#1 TGT benefits from a stellar dividend growth history and classic business model in order to maintain the interest of investors.

#2 Many investors see TGT as being the opportunity of the year and claim it is clearly oversold.

#3 On my side, all I see is declining revenues, margins under pressure and no growth vectors.

#4 TGT is a screaming sell, prove me otherwise!

All the time I find too many articles telling me how Target (TGT) is a great company and that it is being oversold. This is probably the opportunity of the year… really? In this article I’m going all-in to destroy this company and show you how bad it is. I do it this way because sometimes, we need a good slap in the face to wake-up from our fantasy. You can thank me later.

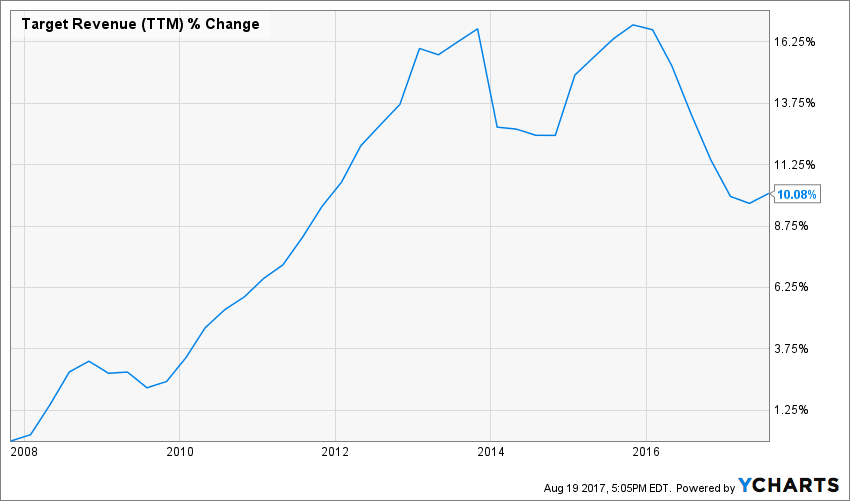

#1 No revenue growth

My first point is Target didn’t show the ability to grow their revenue through the past decade. When you look at the graph below, you see an annualized revenue growth rate of 0.96%.

Source Ycharts

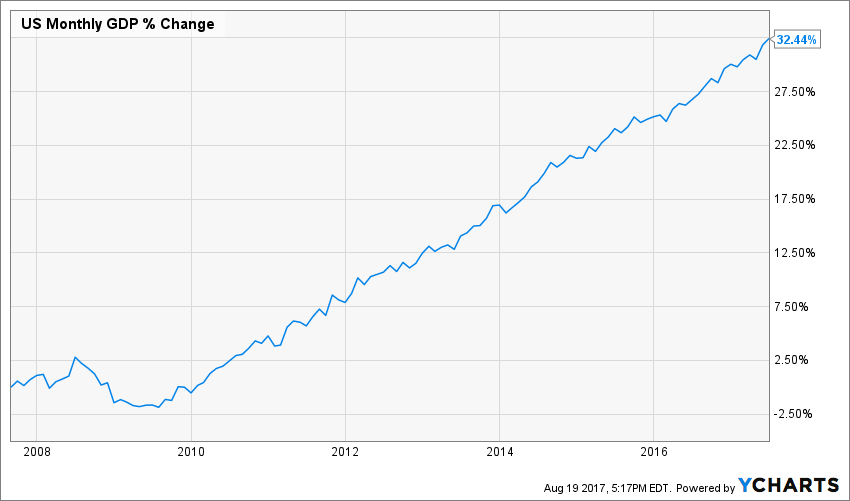

In the meantime, I keep reading articles telling me how the U.S. economy is growing at a mediocre rate with no really strong tailwinds:

Source: Ycharts

Well… the no-tailwind-mediocre-growth-rate of the U.S. GDP is still three times bigger than Target. If the GDP is going up, unemployment rate is going down and American customers’ confidence is strong, can you tell me where TGT revenue will be once we hit a recession? The company is showing no ability to grow their revenues. This is very scary.

#3 Where are the growth vectors?

