Each month, we issue The Mike’s Buy List for our DSR members. They get our best ideas for both U.S. and Canadian dividend stocks. The first Friday of each month, they receive our top 10 growth and top 10 retirement (yield over 4%+) investment ideas.

We are still following the virus and its impact on the economy. Considering what happened on the market over the months, I decided to share some of our picks with you. Today, we’ll cover two growth stocks and I’ll share two companies to consider for your retirement next time.

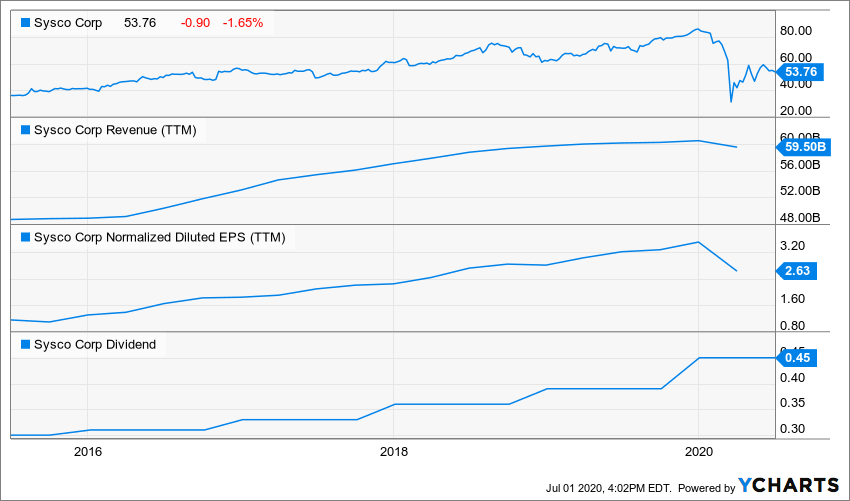

SYSCO (SYY)

What’s the story?

The sentiment around the restaurant business is going both up and down depending on how the virus spreads across the U.S. As we saw more cases in large states such as Texas and Florida, Sysco took another beating. Since 62% of its revenue comes from the restaurant industry, you can expect a bumpy road ahead.

Later in June, we got some good news coming from one of its competitors, Performance Food Group’s (PFGC), as it reported their earnings on June 23rd. The food distribution company showed a steady trend of weekly sales increasing from March to June. PFGC is a smaller player compared to SYY, but it gives us more information on how sales could bounce back during summertime.

In the meantime, SYY shows $6B in cash to weather the storm. You can count on this dividend king to still be around after this crisis and thriving once restaurant activity returns to some semblance of normal.

Business Model

Sysco is the largest U.S. foodservice distributor, boasting 16% market share of the highly fragmented foodservice distribution industry. Sysco distributes over 400,000 food and non-food products to restaurants (62% of revenue), healthcare facilities (8%), travel, leisure, and retail (9%), education and government buildings (9%), and other locations (12%) where individuals consume away-from-home meals. In fiscal 2019, 80% of the firm’s revenue was U.S.-based, with 8% from Canada, 5% from the U.K., 3% from France, and 4% other.

Investment Thesis

Sysco is a dominating player in a highly recurring business, food distribution. Even better, this market is fragmented in the U.S. with over 10,000 small food distributors across the country. This offers SYY a great opportunity to acquire and integrate smaller players. SYY is more than twice the size of its largest competitor, US Foods. The company offers a wide variety of products and its network quality and reach is unmatched. While the pandemic may hurt the entire industry, SYY will likely become one of the big winners assuming some competitors to close business. SYY also offers restaurant-quality data as it compiles trends across the world. The company is also well-diversified as none of its clients represent more than 10% of its sales alone.

Potential Risks

Sysco evolves in a challenging business environment as many restaurants have a hard time growing their sales. If inflation starts to rise, it is possible that SYY will have to eat up a part of the cost increase as restaurants might not be able to take additional price raises. Since food distribution is treated as a commodity with little differentiation, SYY doesn’t enjoy much pricing power. With the economic lockdown and social distancing, many restaurants will close and SYY will see a short-term drop in revenue. Buying the dip is an educated guess, but proceed with caution. Finally, its recent effort to manage costs failed to improve margins significantly. Therefore, expect slower earnings growth ahead as inflation will likely bite.

Dividend Growth Perspective

SYY shows 50 consecutive years with a dividend increase. With such an impressive dividend growth history, you can expect SYY to keep going forward. The company has built a business model generating a recurring source of cash flow. The company continues to grow both organically and through acquisitions. It can keep a dividend growth policy around 5% each year. This is definitely a stable holding for your portfolio.

