The RRSP season is nearing its end (your last day for 2014 RRSP contribution is March 2nd 2015) and I thought I would go for 4 stock pick ideas. Since US dividend payouts are non-taxable in a registered account, this is the perfect place for Canadians to buy US stocks. Between you and me, even though the currency exchange rate is hurting your purchasing power, this won’t change this year and it could even get worse. So why not considering the great US diversification in dividend payers and go south of the border for your next pick? Here are my suggestions;

Walt Disney (DIS)

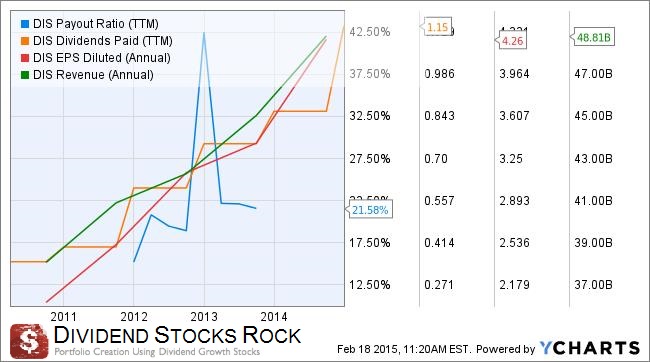

You know I’m a big fan of Disney. And their latest quarterly reports confirm my beliefs. Despite an outbreak of measles at Disneyland this December, Disney posted very strong results. Latest blockbuster Frozen boosted home entertainment and toy sales. All five divisions (Media Networks, Parks & Resorts, Studio Entertainment, Consumer Products and Interactive) posted stronger sales compared to same quarter last year. It also benefits from a strong US economy and rising consumer’s confidence as the Parks unit shows operating profit higher by 20%. Disney’s movie studios published a 33% surge in profit led by three blockbusters: Frozen, Guardians of the Galaxy and Maleficient. The best part for Disney is that the pipeline is also full for the years ahead. A new Star Wars Trilogy will hit the screen with the first episode in December 2015 and the company also expects to open Shanghai Disney in spring of 2016. The dividend yield remains low (around 1%), but the company keeps most of its money (payout ratio at 22%) to ensure future growth with major investments. When you look at the stock in a dividend growth perspective, DIS is a BUY.

Lockheed Martin (LMT)

Surprising enough, Lockheed Martin managed to go through the US recession and military budget cut clouds without much pain. Now that the economy is doing better and consistent war & terrorism threats continue to appear, the need for additional defence supplies will be required. LMT is now set for higher sales for the upcoming years. The international market is also gaining momentum as Lockheed is trying to find ways to be less dependent on the US Government. The short term outlook is deceiving (as LMT issued lower than expected guidance for 2015) but the long term potential is definitely interesting. On the other hand, you have to note that Lockheed Martin is well-known for lowering guidance to temper hype and delivering higher than expected earnings. Is this a strategy or simply the fact that management is conservative? Either way, higher earnings is always good for dividend investors!

Lazard (LAZ)

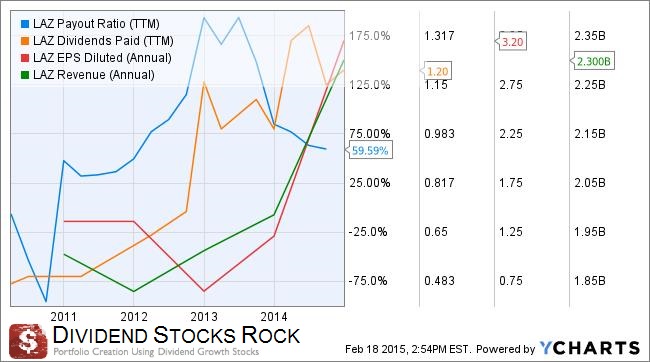

Lazard is currently riding the bull market with great success. Earnings are up significantly over the past 5 years and investors benefitted through higher dividend payouts climbing from $0.13/share to $0.30/share during this period. The fact that LAZ earns about 50% of its business from asset management and the other half through M&A provides a better diversification than other “boutique investment firms”. More recently, Lazard stock surged 15% from January 15th to February 5th, the date of their quarterly report. A Combination of strong earnings and optimistic outlook for 2015 made the stock go back to a positive level since the beginning of the year. Lazard is the most geographically diversified investing firm and benefits from a very strong reputation. Diversified revenue income streams (portfolio management, M&A, restructuring services, etc) will open the door for additional profitability in 2015. Now that the payout ratio is back to a more appreciable level, Lazard should be on your radar.

Garmin (GRMN)

This is a timely pick as GRMN just released disappointing results on February 18th and the stock price dropped like a rock on that day. EPS were not good enough for analysts and the company missed the target by $0.01 ($0.77 vs $0.78) for the quarter. This data alone isn’t enough to make the stock drop, but the deceiving EPS guidance for 2015 was as it missed the consensus by $0.14 ($3.10 vs $3.24). Garmin automotive device segment reported a drop in sales of 11%. Enough with the bad news, now I’ll tell you why this stock should be on your list. The first reason is that GRMN increased its advertising expenses by 55% last quarter; this is mainly why the company failed meeting EPS estimates. On the other hand, this marketing strategy might bring additional sales in 2015 as the advertising effect is not always immediate. The second reason GRMN is a good pick is due to its fitness segment. Even though there is fierce competition in this sector, Garmin expects sales to grow by another 25% this year. This helps the company diversify its sources of income (the automotive segment now represents 43% of total revenue compared to 58% in 2013). Considering the recent drop in price, I think Garmin is a great buying opportunity.

Which one is your favorite?

To be honest, if I had to pick only one stock from this list, it would be Disney… but I hold it already. What do you think?

Disclaimer: I personally hold shares of DIS, LMT and both stocks are also hold in our Dividend Stocks Rock portfolios.