If you feel uncomfortable about the market right now, utilities should not get you worried too much with their strong yield and their decent dividend growth! There are some great utilities on the Canadian side and today I’ll go through my Top 4!

Note that this article is part of my “Utilities series”. First, we’ve covered What Are Utilities and Why You Should Hold Some, then I went through the best Renewable Energy to invest in the future and the upcoming post will be about the Best US utilities available.

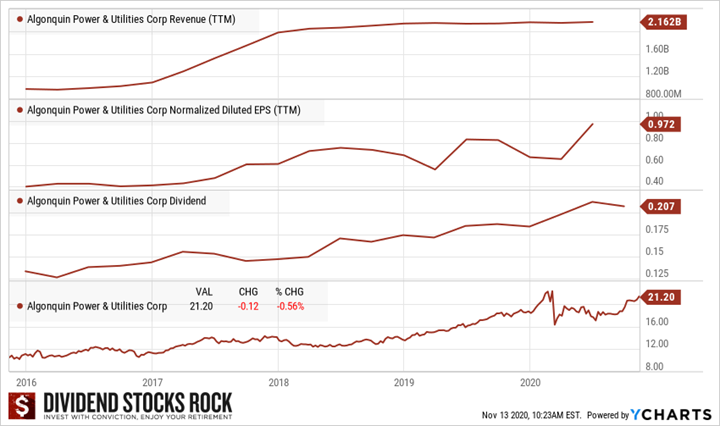

Algonquin Power & Utilities (AQN.TO) (AQN)

Algonquin Power & Utilities Corp is a North American generation, transmission, and distribution utility. Within its distribution group, Algonquin owns and operates regulated water, natural gas, and electricity distribution utilities in the United States. Most of the company’s revenue is derived from this division and, in turn, most of this division’s revenue comes from its distribution of natural gas. In its generation group, Algonquin sells electricity produced by its energy facilities, including hydroelectric, wind, solar, and thermal power plants. Algonquin’s wind farms account for most of its generation revenue. Finally, the company’s transmission group focuses on building and investing in natural gas pipelines and electric transmission systems.

Investment Thesis

Like many utilities, solid growth is coming from outside the company. AQN had about 120,000 customers in 2013 and now serves over 762,000. It achieved this impressive growth through acquisitions, and the largest one was Empire District Electric for $3.4B completed in early 2017. With a budget of $9.2B in CAPEX, AQN has several projects coming on stream through 2024. These include more acquisitions, pipeline replacements and organic CAPEX. The utility counts on its regulated business to grow its revenue once those projects are funded. AQN shows a double-digit earnings growth potential for the foreseeable future, but we expect a short-term slowdown due to the economic lockdown.

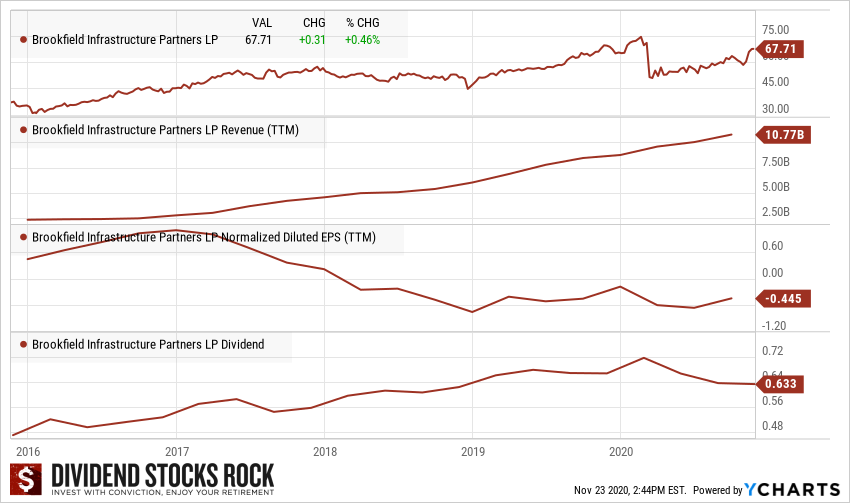

Brookfield Infrastructure Partners (BIP.UN.TO) (BIP)

Brookfield Infrastructure Partners LP is a Bermuda exempted limited partnership that owns and operates quality, long-life assets that generate stable cash flows, by virtue of barriers to entry or other characteristics that tend to appreciate in value over time. It focuses on acquiring infrastructure assets that have low maintenance capital costs and high barriers to entry. The company’s segments consist of Utilities, Transport, Energy businesses, and Data Infrastructure.

Investment Thesis

BIP has built an impressive portfolio of infrastructure through various business segments: utilities, transportation, energy and data infrastructure. The company manages 2,700km of regulated natural gas pipeline, 2,200km of electricity transmission, 32,300 km or railroads, 4,000km of toll roads, 13 ports,16,500km of natural gas pipeline, 20,000km of fibre backbone and 51 data centers. While revenue may slowdown amid the pandemic, Brookfield has $3B in liquidity, no significant debt maturities in the next 5 years and it is backed by Brookfield Assets Managements (BAM). You now have the option to trade Brookfield either as a limited partner or corporation. Please see your accountant for more details.

