Andrew Peller (ADW.A.TO) owns wineries in British Columbia, Ontario and Nova Scotia. It doesn’t only produce its own wine, but also market it along with other products. ADW owns several brands like Peller Estates, Trius, Hillebrand, Thirty Bench, Sandhill, Copper Moon, Calona Vineyards Artist Series VQA wines and Red Rooster. Currently the company has an estimated 14% share of its total wine market and a 37% share of domestic wines.

The company is known to grow its revenues through acquisitions. Since 1995, management invested over $114M to purchase 14 vineyards.

Source: ADW Factsheet

The company has built a solid relationship with provincial liquor stores, but also maintain company-owned retail stores in Ontario.

Revenues

Source: Ycharts

Andrew Peller shows a strong and steady growth of its sales mainly due to the creation of multiple products, a strong marketing program and several acquisitions. The Canadian wine business is doing well and ADW continues to ride this bullish trend.

Its recent alliance with Wayne Gretzky vineyard will not only be good for wine sales, but will also open the door to whisky production.

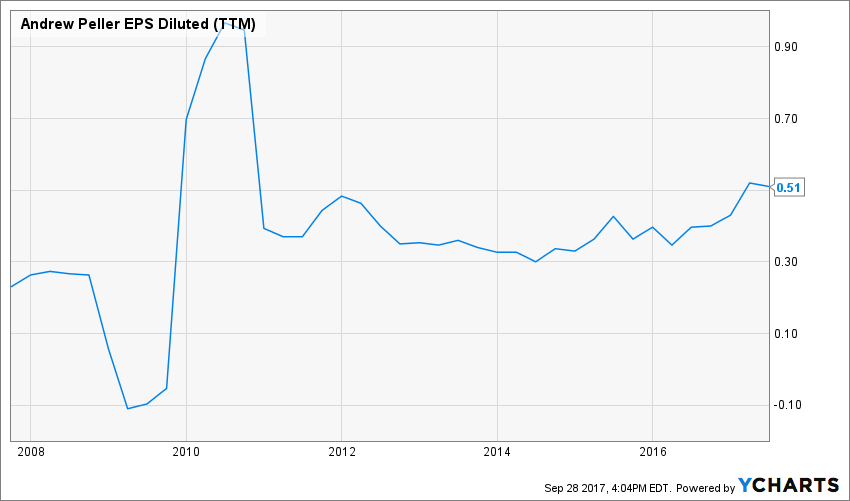

Earnings

Source: Ycharts

Unfortunately, growth came with a price. Over the past 5 years, the company has struggled to increase its EPS. Creating brand awareness is expensive and ADW had to spend significant money in marketing and developing new vineyards. Fortunately, management has put more emphasis on their costs and revised their supply chain to improve their margins.

Source: Ycharts

Dividend Growth Perspective

Source: Ycharts

Wow… such a low dividend yield for this wine company. Does it even make sense to invest? Well, if I sell you that while the yield went down from 3.75% to 1.28%, the stock price surged 260% over the past years, would you be more lenient? The dividend payment also increased by 36% or 6.34% annualized growth rate during the same period.

Source: Ycharts

It is rare that we such low payout ratio with such high cash payout ratio. When I looked at their financial statement, we can see that the company had to invest massively recently, boosting capital expenditure to a record level:

Source: Ycharts

Additional investments have been required notably to open the new Wayne Gretzky Estate Winery & Craft Distillery. This is a 15,000 square foot facility includes a winery, craft distillery, barrel aging cellars, tasting rooms, retail and hospitality facilities, all surrounded by landscaping and vineyards.

I expect the CAPEX to go back down to more reasonable level in 2018. Therefore, there is nothing to worry about the dividend sustainability.

Potential Downsides

The wine industry and the domestic and international market in which the Company operates are consolidating. While this could be a great opportunity, it also brings stronger competitors to the table. ADW must continue investing in its brand awareness to keep its market share.

Since Wine is a luxury product, any economic downturns would affect ADW sales. For now, I don’t think it’s an issue as the Canadian economy has proven to be more resilient than anticipated.

Valuation

After such a great ride on the stock market, is there any money left to be made on ADW? Let’s take a look at how the market valued the stock over the past decade.

Source: Ycharts

In all honesty, ADW seems a bit pricey right now. The PE ratio never stopped growing since 2010. On the other side, we are looking at a company that is continuously reaching for the sky as well. Nevertheless, at a 24 PE, there is no bargain here.

Digging deeper, I’ve used a doubled stage dividend discount model to see if there is value to invest in.

| Input Descriptions for 15-Cell Matrix | INPUTS | |||

| Enter Recent Annual Dividend Payment: | $0.18 | |||

| Enter Expected Dividend Growth Rate Years 1-10: | 9.00% | |||

| Enter Expected Terminal Dividend Growth Rate: | 7.00% | |||

| Enter Discount Rate: | 9.00% | |||

| Margin of Safety | 8.00% | 9.00% | 10.00% | |

| 20% Premium | $27.62 | $13.72 | $9.09 | |

| 10% Premium | $25.32 | $12.57 | $8.33 | |

| Intrinsic Value | $23.01 | $11.43 | $7.57 | |

| 10% Discount | $20.71 | $10.29 | $6.81 | |

| 20% Discount | $18.41 | $9.14 | $6.06 | |

Please read the Dividend Discount Model limitations to fully understand my calculations.

Interesting enough, there isn’t a huge bargain on ADW, but it seems that you would not be left in the field if you buy it now. There is still a small margin of safety of 6-7% at the moment.

Final Thought

When you find a company growing at this pace, it’s hard to no pay a premium. However, it seems the wine isn’t that pricey these days. It could be a good timing to buy some bottles!

Disclaimer: I do not hold ADW.A.TO in my DividendStocksRock portfolios.

If you like my analysis, click on FOLLOW at the top of the article near my name. That will allow my articles to display on your homepage as they are published.

Additional disclosure: The opinions and the strategies of the author are not intended to ever be a recommendation to buy or sell a security. The strategy the author uses has worked for him and it is for you to decide if it could benefit your financial future. Please remember to do your own research and know your risk tolerance.