I remember my first trades on the market back in 2003 when I was 22 and starting both my career in the financial industry and my investing journey. I was fortunate enough to avoid high fees from mutual funds and start directly with an online broker account.

The first thing I did after opening it was to buy shares of Power Corporation (POW). My investment thesis? I worked for a business unit in partnership with many of POW companies. I thought it was smart. (You can see how I evolved into a more articulate investor since then! Haha!)

After pulling out a few stock filters out on the Canadian market, I realized how difficult it was to build a 100% Canadian portfolio. Banks, telecoms, energy and basic materials stocks were omnipresent among my holdings. While those were the good years to be in the market, I felt limited in my options.

As I experienced various strategies and read many books and articles, I’ve built a complete and meticulous investing process. While I prefer to invest a good part of my money in the U.S. market (for diversification and potential), I am now able to find some hidden gems in the Canadian market.

Today I wanted to share my view on what it’s like to be a Canadian investor. I’m sure you will recognize many of the goods sides and struggles we face. I’ll also tell you how I managed them.

Source: Pixabay

Limited Sector Allocation

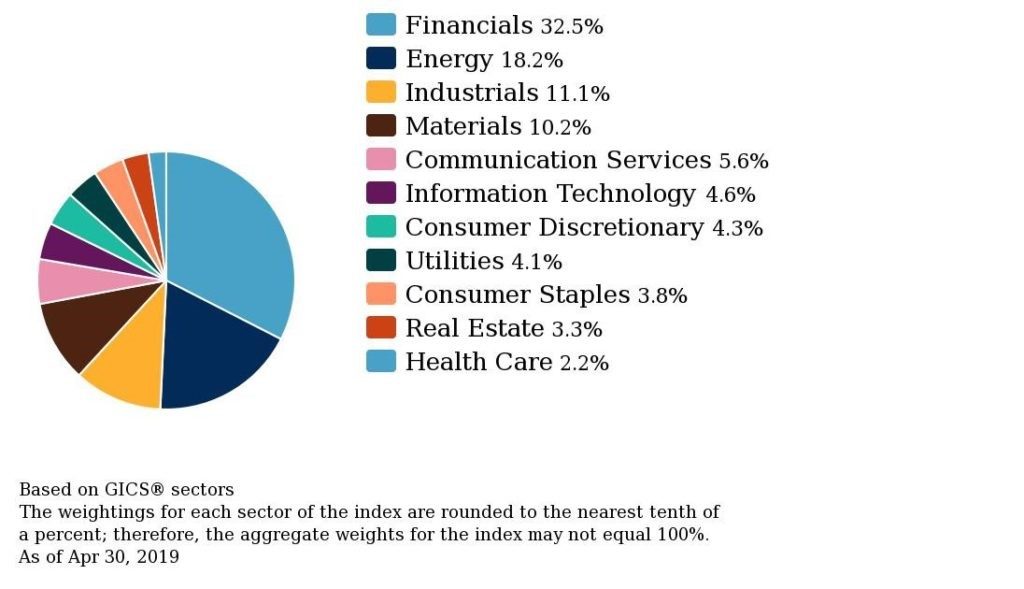

First, investing in the Canadian market initially meant being stuck with 50% of the market cap concentrated into 2 sectors: Financials and Energy. Financials are led by the Big 5 (the 5 largest Canadian Banks) who are renowned to represent one of the strongest and most stable banking systems in the world. Then, you have a few great insurance companies such as SunLife (SFL), Manulife (MFC) and GreatWest Lifeco (GWO) and a few more conglomerates such as Brookfield Assets Management (BAM) and Power Corp (POW).

The energy sector finds its power mostly in Northern Alberta with the oil sand. There were the good old days of the oil income trust until the government shut down this plan on Halloween (yes, it was a horror story for many income seeking investors!). Once I was done with those two sectors, I had only 50% of the market capitalization left to build a solid portfolio:

Source

If you are a dividend investor like me, you will find it very hard to find dividend growers among basic materials, technology and consumer (both staples and discretionary). The problem with consumer stocks is usually their very low yield. Still, I found a few interesting picks in those sectors throughout time. However, you won’t find any Disney (DIS), Starbucks (SBUX) or Coca-Cola (KO) among Canadian companies. The most important problem with most sectors is that very few businesses have international exposure.

