In September of 2017, I received slightly over $100K from my former employer, representing the commuted value of my pension plan. I decided to invest 100% of this money in dividend growth stocks.

Each month, I publish my results on those investments. I don’t do this to brag. I do this to show my readers that it is possible to build a lasting portfolio during all market conditions. Some months we might appear to underperform, but you must trust the process over the long term to evaluate our performance more accurately.

Performance in Review

Let’s start with the numbers as of April 4th, 2023 (before the bell):

Original amount invested in September 2017 (no additional capital added): $108,760.02.

- Portfolio value: $212,906.88

- Dividends paid: $4,829.25 (TTM)

- Average yield: 2.22%

- 2022 performance: -12.08%

- SPY= -18.17%, XIU.TO = -6.36%

- Dividend growth: +10.83%

Total return since inception (Sep 2017-March 2023): 100.36%

Annualized return (since September 2017 – 67 months): 13.25%

SPDR® S&P 500 ETF Trust (SPY) annualized return (since Sept 2017): 11.46% (total return 83.23%)

iShares S&P/TSX 60 ETF (XIU.TO) annualized return (since Sept 2017): 9.05% (total return 62.19%)

Dynamic sector allocation calculated by DSR PRO as of April 6th.

Quarterly Performance Review

At the end of each quarter, I feel like it’s Christmas: I’m excited to open my DSR PRO report and review my portfolio’s progress. As I have stated before, I don’t pay much attention to the total return for this period. What’re 3 months when you invest for more than 500 months? Even if you are 65 today, it’s fair to assume you’ll be investing for the next 20 years. Therefore, 3 months is only 1.25% of the time you will be investing.

Before I dive into my portfolio, I’d like to highlight what has happened in the market since everything started to go wrong in 2022.

The market isn’t that bad.

We didn’t know back then, but January of 2022 marked the end of the party and the start of a bear market for Americans. In Canada, we got lucky as the energy sector supported us for the first part of the year. As higher interest rates directly affected bond pricing, I don’t know many investors who made money in 2022.

When I read the headlines, I feel like we are in deep trouble, and the current market conditions will last a very long time. But when I look at the market realistically, I realize that the TSX is only down 2% (including dividends) and the S&P 500 is down 12%. It’s not the apocalypse many may want us to believe.

You know how “bad” 2022 was for my portfolio. I failed with my investment in Sylogist and suffered from major corrections at both Algonquin and VF Corporation. They both eventually cut their dividends in early 2023. For a dividend growth investor, that is possibly the worst-case scenario: I lost income and I lost capital to invest.

But this is only “true” if you focus on the bad investments I made. Similarly, to an individual person who is not just the product of his weaknesses or flaws, a portfolio is also not only represented by its bad investments.

When I look at my portfolio performance between January 2022 and April 2023, I see that I’m currently down 2.8% while the markets are doing much worse. I’m very close to the highest value I have ever shown (going from $108K to $224K). On the other hand, such crazy returns of doubling my investments over 5 years will eventually be adjusted during the bad months. It’s unrealistic to expect a 13% annualized return for an extended period.

I have shown double-digit returns since I focused on a dividend growth strategy in 2010. But those impressive returns are explained by three main factors:

#1 Luck (investing during this period was an amazing time for all investors).

#2 A robust strategy (dividend growers have repeatedly proven to outperform the market).

#3 Sticking to that strategy (I never shifted my focus or my strategy during tougher times).

I encourage you once again to stay invested and simply make sure your portfolio is well-invested. This is the key to weathering any kind of storm. But you are in luck as we have developed the tools to help you make sure your portfolio is well-invested! Let’s use the DSR PRO report (you can download my latest portfolio report here) to analyze my portfolio.

Lower yield, stronger returns

The first table in this report is the portfolio summary. Within seconds, I have a clear idea of what my portfolio looks like. Here’s a quick analysis:

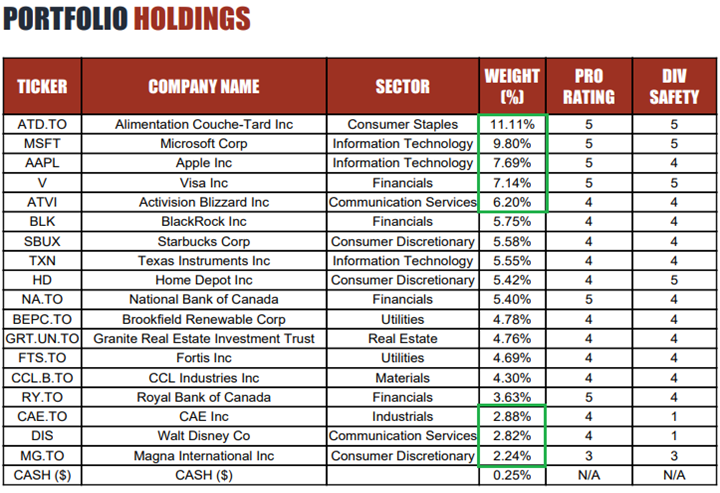

19 holdings: I want each of my stocks to have a definitive impact on my overall performance.

