The U.S. Market is beating all odds!

Source: Ycharts

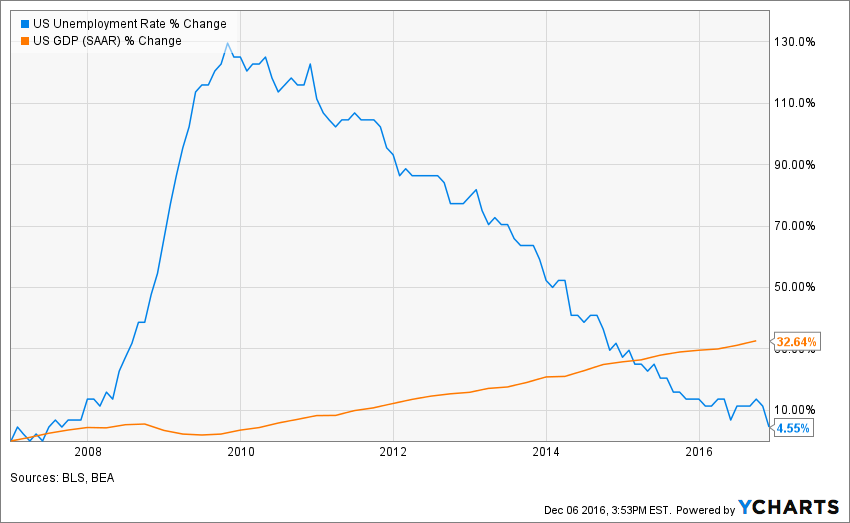

I like this graph as it shows the pre and post situation of 2008 for unemployment rate and GDP. We can clearly see how the unemployment rate jumped drastically following the credit crisis and how the GDP slowed down during the same period. However, while the GDP slowly started to grow again, jobs recovery seemed to be a lot faster. Now fast forward in 2016, we now have a GDP 33% stronger than at the end of 2006 and an unemployment rate solely 4.55% higher. In other words, the U.S. economy hasn’t been affected that much by the 2008 crisis as it rapidly recovered a steady growth. As for jobs, they were quick to disappear and the impact on people was disastrous. Fortunately, what we first saw as a bunch of “Mcjobs” created in the post-2008 economy founded the basis of a more solid employment situation. 8 years after the crisis, we can’t claim there were only minimum wages created during this period. Good jobs are also being offered on the market.

Source: Ycharts

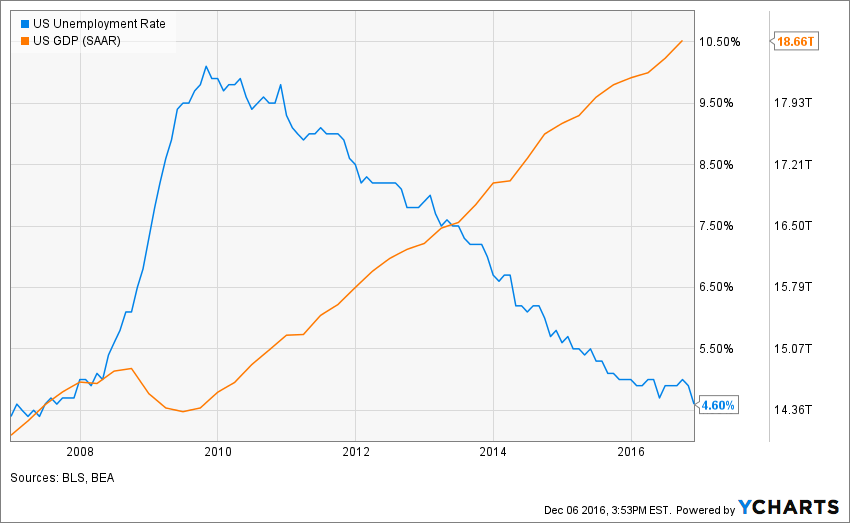

This is the same graph in numbers. You can clearly see how the GDP is growing and how the unemployment rate is now getting stable under 5%. While we keep reading that the economy is going nowhere and that jobs numbers are bogus, it doesn’t seem that way when we look at the fact. If all the numbers we read are modified or interpreted in a nice way, how can the Government lie for so long? Since 2008, they would not been able to hide the truth for almost a decade. Then, let’s face the fact; the economy is going well in the U.S. and the stock market is following the same trend. Period.