Don’t fall for energy & basic materials

My first thought when I look at the TSX sector allocation is “don’t fall for the trendy stocks”. Many energy and materials companies have their 15 minutes of fame from such things as an oil boom, a new mine, or explosive demand for a commodity. That kind of news makes any investor’s dream as the stock usually skyrocket and making a small fortune for shareholders. I was part of the dreamers too before I became a dividend growth investor.

After making lots of money from oil income trust (my 7-year-old could have made those picks for me), I decided to make a play on a big news. I bought a bunch of shares of a small mining company (penny stock) before it posted their exploration results. This worked for a few months as I was making over 100% return and then, boom! One day I came back from lunch and I had lost 50% of my initial investment. The stock plummeted to new lows since the company discovered… nothing.

While not all play or “do or die” investments, this story taught me a lesson: “commodities related businesses are volatile”. Many Canadians complain they haven’t had much of a return in the past 5 years. When you look at their portfolio, you realize that the bulk of their money is invested like the TSX60… Lots of energy and resources stocks.

Struggling with the U.S. currency rate

The best way to improve my portfolio diversification as a Canadian was to look elsewhere. As I mentioned, the Canadian market doesn’t include many international consumer staple, cyclical, industrial or tech stocks. I recently explained why I would rather invest in US stocks to cover international diversification. We are talking about the world’s largest, most stable and most diversified stock market.

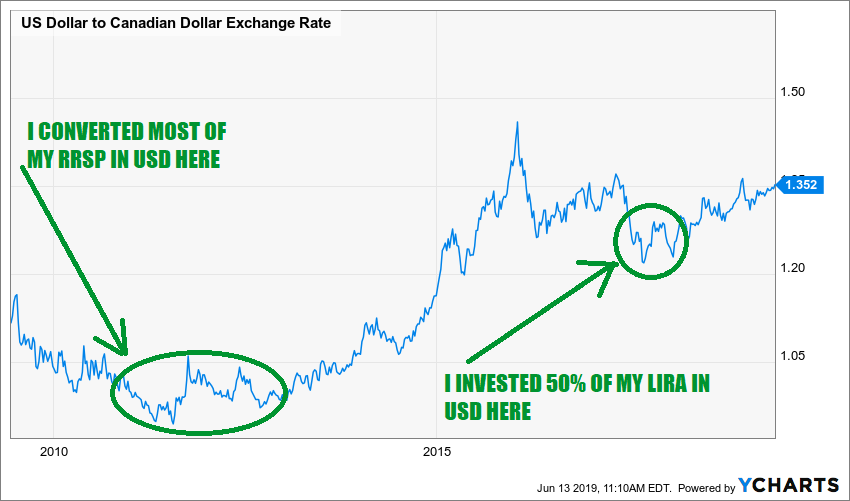

The problem we face as Canadians is that we need lots of loonies to even buy a Happy Meal!

Source: Ycharts

For once, I must admit that the two times I converted CAD to USD was pure luck. As you can see on the graph, it seems that I read the market correctly twice. But nothing is far from the truth. After buying The Dividend Guy Blog in 2010, I decided to build a dividend growth portfolio between 2011 and 2012. This was when I invested massively in US stocks through my retirement account (RRSP).

Then, when I quit my job in 2017, I received my money in September of the same year. My strategy included a 50% USD portfolio. I was right on time as the currency lost momentum a few months before I started investing.

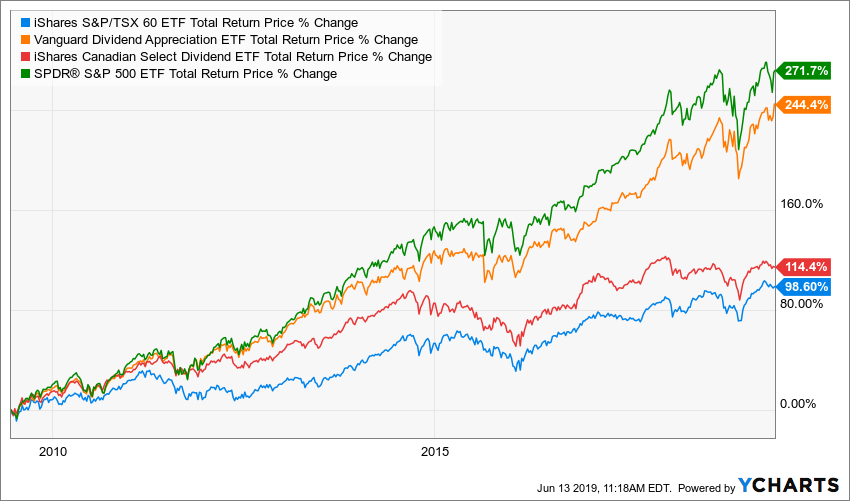

Besides luck, I would have invested no matter the currency rate. When I look at the fluctuation over the past 10 years, I see a 21% unfavorable headwinds for Canadian. That’s a 1.92% annualized rate. When you look the difference in returns when you compare both markets, you can see that the 1.92% difference is nothing compared to the expected return:

Source: ycharts

I know, it’s only 10 years of historical returns, and it’s not worth writing an academic paper about it. Still, in the most recent 10 years, investing in the US market was the right thing to do. I’m ready to bet on that strategy for the next 10 years. If you think the Canadian market will outperform the US market by more than 100% in the next decade, let’s bet $2 (USD) on that. But this article isn’t about the US market, so let’s go back to the Canadian stocks’ universe.

A few easy picks to start with

For any Canadian investors, there are a few easy picks that pretty much will agree on to start a portfolio. We have a few sectors where we are just amazing:

Banks (my ranking here)

Evolving in an oligopoly protected by the government, Canadian banks use their core business to generate strong cash flow and growth through various strategies. Some use capital markets and wealth management (RY.TO, BMO.TO, NA.TO), while othes go after the U.S. market (TD.TO) and Latin America (BNS.TO). They all show strong balance sheets, decent yield (~3-4%) and steady dividend growth (mid to high single digits).

Telecoms (my favorite is Telus (T.TO))

Similar to the Canadian banking playground, telecoms evolve in “closed markets” where 3 players split over 80% of the wireless sugar pie. There is a willingness from the government to open doors to more competition, but the Canadian market is a challenging adventure for many outsiders (ask Target (TGT) what they think of us!). Canadian telecoms offer small yield (yet still around 4-5%) compared to AT&T (T) and Verizon (VZ), but their growth perspectives are a lot more interesting.

Railroads (Canadian National Railway (CNR.TO) is by far my favorite in this sector).

You can’t really compete against railroads. While they are capital-intensive businesses, railroad operators are “alone” in their market as nobody can use their asset to transport goods and merchandise. They offer lower yield (roughly 1%), but are great stabilizers in one’s portfolio.

Utilities (Emera (EMA.TO) and Fortis (FTS.TO) are perfect for a retirement portfolio).

There are several strong utilities in the Canadian landscape. Many of them used the “banking strategy” where they used their core assets in Canada to generate cash flow and expand their business in other countries. Most of them are focused on green energies making them smart choices for the future, too.

REITs

I do not expect to touch this money for at least 30 years, so I am not actively looking to generate income. Canada shows a stable economy and one of the most solid banking systems. This is a great foundation for building healthy REITs in many sub-sectors. You can then find retirement, apartment, industrial REITs showing great yield, and dividend growth perspective. Among my favorites, you will find Brookfield Property (BPY.UN.TO), CT REIT (CRT.UN.TO) and Granite REIT (GRT.UN.TO).

Once you have picked a couple of stocks form these 4 sectors, you end up with 8-10 strong dividend payers that represent a solid core portfolio. If you don’t want to look pass the southern border to complete your portfolio, I might add a few more suggestions along the road. They are sometimes showing low yield, but they are all about dividend growth.

Dividend growth for Canadians

I guess the biggest challenge for Canadian investors is to find a considerable yield (3-4%) in various sectors. Once you have filled your portfolio with the 4 sectors I’ve mentioned, you still have several untouched industries such as consumer staples, consumer cyclical, tech and a large part of the industrial sector.

After further research, I was able to find interesting companies in other sectors. Most of them show lower yield than their American peers. However, if you combine those companies with the core portfolio we discussed earlier in this article, you can find a great balance between yield and growth. Here are two of my favorites (you can get more Canadian picks ideas here).