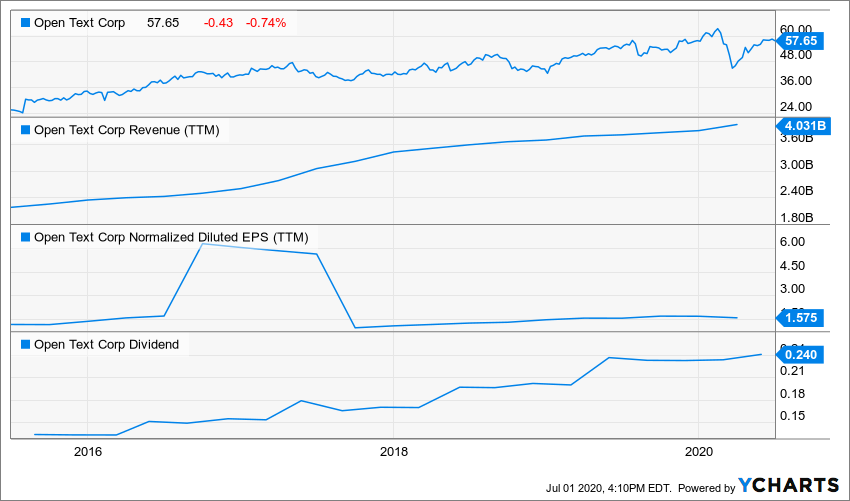

OPEN TEXT (OTEX.TO / OTEX)

What’s the story?

To nobody’s surprise, OTEX is performing better than the Canadian stock market since the beginning of the year. This trend continued in June as well. Interesting enough, tech stocks may be the safest place to invest for the rest of the year.

OTEX could see more business coming from the healthcare sector. For example, Rapid Radiology will use the OpenText EMR-Link to streamline the delivery of radiology test results to EMR charts at healthcare facilities. This will include senior and long-term care facilities with their more vulnerable patients. The OTEX products help the healthcare industry manage and transfer information more rapidly. This could become a crucial tool in the event of a second wave of the virus.

Business Model

Imagine a big business that employs 100 people and keeps growing. Each day, tons of information is collected about products, sales, employees, expenses, contracts, etc. This information is piling up in mountains of unreadable reports. It needs a solution to receive, integrate and digest this data. This is called Enterprise Information Management (EIM) system. EIM helps managers make better decisions by organizing the information to access it rapidly, understand it and trust it. OTEX is a leader in the industry and Canada’s largest one. It helps over 100,000 customers to share, store, retrieve and analyze their company’s information.

Investment Thesis

Big data, cloud, and security. Three keywords you are not done hearing about. As we evolve through an era of consolidation; businesses grow larger every second. Managing growth is one thing but dealing with the enormous amount of data this growth is bringing inside each company is part of Hercules’ labors. Enterprise Information Management (EIM) systems have been developed to manage this issue, and OpenText happens to be one of the leaders in this emerging business. OTEX has developed a strong expertise in growth by acquisitions. Each time it adds a new business, it increases cross-selling opportunities.

Potential Risks

Open Text evolves in a changing environment and is continuously one iteration away from being obsolete. Several competitors also lurk to grab OTEX clients. Many are larger U.S. companies with more resources. OTEX built a strong name and there is a switching cost for clients, but it is not impossible that OTEX stops being the flavor of the month. Plus, OTEX is condemned to grow by acquisitions. With several transactions under its belt, it doesn’t seem like a problem. However, this could lead to hectic quarters. The company recently announced a restructuring plan and reduced spending for 2020 amid the covid-19 crisis. Nobody is truly sheltered from the economic impact of this virus.

Dividend Growth Perspective

OTEX shows a low yield but its growth policy is quite aggressive. OTEX will be surfing on strong tailwinds for several years. OTEX has built a business model generating consistent cash flow (recurring revenues through subscriptions). This will support dividend payment (and increases) for a while. As the company continues its quest for growth, expect a double-digit dividend growth policy for several years to come. Please note the dividend is paid in USD.

Techniques to Avoid Dividend Cut

In these times of uncertainty, it could be easy to fall for a bargain. But if you want to avoid dividend cuts, you must invest with caution. Recently, I offered you my three favorite techniques to avoid cuts. They have been proven to be highly effective in the past. You shoud use this short and applicable list of actions to review your portfolio this summer. There is nothing like hanging around a pool and optimizing your portfolio.  Volume will be lower, volatility will take a pause, and it will be time for your to take a deep breath and make sure you don’t suffer from additional cuts this fall.

Volume will be lower, volatility will take a pause, and it will be time for your to take a deep breath and make sure you don’t suffer from additional cuts this fall.

The post Add Magic to Your Portfolio: Two Dividend Growth Stocks to Buy appeared first on The Dividend Guy Blog.