Source: Ycharts

Another effect that has been affecting earnings over the past couple of years is the strong U.S. currency. As the U.S. dollar gains strength against all other currency, we see U.S. companies have a harder time to export their goods. A strong U.S. currency also affect companies doing 40% and over of their revenue offshore. Unfortunately, this is the case for many dividend paying stocks. This is probably why you will not see strong earnings growth over the past 2-3 years for several companies. However, as you can see in the graph above, the U.S. dollar seems to have reached a plateau against the Canadian dollar and the Euro. Following this situation, the exportation of goods is picking-up. This is because the market is now getting used to this new reality. We can now look forward. The beauty of the U.S. stock market is that it is well diversified. There will also be a sector growing and where investors could benefit.

I’ll finish this introduction with one of these sectors.

Source: Ycharts

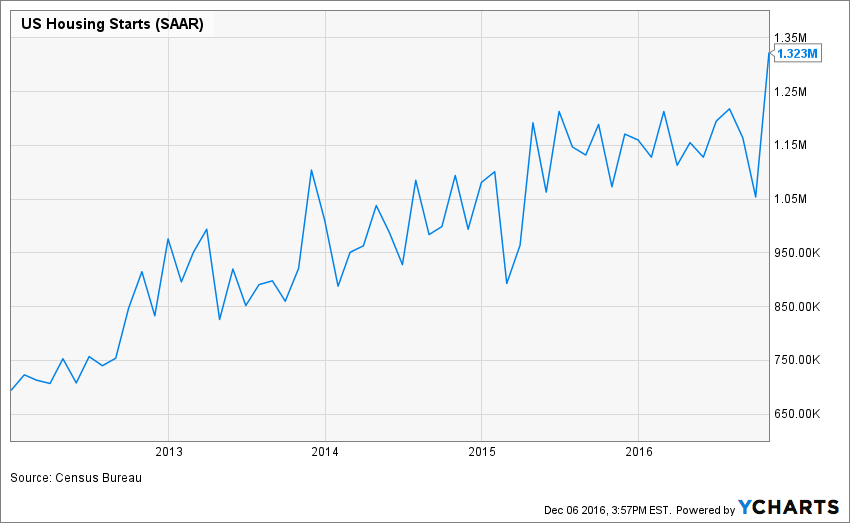

The construction sector was somewhat the foundation of the 2008 credit crisis. As more people were using their house as a ATM machine, more people were flipping houses and pushing new constructions to the top. By looking at this graph, we can see that this sector is recuperating very well and this will support a strong U.S. economy in the upcoming years. When you combine GDP growth with low unemployment rate and strong housing starts, you get all the ingredient for a stable and growing economy. In other words, there isn’t much sign of a recession coming our way and we should definitely have an interesting year in the stock market for 2017.

In the light of this analysis, we are bullish for 2017.

The following lists of stocks has been defined accordingly.

I’ve started a tradition of selecting 20 U.S. companies to beat my benchmark, the VIG (Vanguard Dividend Appreciation ETF) back in 2012. Out of all my prediction, my U.S. portfolio failed only once to beat its benchmark. This article is highlighting 3 of my selections:

HONEYWELL INTERNATIONAL (HON)

Business model:

Honeywell invents and manufactures technologies to address some of the world’s toughest challenges initiated by revolutionary macrotrends in science, technology and society. The company evolves in three different industries: Aerospace & Transportation, Automation & Control system, Materials & Chemicals. The company recently combined the aerospace and the transportation segment in order to improve scaling economy.

Main strengths:

The company has put additional focus on software engineering with nearly 11,000 engineers working on software instead of more classic industrial goods. The software business is better as it enables more combinations of services and drives higher margins. Honeywell certainly has some solid ground for future growth.

Potential risks:

While margins improvements were quite phenomenal, we can’t expect to see the company keeps increasing its margins. Therefore, further numbers shouldn’t be that impressive. Also, HON automation segment may suffer from the oil and gas industry slump.

Dividend growth perspective:

management had announced last year that the dividend payout ratio will increase in the upcoming 4 years. In 2015, the dividend payment increase was of 15% and 11.76% in 2016. I’m not putting on my pink colored glasses and expecting a 12% dividend growth for the next 10 years, but I can appreciate the growth will be significant for several years to come.