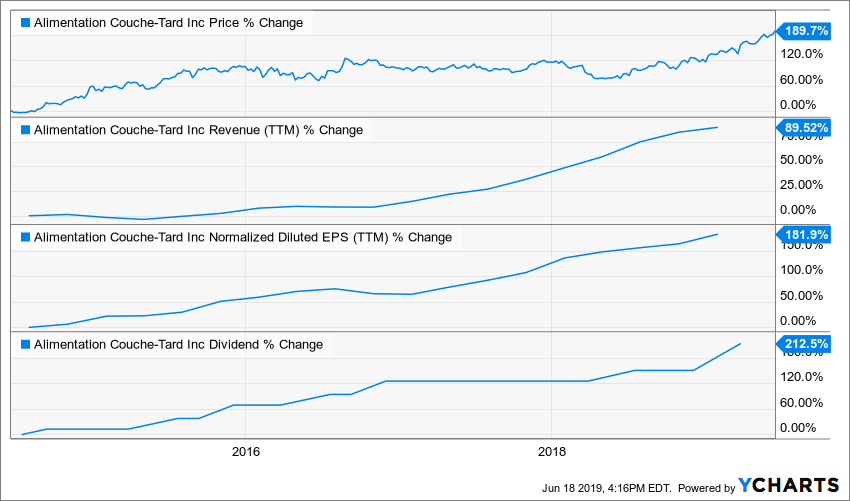

Alimentation Couche-Tard (ATD.B.TO)

Alimentation Couche-Tard is the largest convenience store operator in Canada and 2nd largest in North America. While constantly expanding its presence in the US and Europe, it successfully built a convenience store that includes daily-use products. Many stores are also combined with fuel service stations. ATD operates 12,081 stores (7,863 in North America, 2,708 in Europe and 1,510 internationally). Instead of simply selling chips and beers, ATD focuses on a superior offer including fresh food, private labels and strong product concept offerings.

An investment in ATD is definitely not for an income producing stock. However, if you are looking at the long-term, your dividend payouts will grow in the double digit for a while, and you will enjoy a strong stock price growth. ATD’s potential is directly linked to its capacity to swallow and integrate more convenience stores. Management has often proven its ability to pay the right price and generate synergy for each deal. ATD shows a perfect combination of the dividend triangle: revenue, EPS and dividend strong growth.

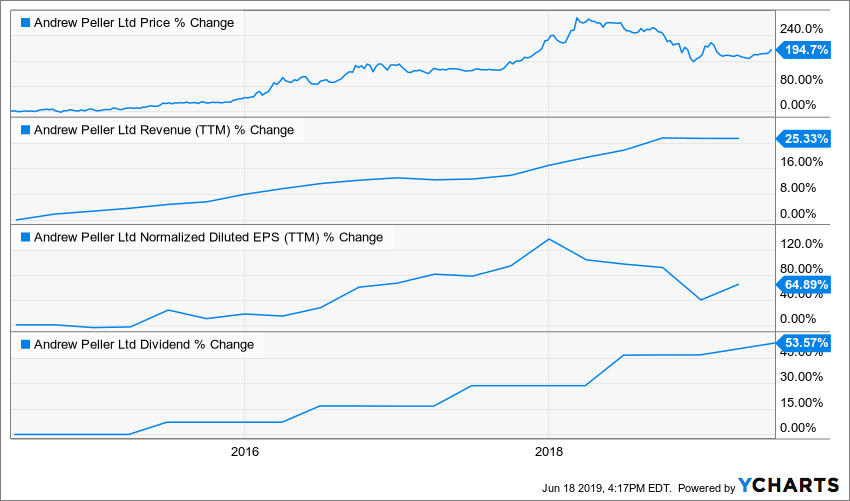

Andrew Peller (ADW.A.TO)

Andrew Peller owns wineries in British Columbia, Ontario and Nova Scotia. ADW not only produces its own wine, but also markets it along with other products. It owns several brands like Peller Estates, Trius, Hillebrand, Thirty Bench, Sandhill, Copper Moon, Kalona Vineyards Artist Series VQA wines and Red Rooster. Currently it has an estimated 14% share of its total wine market and a 37% share of domestic wines.

Andrew Peller is known to grow its revenues through acquisitions. Since 1995, management invested over $200M to purchase 17 vineyards. The company built a solid relationship with provincial liquor stores, but also maintained company-owned retail stores in Ontario. Andrew Peller is a dominant player managing a strong brand portfolio. The company posted a record year in 2018 and management has invested a lot during that year. We expect those investments in branding systems planning and production efficiency will translate into stronger earnings in the upcoming years.

Are you looking for more Canadian picks ideas? register to my new webinar (free instant replay if you register after June 27th). Click on the image below:

The post What is it to be a Canadian Dividend Investor? appeared first on The Dividend Guy Blog.