Investing when the market is high is not a simple task. You may think you found the right company, but the stock is clearly overvalued. Therefore, you wait until the market offers you an opportunity.

With one of the strongest starts of the year in the modern stock market history, it’s even more difficult to find fairly priced dividend stocks. It’s like trying to find water in the desert, right?

Believe it or not, there are opportunities in this all-time high market. Some companies are being punished for the wrong reasons and it’s up to you to pick them up. Here are two examples of what’s on my list right now.

UPS Didn’t Deliver Last Quarter

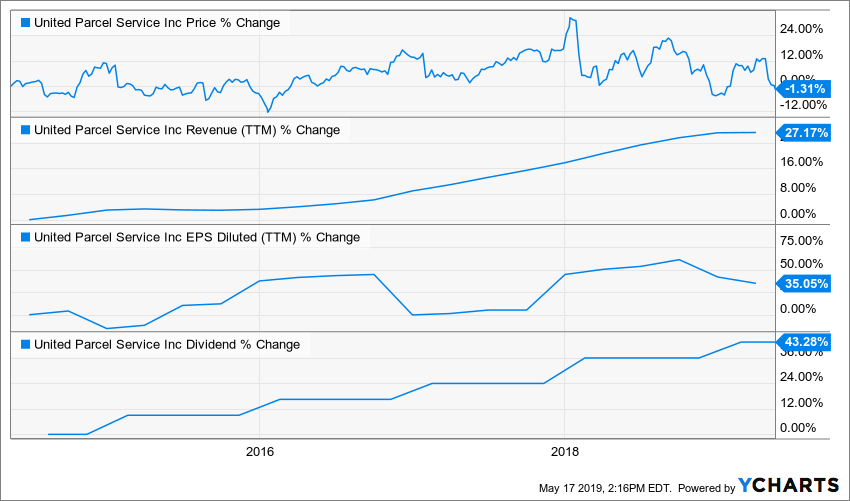

United Parcel Service (UPS) is the world’s largest package and delivery company. It employs over 430,000 employees in 2,500 operating facilities across 220 countries and has generated over $70B in revenue. UPS serves 1.5M pick-up customers and 7.9M delivery customers daily. The company has evolved in an industry where size does matter. United Parcel Service is by far one of my favorite industrial stocks. You can check out my complete list of dividend industrial stocks here.

Source: Ycharts

What’s the story?

UPS has failed to post consistency in their results from one quarter to the next. Sometimes, it failed to forecast the necessary resources required during the holidays, at other times it’s the weather, and finally, the economic slowdown in Europe. Because of this, UPS is bouncing up and down depending on their earnings. With a yield over 3.50% and a share buyback program in place, UPS makes a great candidate for your retirement portfolio.

UPS was hurt on the market on earnings day (once again!) since the company missed revenue growth expectations. Revenue increased 2.5% in the U.S domestic segment during Q1 to $10.48B vs. $10.7B expected. Growth in ground revenue per piece was up 2.9%. Segment operating profit was $694M vs. $756M a year ago. Unfortunately, international revenue was down 2.1% Y/Y to $3.46B. Revenue per piece adjusted for currency was up 2.3%. Segment operating profits rose 3% to $612M. Difficult weather also slowed down UPS’s activities. The company expects adjusted EPS to be relatively flat in Q2 compared to a year ago. For the full year, UPS sees EPS of $7.45 to $7.75 vs. $7.52 consensus and adjusted free cash flow of $3.5B to $4.0B vs. $4.05B consensus.

Potential Risks

UPS is highly dependent on the economy to perform. If businesses slow down, so does shipping. This might explain why UPS will never be a dividend aristocrat. The market doesn’t really like UPS right now. The stock will suffer even more if the economy slows down. The European parcel delivery market is more fragmented, opening the door to competition and putting pressure on margins. As UPS already deals with lower margins due to the increase of B2C business (home delivery), additional margins pressure is not a good thing.

Dividend Growth Perspective

UPS paused its dividend payment and didn’t increase it back in 2009, or during the 2001-2002 recessions. However, UPS is on a 10-year dividend raise streak now. The company has a very stable payout ratio and keeps it around 50%. Now, management should be able to hold to its dividend growth policy during recessions to please the market.

Investment Thesis

UPS should benefit from the current economic tailwinds. The unemployment rate is low and consumers are confident in the economy and will spend their money. As the economy rolls, UPS has more packages to deliver across the world. UPS is the largest player in a playground where size and economy of scale matters. UPS also shows the best margin in the industry because they are obsessed with efficiency. Also, online shopping means more delivery service options. While not a new phenomenon, this trend is growing, leading UPS to do more B2C business. Finally, international opportunities are rising. UPS captured important growth coming from it over the past decade with roughly +7% CAGR volume trend. The strength and efficiency of UPS network makes it the first choice for many businesses.