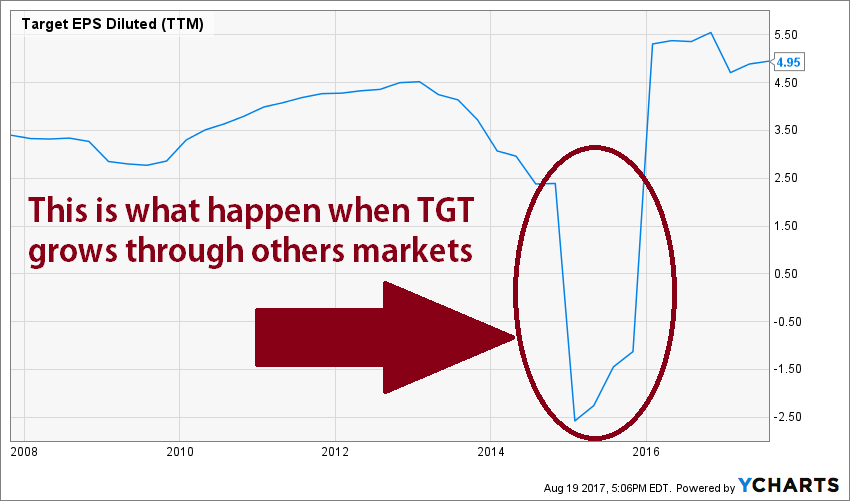

I’m pretty sure management is well aware of the situation. Therefore, I’m sure they all called their buddies and held an offshore meeting to make sure they had clear ideas on how to build the “new Target”. You know the one that will generate growth?

A few years ago, a smart guy in the upper management level team had a great idea while sipping his whisky: Why not conquer the Canadian market? Sound idea. I’m not being sarcastic here. The Canadian market is very close to the U.S., not only geographically speaking, but in terms of culture too. Well, this is what we thought anyways! Here’s what actually happened when they tried to do business with their neighbors:

Source: Ycharts

All right, now that the Canadian mess has been closed and written off, TGT is back to making money. Still, no growth vectors. Could we hope for an international growth operation? I highly doubt they could do better than what they just did.

Yeah, but Mike, there are online sales, last quarter, Target’s comparable digital channel sales increased 32%!

Fair point; 32% increase is huge. However, 32% growth when your online sales count for 4.4% of your total sales isn’t really what I call a game changer. I call it a nice gig. In fact, TGT and the media can continue telling the world their online sales are surging, they are nothing compared to their core business:

Source: TGT 2016 annual report

But let me ask you a question: if online sales grow by 30% and total revenue grows by 1% over a decade, don’t you think TGT is just cannibalizing their store sales with their online business?

I’m sorry, but I don’t see how TGT will grow their business in the next decade. Anyone in the audience care to explain it?

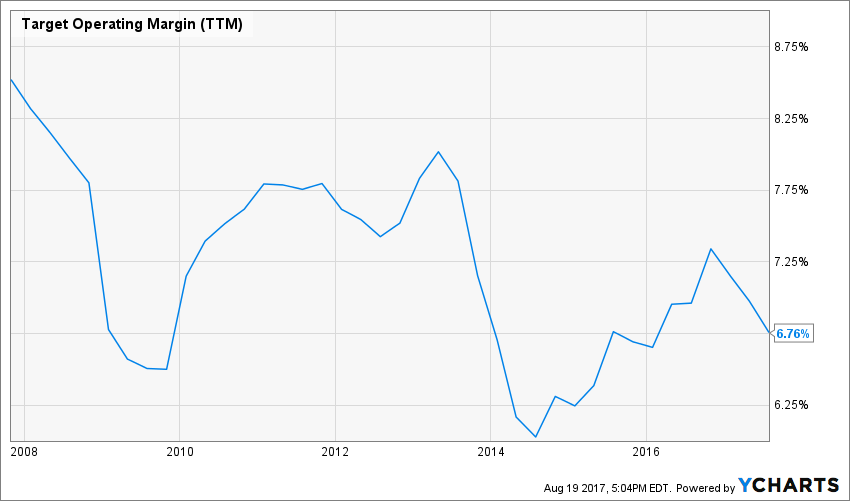

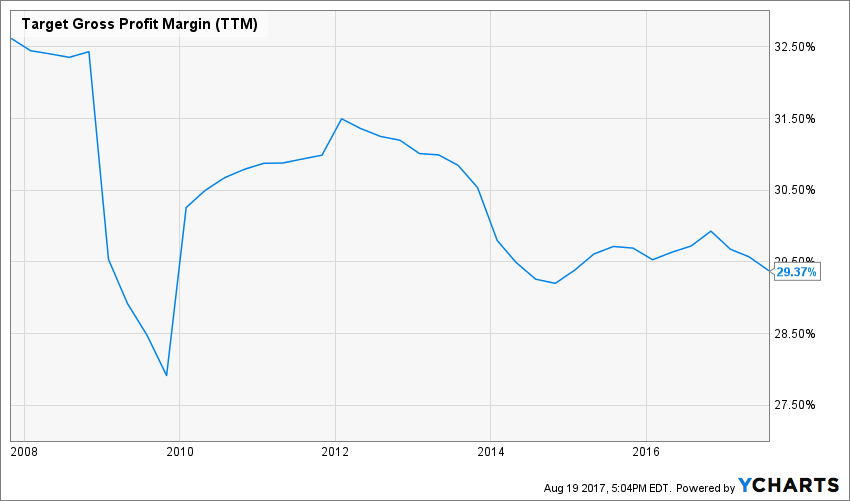

#3 Margins under pressure

Funny enough, I’m already at my third reason and I haven’t written about “you-know-who”. And I can continue with margins before looking at the Great Retail Destroyer. What happened to TGT’S operating margin while their revenues were barely going up during the past decade? It is also down:

Source: Ycharts

And you see a similar landscape if you look at TGT gross profit margins:

Source: Ycharts

All right… some TGT lovers mentioned the company could go head-to-head with the Disruptor. It only has to cut their prices to keep their clients in store instead of online. But since TGT’s margins are already under pressure, how could the company fight Voldemort trying to use its own magic against him? And while TGT tries to beat Amazon (AMZN) online, it will also receive a few jabs from other competitors such as Wal-Mart (WMT). Therefore, this strategy only contributes to further margins decline… TGT is on sale you are telling me?

#4 TGT is very expensive – IT IS NOT ON SALE

Yeah… let’s get to the point and look at this incredible buying opportunity. Those who look at the tree and not the forest see a PE ratio of 11.24. This is an incredibly low valuation:

Source: Ycharts

However, low valuation doesn’t always rhyme with great buy opportunity. You can ask BlackBerry (BBRY) shareholders their opinion on this:

Source: Ycharts

In fact, if I use a different method like the dividend discount model, I get a completely different song:

| Input Descriptions for 15-Cell Matrix | INPUTS | |||

| Enter Recent Annual Dividend Payment: | $2.48 | |||

| Enter Expected Dividend Growth Rate Years 1-10: | 4.00% | |||

| Enter Expected Terminal Dividend Growth Rate: | 4.00% | |||

| Enter Discount Rate: | 10.00% | |||

| Discount Rate (Horizontal) | ||||

| Margin of Safety | 9.00% | 10.00% | 11.00% | |

| 20% Premium | $61.90 | $51.58 | $44.21 | |

| 10% Premium | $56.74 | $47.29 | $40.53 | |

| Intrinsic Value | $51.58 | $42.99 | $36.85 | |

| 10% Discount | $46.43 | $38.69 | $33.16 | |

| 20% Discount | $41.27 | $34.39 | $29.48 | |

Please read the Dividend Discount Model limitations to fully understand my calculations.

TGT shows an additional potential downside of 23%!

If TGT fans tell me I should keep it or buy it due to its stellar dividend growth history, using the DDM should make total sense. However, even with a 4% dividend growth rate (this year’s raise is 3.33%), the stock is a screaming sell trading way higher its intrinsic value. When catching a falling knife, you would expect to get some sort of safety net. You don’t get any kind of safety net on this trade, that’s for sure.

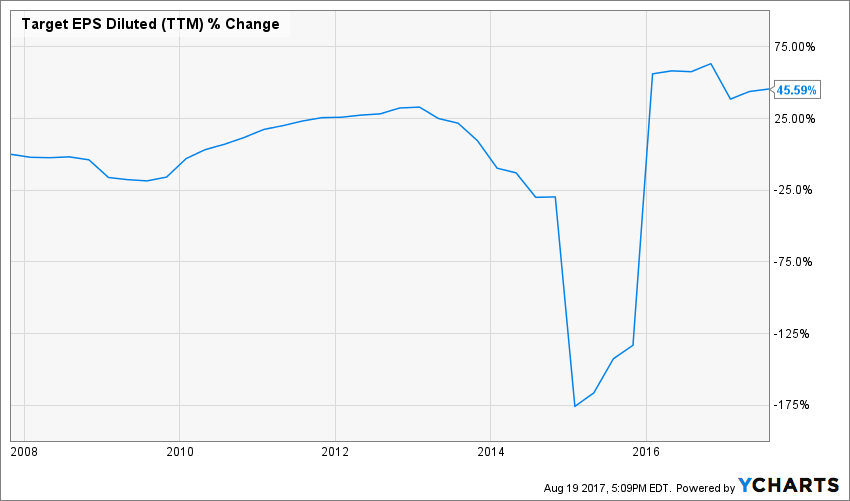

#5 But, Mike, the EPS is growing… that’s another reason to sell!

Source: Ycharts

While revenue growth is inexistent over the past decade, TGT has been able to bring a respectable 3.83% annualized earnings growth rate. But this tells me only one thing; TGT has streamlined its process, cut where it was necessary and it is probably getting closer to no room in cutting to improve their results. Since I’ve already demonstrated TGT will not be able to generate any kind of growth in the future, I’m asking you, dear readers, to tell me how TGT will get away from this situation.

Don’t tell me you hate Amazon or you shop at TGT. The company sold over $69 billion in goods last year, I know it has clients. Still, I’m asking you where is the growth? Where TGT will be in 10 years? I have an answer for you, do you remember these names?

Eaton, The Bay, Zellers, Woolco, Sears, RadioShack……

Disclaimer: I’m long AMZN