I’ve been fighting for many, many… many years. It has been an epic fight that started the day I switched my portfolio toward dividend paying stocks. When I started blogging about dividend growth investing, I was reminded several times by older investors that many of my picks didn’t mean anything to them. After all, who needs Disney (DIS) or Canadian National Railway (CNR.TO) with such low yield when you can buy Kinder Morgan (KMI) and Cominar (CUF.UN.TO). All right, I’m writing 2 two names in bad faith since both companies are known for their high yield and massive dividend cuts in the past.

That is my point all along; how could you hope for a safe portfolio with high yielding stocks? There are no free lunches in finance. If a yield is over 5%, it means there are additional risks attached to this company. Over the past 10 years, we have seen incredibly low rate across all investment products. Therefore, when you pick a stock paying a 6-7% yield, it seems too good to be true… and it is usually is!

As the same time, I totally understand the point of many older investors. They are retired or about to retire and wish to use their portfolio to generate income. If someone spent his entire life saving money aside, the last thing he wants to do is to take money away from his capital. Therefore, the perfect retirement portfolio would generate enough income he would not have to sell shares of any stocks to live.

Retire with a 4%+ yield portfolio? Yes if…

With this idea in mind, I decided to do extended research. I wanted to see if I could pick companies with a higher yield that would still meet some basic investment criteria. I’ve been asked many times by DSR members to create a “revenue portfolio”. I was reluctant to create one since I see lots of risks in investing in higher yielding stocks. After lots of research, I realized it was possible to build a solid portfolio with a higher yield. There is a thin line where you sacrifice potential growth for a higher yield without compromising your retirement. It’s not easy, but you can do it. Here are some rules I will use to build a “revenue portfolio”.

01 Aim for 4-6% yield for most stocks

I know that some investors will tell me there are incredible opportunities with a “safe” dividend payment and a 11% yield. But I’d like to have this conversation once we hit a bear market and your company cut its dividend to see its shares tumble.

Therefore, my goal will be to pick among companies that are slightly more generous than others. Just by using a 4-6% yield condition in my stock screener, I drop the potential companies to 1,049 candidates (for both US and Canadian market). I’m not saying I will not pick a few stocks with higher yield. For example, I think Enbridge (ENB.TO) is a good pick at the moment and it currently pays around 6.50%.

02 Some Dividend growth to cover the inflation

Many investors tend to forget about one of the most important concept when it comes down to retirement planning. I’ve discussed on this blog (here) that inflation could eat up a good part of your income over time. Therefore, if you retire with $1M generating 8% (80K) annually with no dividend growth, you will fall short at one point in time. Interesting enough, many companies paying 8%+ yield don’t offer any kind of dividend increase.

This could have a huge impact on your portfolio in 20-30 years from now. If you are younger than 75, you should be concerned about inflation.

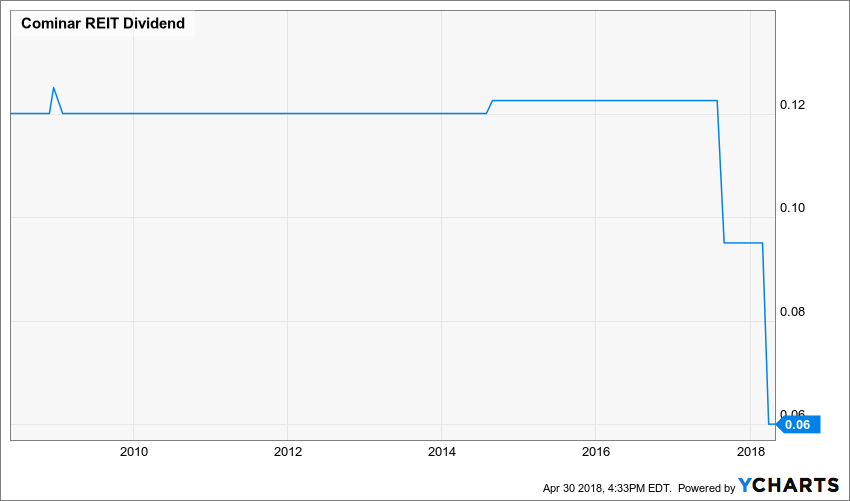

The other risk of picking a “no growth” stock is obviously suffering from a dividend cut. When a company can’t increase its payout, it is usually because it is at the maximum of its capacity. Those companies are one bad luck away from a dividend cut. This is exactly what happened to Cominar when you look at their chart:

Source: Ycharts

The company showed a $0.002 (no typo) on its monthly dividend 4 years ago. The company couldn’t pay a dime more during many years and end-ed up cutting its payment twice in the past 12 months to ensure its survival.

For that reason, I’ve added a 2% annual dividend growth rate to my stock screener. I went from 1,049 companies to… 252! If a company can’t even keep up with the inflation, I don’t see why I should even consider it for any type of portfolio.

03 Avoid sector concentration

It is well-known that utilities, energy / MLP’s and REITs are more generous sectors in term of payments. It would be tempting to concentrate on a few “sure sectors” and cash a juicy dividend. The problem with such strategy is that, sooner or later, one of those sectors will get hit my challenging economic conditions. During such event, there are good chances to see a few companies cutting down their dividend. You certainly don’t want to hold too many stocks cutting down their payout at the same time, don’t you?

For that reason, I will not allow any sector to represent more than 20% of my portfolio. It will be crucial to find companies evolving in various industries. This is the best way you can ensure your portfolio will sustain its high yield throughout many years.

Starting to work on those revenue portfolios!

I have several projects on my plate, but it seems I can’t get enough! This month, I’ll have a major announcement and I’ll be working on 2 revenue portfolios (US and Canadian). They should be ready by the end of the month for DSR members! In the meantime, you can have access to my Retirement Dividend Stocks List here:

Disclaimer: I hold shares of ENB.TO

The post A High Yield Portfolio? Only if You Meet Those 3 Criteria appeared first on The Dividend Guy Blog.