Enbridge is the Ultimate Dividend Pipeline

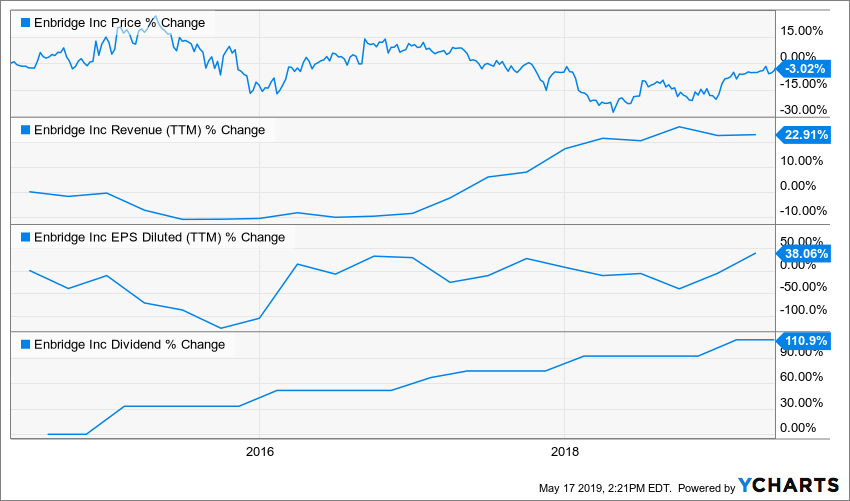

I’ve written a few times about Enbridge in the past couple of years. I think there is still room for growth in the upcoming years, though. Enbridge owns and operates an impressive network of liquid (Oil) and natural gas pipelines such as the Canadian Mainline system (which represents approximately 70% of Canada’s pipeline takeaway capacity). ENB can transport energy from coast to coast and from north to south. ENB shows a model of stability and predictability for shareholders as 98% of its estimated EBIDTA for 2019 is regulated.

Source: Ycharts

What’s the story?

If you have been waiting for the moment where Enbridge emerges from their troubles to dip your toe into the water, it may just be the time right now. In 2018, ENB was all over the news. Its ability to pay off its large debt, the Line 3 replacement and its regulators and finally, its mega-merger with all its other partners (SEP, EEP, EEQ and ENF) were discussed abundantly in the financial media. Fast forward to January 2019 – Enbridge has shown its ability to finance its projects ($22B) in a sustainable manner. Line 3 replacement keeps moving forward, the merger deal has been approved, and ENB increased its dividend by another 10%. No wonder ENB stock is up double-digits since the beginning of 2019.

ENB continues to move ahead with its long term plans, and their shares are slowly following an uptrend. Distributable Cash Flow (DCF) was $1,863 million for the fourth quarter and $7,618 million for the full year 2018, compared to $1,741 million for the fourth quarter of 2017 and $5,614 million for the full year 2017. ENB reaffirmed financial guidance for 2019 and 2020, with the midpoint of the DCF per share guidance range of $4.45 per share and $5.00 per share respectively. ENB keeps raising its dividend but suspended the DRIP effective with the December 1, 2018 dividend payment, thereby helping Enbridge move to a fully self-funded growth model.

Potential Risks

Companies do not pay a high yield for nothing. ENB raised its debts and number of shares in the merger with Spectra and more “balance sheet items shuffle” is expected with the integrations of all partners. Since pipelines require lots of capital to build and maintain, Enbridge may find itself in a position where cash is missing. After all, management has plenty of projects to fund, a double-digit dividend growth promise to keep and larger debts to repay. This could seriously jeopardize the company’s growth plans.

Dividend Growth Perspective

The company has been paying dividends for the past 65 years and has 23 consecutive years (2019) with an increase. ENB expects to increase its payouts by 10% through 2020. Management reaffirmed their dividend growth policy by announcing their 10% dividend raise for 2019. Since the pipeline business model is built around long-term contracts and predictable cash flows, I have no doubt this will happen

Investment Thesis

Enbridge clients enter into 20 to 25-year transportation contracts. The company is already well positioned to benefit from the Canadian oil sands (as its Mainline covers 70% of Canada’s pipeline network). As production grows, the need for ENB pipelines remains strong. Now that it has merged with Spectra, about a third of its business model will come from natural gas transportation. The company has a handful of other projects on the table or in development. Among those projects, is the Line 3 replacement. The company expects the completion of this project in mid-2019. In 2018, the company presented a plan to integrate all its partners into a single company. This will facilitate the company’s financial structure and should help maintain high credit standards.

Want more? I have a complete list coming up this Thursday!

Join me next week for a free webinar about Q2 earnings review. I’ll share my thoughts on the market and give you some of my favorite picks.

Register here (it’s 100% free)

Topic: Best Dividend Picks Q2 2019: Hidden Gems from the Desert

Date: Thursday, May 23th at 1pm EDT

Description: In this webinar, I’ll identify 5 dividend growth stocks that are on my radar and I’ll tell you why they are great opportunities. I’ll also share a few of my tricks to find those opportunities.

- You must register with Webinar Ninja to attend (if you did it in the past, no new registration is required). This is completely free and the webinar is free also. Webinar Ninja is the platform we use to run all our webinars. It works well and provides an optimal experience for everyone.

- The presentation will last about 35 minutes.

- There will be a Q&A session of about 25-30 minutes.

- The webinar platform works on Google Chrome or Safari from a laptop or computer. (not compatible with smartphones or tablets)

- If you can’t make it on time, there will be a full replay available, but you must register to access it.

Register here

Please forward this article to your friends, they may save money thanks to you!

I hope to see you at the webinar!

Cheers,

Mike, Passionate Investor

Disclaimer; I own shares of UPS and ENB

The post Two Dividend Stocks Being Beaten Up For The wrong Reasons appeared first on The Dividend Guy Blog.