Investment thesis:

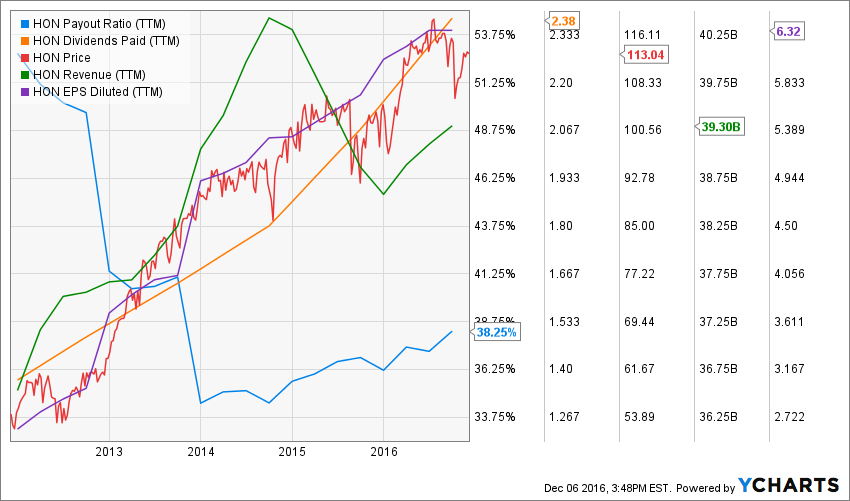

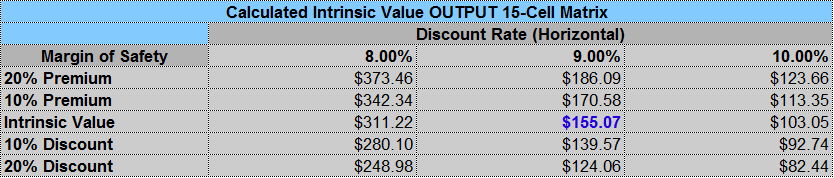

Honeywell has made impressive efforts to improve their internal practices over the past 15 years after failing to merge with General Electrics (GE). Those efforts paid well as the company operating margins improved from 7.6% in 2004 to 15.2% in 2014. Those impressive margin increase lead HON EPS to increase by 10% in 2015 as the company is facing a challenging economy. The company was also able to increase its dividend by 10% CAGR over the past 5 years. HON is a leader in the aerospace control and safety systems and should benefit from its leadership position during the commercial aircraft upcycle.

Valuation:

JOHNSON & JOHNSON (JNJ)

Business model:

Johnson & Johnson is among the noblest companies on the dividend king list. It demonstrates an incredible combination of #1 and #2 brand portfolio across the world while also offering additional growth vector through its drug division. JNJ shows a diversified revenue stream model across many consumer goods and has the necessary cash flow to support a strong drug pipeline leading to sustainable cash flow creation year after year. The pharmaceutical division represents 40% of JNJ’s total revenue and is mainly concentrated around immunology, oncology & psoriasis drugs. JNJ has a strong focus on speciality drugs which shows stronger pricing power and are harder to replicate once patents expire. This gives more time to JNJ to capitalize on their products.

Main strengths:

Johnson & Johnson is a strong company on many levels. The company is so well diversified that it always has a source of growth somewhere. Recently, a new cancer drug called Darzalex started its first sales quarter with $100 million… well above expectations.

Their various consumer products benefit from high pricing power due to their world class brands. The medical equipment division enjoys continuous business from the same clients as the switching cost is often higher than any potential benefit. The company is also building an important cash reserve (17 billion in 2016) in the light of potential acquisitions to find additional growth vectors.

Potential risks:

Back in 2012, JNJ had several quality control issues. This hurt sales and potentially hurt some brands as well. It was a good example that even the best companies are not 100% sheltered. Potential lawsuits due to product misconception or severe drug side effects could also hurt JNJ balance sheet and image. Finally, pharmaceutical companies are always dependant on their pipeline to assure their future. Failing to continuously discover new drugs could also penalize growth.

Dividend growth perspective:

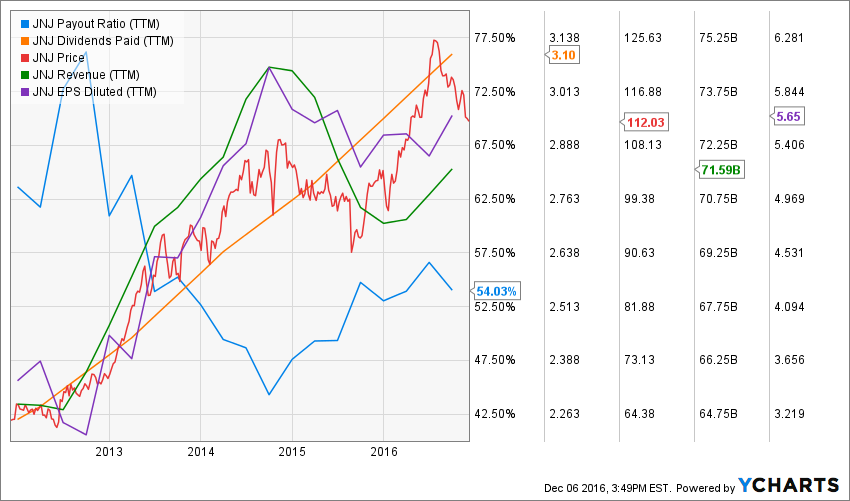

After solving its quality control issues in 2012, JNJ has brought its payout ratio back under 60% leaving the company enough room to increase their dividend for years to come. With so many income streams coming from various segments, cash flow creation is never an issue. JNJ is definitely one of the best dividend kings from the list.

Investment thesis:

JNJ shows both stock appreciation potential and strong dividend growth. This is the perfect model of a recession-proof business with enough growth vector in their portfolio to boost sales year after year. An investment in JNJ will bring its shareholder a healthy and increasing dividend payment at the same time at considerable stock appreciation over the long haul.

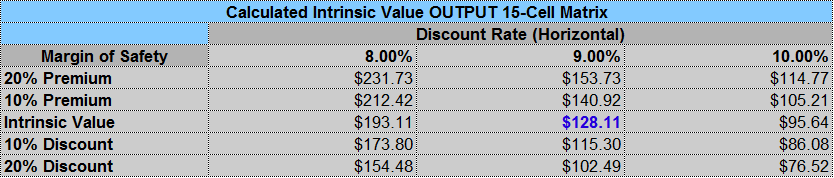

Valuation:

STANLEY BLACK & DECKER (SWK)

Business model:

The company is a diversified industrial goods manufacturer showing #1 and #2 brands in all their markets. Its products revenues are coming from both US (49%) and outside the country (51%). The company has been paying dividend for the past 139 years and shows 48 consecutives increases.

Main strengths:

The size of the company and the power of its distribution network allows the company to benefit from important scaling economies. Most tools are heavily used in the construction industry and therefore, generate repetitive purchases. This generates a continuous cash flow for the company. Their brand portfolio is very strong and brand names are well-known by customers. They are also synonymous with performance.

Potential risks:

The stock market has put great hope to see the company increasing its revenue and earnings in the future. If the FED raise interest and it slows down consumers’ appetite for new house and renovation, SWK sales may be hurt in the upcoming years.

Dividend growth perspective:

What is more important than past dividend growth? Future dividend growth! I’m mostly interested in the company’s ability to increase its dividend in the future. Looking at the SWK dividend growth combined with its payout ratio, we can see that management’s policy is to maintain a very stable payout ratio and therefore, increase its distribution according to its EPS growth.

Investment thesis:

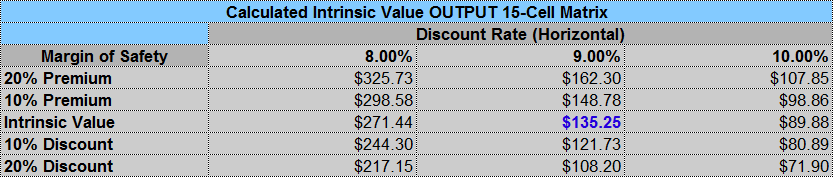

SWK is a long term play considering its relatively low dividend yield, but strong and consistent dividend growth policy. This is not a supercharged stock that will skyrocket, but it will certainly improve your portfolio stability and add some serious dividend growth power. SWK important size of its distribution network enables large economy scale. SWK is using its free cash flow to buy back shares and gives 50% of it to its shareholders as dividend payment. As the US economy strengthens, the housing construction and renovation industry is rising. This will obviously boost SWK sales in the US.

Valuation:

Want More? I have 7 other Canadian Dividend Stock Picks in my Book!

I’ve compiled a list of 20 dividend stocks to do well in the market for 2017. You just read about four of them, but there are still lots to discover in the book! The book includes the 20 dividend stock analysis plus 10 Canadian dividend stocks. That’s 82 pages worth of information for only $15.00 usd.

**BONUS** this year, you get the 2017 Best Stock Picks book + The Dividend Toolkit! **BONUS**