Oh Boy Oh Boy! This market is making a lot of people nervous, huh? Considering what happened on the market over the past couple of weeks, I decided to do a “special edition” for my DSR Mike’s Buy List.

Each month, we issue The Mike’s Buy List for our DSR members. They get our best ideas for both U.S. and Canadian dividend stocks. The first Friday of each month, they receive our top 10 growth and top 10 retirement (yield over 4%+) investment ideas. Considering what happened on the market last week, I decided to share some of our picks with you.

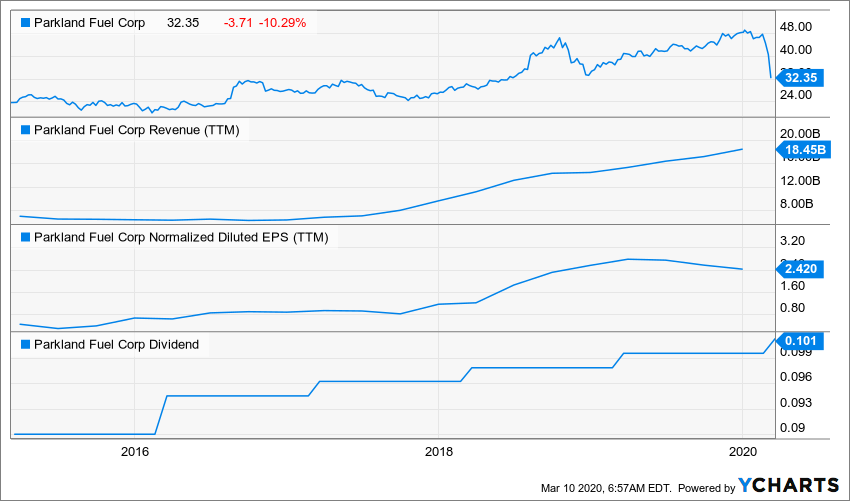

PARKLAND FUEL (PKI.TO)

What’s the story?

The thing with cyclical companies is there is always a good time to get them. Parkland fuel highly depends on North America’s economy for growth. As you can see, its growth by acquisition strategy has paid off as the company shows very consistent revenue increases. PKI is now the largest independent fuel distributor in Canada and will benefit further from economies of scale.

As a middleman, PKI doesn’t suffer from oil price volatility. The company focuses on distributing oil products and connecting clients at all levels with oil producers. The middleman always gets their commission. Plus, PKI’s appetite for growth by acquisition has made it a very successful company. PKI doubled its presence in the U.S. in 2018 through the acquisition of Rhinehart Oil.

2020 may not be a great year in terms of growth, but you can bet on the PKI stock price to bounce back when the economy levels out as fuel is still a basic component of our overall economy.

Business Model

Parkland Fuel is an independent fuel distributor in Canada. The company is North America’s fastest growing independent marketer of fuel. PKI delivers gasoline, diesel, propane, lubricants, heating oil and other high-quality petroleum products to motorists, businesses, households and wholesale customers in Canada and the United States. PKI is Canada’s largest fuel retailer and is looking to expand its activities in the U.S.

Investment Thesis

Parkland is another middleman. It doesn’t own any pipelines or extract any oil. It focuses on distributing oil products and connecting clients at all levels with oil producers. This is a perfect situation as PKI doesn’t suffer from oil price volatility. The middleman always gets their commission. Plus, PKI’s appetite for growth by acquisition has made it a very successful company. PKI doubled its presence in the U.S. in 2018 through the acquisition of Rhinehart Oil. As the oil market continues to struggle, other opportunities (like Husky) could appear on PKI’s radar. You can clearly see how Parkland is pushing its revenue and earnings higher year after year. PKI is a growth machine with a strong dividend triangle.

Potential Risks

An appetite for growth is always a bit dangerous when interest rates start rising. Management had a hard time generating strong profits over the past 5 years. It is one thing to grow your revenues, but you must find a way to make more money as well. The shares surge in early 2018 (+50% at mid-year) opened the door for the recent price drop for the second half of 2018. It should be a more stable year in 2019 as negative outlooks seem to be priced into the share price already.

Dividend Growth Perspective

I like the yield and the fact that management is paying a monthly dividend. So far, PKI has increased its dividend for 7 consecutive years. PKI obviously focuses on its growth by acquisition strategy, but management increased its payout by 2.04% in early 2019. We have now reduced PKI’s dividend safety score to 3. The dividend is safe, but management prefers using their cash flow to fuel growth instead of dividends.

