan portfolio has been affected by the pandemic, but provision for credit losses has been smaller for Q3 2020 vs Q2 2020. We will have to wait for this fall to see if the economy will suffer from another virus outbreak.

Dividend Growth Perspective

Royal Bank has a “tradition” of increasing its dividend twice a year. In normal times, you can count on two low-single digit dividend growth per year. It paused its dividend growth policy between 2008 and 2010, but came back with the double dividend growth tradition in 2012. The bank is likely to follow a similar strategy and should pause its dividend growth policy for the rest of 2020 and potentially 2021. We will follow the situation closely. In the meantime, the dividend is safe as the payout ratio remains under control.

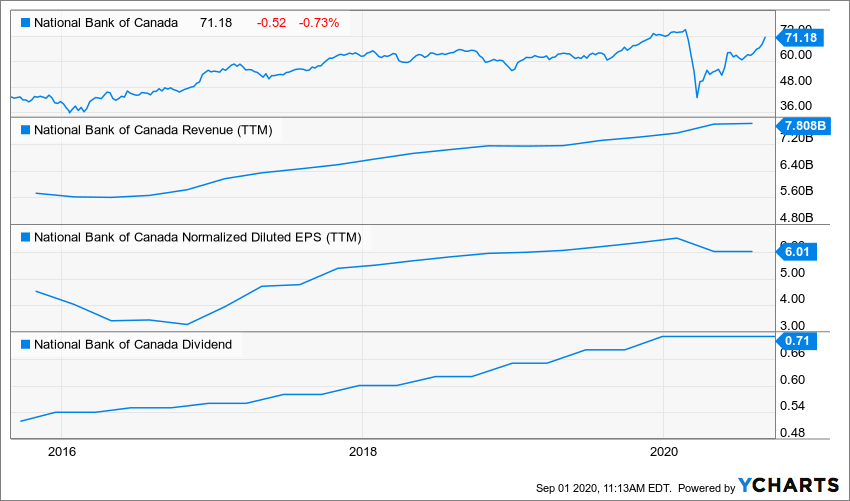

National Bank (NA.TO)

Business Model

National Bank is very small compared to the big 5 Canadian banks. As the sixth largest one, NA is mostly in Quebec with 62% of its revenues earned in this province. Its smaller size is currently paying off as National Bank was quicker to develop a strong brand in Wealth Management with Private Banking 1859 and built a highly profitable Financial Market division.

What’s the Story?

“Since the gradual reopening of the economy, many indicators have improved, but the situation remains uncertain, especially given the potential for a second wave of the COVID-19 pandemic. In this environment, the Bank is continuing to deploy efforts to support its employees, its clients, and the community,” said Louis Vachon, President and Chief Executive Officer of National Bank of Canada.

Source: NA Press Release

Lots of uncertainty, but he’s focusing on a strong position, solid balance sheet, defensive position, and he’s highlighting quality credit portfolio and prudent approach to provising (you can read full statement here).

National Bank did exactly the same as Royal Bank with their provision for credit of losses. They went from 500 millions in April to 143 millions.

According to their presentation, 3.7% of their loan portfolio could be called as vulnerable, which is not too much. However, the energy sector is not included. National Bank seems to be trying to look good. While I get why they do that, it’s a little shaky.

I’m going to go deeper and look into that in the next days and you should too if you are a shareholder.

Now let’s dig into the numbers.

- Net income $602M, -0.99%

- Adjusted EPS $1.66, flat

- CET ratio is at 11.4 (flat)

Again, these results seem questionnable in the actual context. However, NA got growth from international exposure. Obviously, the exposure of international banks for NA is a lot less than ScotiaBank, but last year they completed the purchase of ABA Bank in Cambodia, and this is what brought a lot of this growth for the quarter.

They also have a great financial market and wealth management division, up by 5% and 2%. So far, banks have been dragged by classic personal and commercial banking. Those doing better do it with capital markets wealth management, international exposure or insurance.

Investment Thesis

Like BMO, NA aimed at capital market and wealth management to support its growth. Private Banking 1859 has become a serious player in that area. The bank even opened private banking branch only in Western Canada to capture additional growth. Since NA is heavily concentrated in Quebec, it concluded deals to do credit for investing and insurance firms under the Power Corporation (POW). Branches are currently going through a major transformation with new concepts and enhanced technology to serve clients. While waiting for the results, it seems wise to invest in digital features to reach out to the millennials and improve efficiency. The stock has outperformed the Big 5 for the past decade as it showed strong results. Recently, NA is seeking additional growth vectors by investing in emerging markets such as Cambodia (ABA bank). Can it have more success than BNS on international grounds?

Potential Risks

National Bank is still highly dependent on Quebec’s economy. As a “super-regional” bank, NA is more vulnerable to economic events. So far, the covid-19 situation in Quebec as been well managed and NA posted satisfying results in May 2020. However, we are far from being done with the pandemic. Capital markets revenues are also highly volatile. NA could run into a bad quarter if the stock market enters into a bearish environment. The bank has considerable exposure to the oil market through its commercial loan portfolio. Overall, the bank performs very well, but usually take a little more risk to find growth vectors (such as ABA bank investment and capital markets). So far it has paid well, but it doesn’t mean it will always work.

Dividend Growth Perspective

National Bank offers a generous dividend growth policy. The bank has shown one of the most generous dividends increase in the past 5 years (vs the other Big 5). Not bad considering the company had to take a pause in its increase between 2008 and 2010 due to the financial crisis. The bank should pause its dividend growth policy in 2020 and wait to know the full impact of the pandemic on its loan portfolio. So far, it seems that NA can easily navigate through this challenge. However, we are far from being done and we must wait a few more quarters (ready beginning of 2021) to understand the full impact of the covid-19 on the economy.

Final Thoughts

In both cases, we have a decent payout ratio and a robust balance sheet. I don’t expect any cut from these two banks for the upcoming quarters. They will probably reassess as the economy recovers in 2021, but in the meantime, as an investor, I don’t mind what’s happening. I’m happy with those results, they fit with my investment strategy and my investment thesis for both banks, and I’m just going to keep holding them.

Disclaimer: I do hold shares of NA.TO (NTIOF) and RY.

The post Canadian Banks are Doing Well! – National Bank and Royal Bank Q3 2020 Earnings Review appeared first on The Dividend Guy Blog.