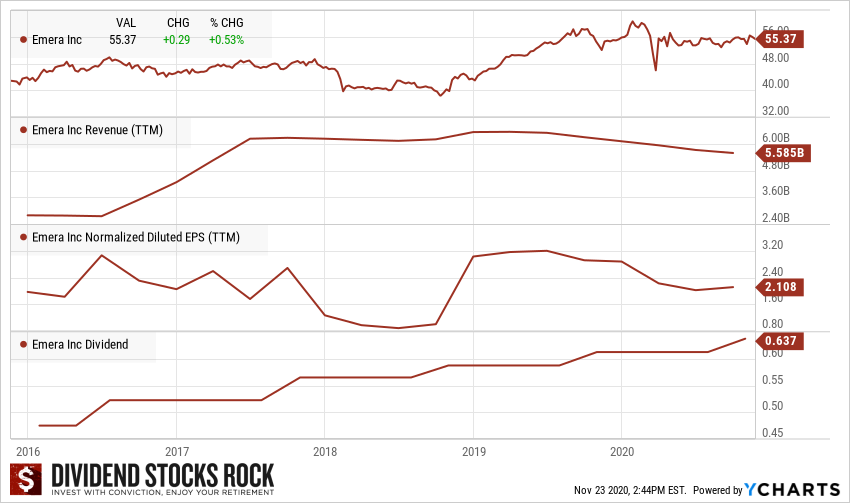

Emera (EMA.TO)

Emera is an energy and service company. Emera’s main market is Nova Scotia as it owns Nova Scotia Power, the province’s main electricity provider. Emera owns power plants and distributes natural gas in Canada, the USA, and the Caribbean. This utility employs over 7,400 workers and serves more than 2.5 million customers. The utility company now manages a regulated portfolio of $32B worth of assets with 65% of its earnings coming to the U.S.

Investment Thesis

Emera is a very interesting utility with a solid core business established on both sides of the border. EMA now shows $32 billion in assets and will generate revenues of about $6.3 billion. It is well established in Nova Scotia, Florida, and four Caribbean countries. This utility counts on several “green projects” with hydroelectricity and solar plants. Between 2020 and 2022, management expects to invest $7.5B in new projects to drive additional growth. This decreases the risk of future regulations affecting its business as the world is slowly moving toward greener energy. The company recently sold Emera Main and received $963M (USD) in March 2020. This improves its financial flexibility and ensure funding for future projects.

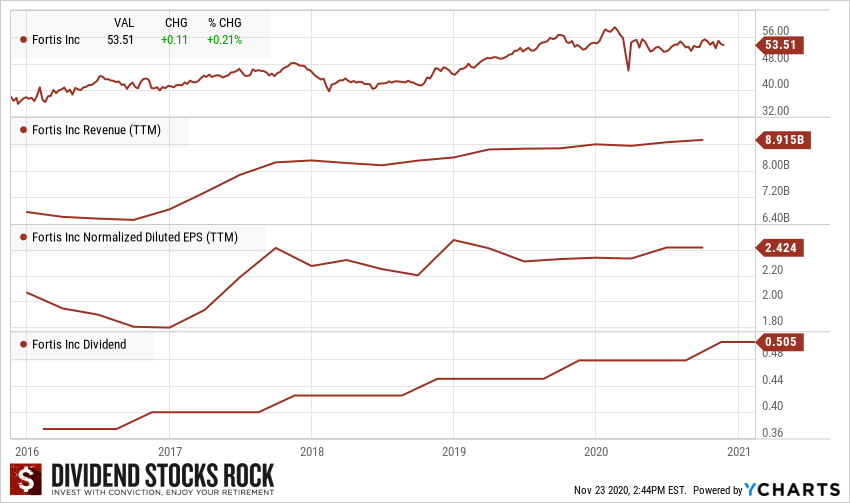

Fortis (FTS.TO) (FTS)

Fortis owns and operates utility transmission and distribution assets in Canada and the United States, serving more than 2.5 million electricity and gas customers. The company has smaller stakes in electricity generation and several Caribbean utilities. ITC operates electric transmission in eight U.S. states, with more than 16,000 miles of high-voltage transmission lines in operation. The company generates about 66% of its earnings outside of Canada.

Investment Thesis

Fortis aggressively invested over the past few years resulting in strong and solid growth of its core business. You can expect FTS revenue to continue to grow as it is expanding. Strong from its Canadian based business, the company can generate sustainable cash flow leading to 4 decades of dividend payments. The company has a five-year capital investment plan of approximately $14.5 billion for the period 2018 through 2022, which is up, $1.5 billion from the prior year’s plan. Chances are most of its acquisitions will happen south of our border. FTS yield isn’t impressive for a utility (~3.50%), but there is a price to pay for such a high-quality dividend grower.

Some More Comments about My Top 4

Above, I shared my investment thesis. However, I went deeper into each business model and the reasons why I picked them as the “top” canadian utilities in the video right below. I believe you’ll find lots of value in this full analysis.

Using Utilities as “Deluxe Bonds”

Disclaimer, I hold Emera (EMA.TO) and Fortis (FTS.TO) in my personal portfolio as what I like to call “deluxe bonds”. This means I will have limited stock appreciation but strong yield and decent dividend growth. To me, this is exactly what Canadian utilities can do for you in a portfolio: they will be your stabilizers. No matter what happens on the market, you can count on those dividend payments.

The post Best Canadian Utilities: My Top 4! appeared first on The Dividend Guy Blog.