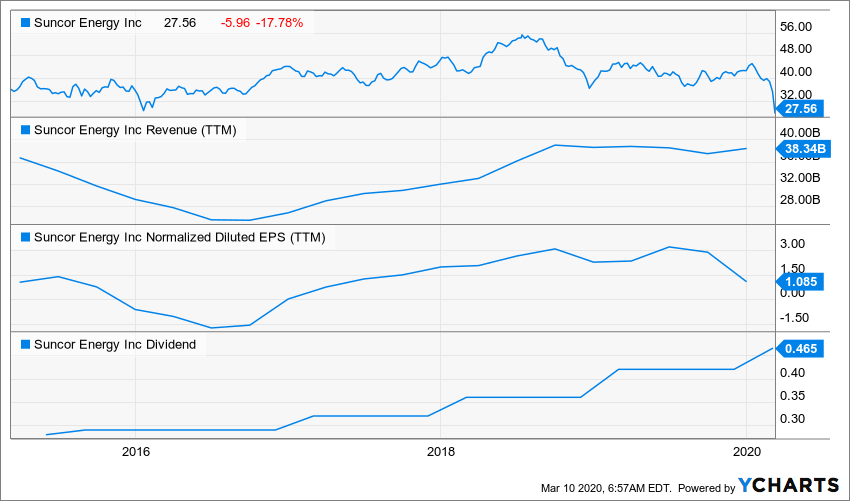

SUNCOR (SU.TO) (SU)

What’s the story?

Well, do I really need to tell you? As if the panic around the corona virus wasn’t enough, big oil players decided to flood the market. A few days ago, the big OPEC/Russia meeting ended without a deal to cut production. Now Russia and Saudi, the two biggest exporters, are saying they’re going to maximise production and flood the market. This is why the energy sector is down the sink. There are no exception for the market and all energy stocks are the same when the oil barrel goes down to hell, but you can make a difference as an individual investor. As long as you review the three major red flags for each company before making any decisions, you will do well.

Business Model

Suncor Energy is one of Canada’s largest integrated energy companies, operating in western Canada, east coast Canada, the United States, and the North Sea. The upstream portfolio includes bitumen, synthetic crude, and conventional crude, which helps to offset higher-cost oil sands production. Suncor’s upstream production is supported by its refining operations, which have a capacity of 462 thousand barrels a day. Production averaged 732 mb/d in 2018, and the company estimates that it holds approximately 7.5 billion barrels of proven and probable crude oil reserves.

Investment Thesis

At DSR, we are not enthusiastic about the oil businesses. During downturns, these companies see their cash flows melt and must pause their dividend growth if not be forced to cut their payments completely. Suncor is among the leaders in the Canadian industry and offers additional protection against down cycles due to its size and integrated model (it makes money from upstream, midstream and downstream activities). SU also made key acquisitions during the latest economic downturn and benefits from its leadership position to acquire smaller players. It should be able to use those assets once the oil price comes back to a more reasonable level. With such price drop, the yield is good and it’s time to “make an exception”.

Potential Risks

Suncor is mainly active in the oil sands production. Those operations require a high oil price to be profitable. SU can count on its integrated business model and its large size to navigate through challenging periods. However, this also limits its dividend growth possibilities. SU will continue to exploit existing projects, but expansion will be limited if oil prices remain low. At some point, total production of oilsands in Alberta could exceed pipeline capacity and prevent Suncor from realizing potential revenues. We can see how fast the stock drop when the oil price is affected.

Dividend Growth Perspective

During a market correction, the key to avoid panic is to track your dividend income (here’s how you can avoid making rash decisions). Suncor shows a strong balance sheet and could leverage its recently acquired assets to produce more when oil prices go back up. This should support a strong dividend growth policy. Considering their payout ratios well under control, investors can expect a high single-digit dividend growth rate going forward. However, keep in mind the oil industry rapidly changes from time to time.

Retirees Make These Fatal Investing Mistakes

I saw lot of panic since the beginning of the year. I hope you are holding on and that you are sticking to your investing strategy. Unfortunately, many retirees make costly investing mistakes based on common beliefs or make bad investment decisions based on fear. I think the biggest concern retirees have regarding their portfolio is probably the fear of losing money. Make sure you don’t do those common retirees mistakes in your portfolio. I’ve listed 4 of them and what you should do instead. I think it’s a good read especially during a market correction.

The post Two Companies That Will Have A Strong Rebound appeared first on The Dividend Guy Blog.