1.99% avg yield: I’ll concede it’s a bit low, but I recently sold Enbridge and replaced it with CCL. There is a 5% yield differential right there.

$4,291.23 in annual dividend payments: Not bad for a low-yield, high-growth portfolio. The yield on cost is now at 3.95%.

10.49% annualized dividend growth: My portfolio is filled with companies that are thriving and increasing their dividends generously.

33% of “Exceptional Buy”, 61% of “Buy” and 6% of “Hold”: I currently hold a great selection of stocks where I have more “buy+” stocks than the average in the database.

My conclusion here is that at first glance, my portfolio is in very good shape and that also explains my performance over the past 6 years. Now it’s time to dig into the sector allocations!

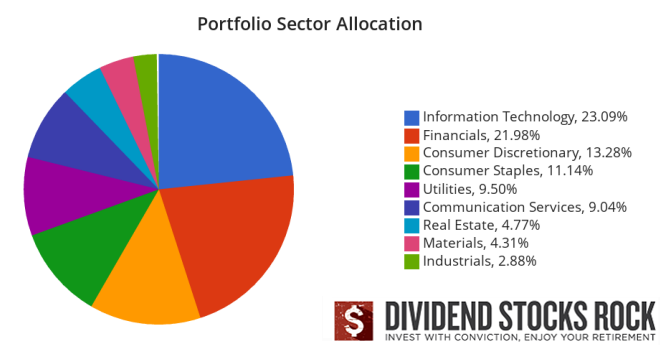

Better sector allocation?

In the introduction, I reported my sector allocation. It shows now that I have less exposure to tech stocks (23%) followed by financials (22%), Consumer Discretionary (13%) and Staples (11%). My top 4 sectors represent 69% of my portfolio. I have three other sectors having a real impact on my portfolio (5%+) with utilities (9.50%), Communication services (9%) and REITs (4.77%). Then, I close the portfolio with a small exposure to materials (4%) and industrials (3%). No healthcare and no energy sector investments. I do have CNQ and JNJ in my RRSP (Retirement account) though.

I used to have close to 30% in the information technology sector and now I’m surprisingly down to 23% without selling any of the tech stocks. Here’s the reason: Visa got moved from tech to financials. This opens the discussion about sector nomenclature. Some companies could be classified into various sectors. Depending on the information source you use, you may have some companies placed in different sectors. It’s confusing at first, but what really matters is to understand a company’s business model.

In my opinion, Visa should be 1/3 financials (it processes payments and transfers money), 1/3 tech (it uses powerful technologies in its operations and its key advantage remains in its network), 1/3 consumer discretionary (if people don’t travel and don’t use those rewards-packed credit cards, Visa will see its sales going down fast).

CCL Industries is another good example. It should be 50% materials (its entire business model is highly dependent on commodity prices, but it doesn’t sell commodities) and 50% consumer discretionary (the need for specialty films, labels and packaging is related to the economy).

The key to sector allocation is to make sure you are invested in many sectors that you understand. Sector diversification will smooth your returns and knowing how sectors work will give you confidence in buying and holding quality companies.

Once I complete evaluating my sectors, I then look at my stock allocations. I first want to make sure none of my positions exceed 15% (that’s the personal limit I’m willing to accept in my portfolio) and that my “educated guesses” and “falling knives” are toward the bottom of that list (e.g., I have lower exposure to them). This allocation limits my chances of suffering from a major loss if one of my largest holdings or my riskiest ones takes a hit.

ATD.TO is clearly one of my favorite holdings and I don’t mind having 11% of my portfolio in it. I see it as an excellent investment if we go into recession. MSFT, AAPL, V and ATVI are clearly there to generate returns. ATVI is the only educated guess of the group, but I’m sitting on a nice profit already. Plus, there is an increasing chance that Microsoft will acquire it at $95 (adding another 10-12% to my return on this investment).

After the spring clean-up, which I did not too long ago (selling SYZ.TO, AQN.TO, VFC and ENB.TO), I’m satisfied with my current portfolio. The only questionable security is CAE (will it reinstate its dividend in 2023?). I’ll hold it until the end of the year, and I’ll consider selling towards the end of the year if no changes happen. The same rationale applies to Disney, but the CEO has already mentioned they want to reinstate the dividend this year.

Trading on Margin

For those who listened to my podcast “The Moose on the Loose”, you know that I’ve used my margin account to acquire shares of TD Bank (TD.TO) during the “bank saga” initiated by the Silicon Valley Bank debacle. TD is on the radar for many reasons:

- 1/3 of its business is in the U.S.

- There is a deal pending to buy First Horizon for $13.4B USD (a US regional bank)

- It owns a 12% stake in Charles Schwab (which has reported a $47B loss on bond values)

- There is the negative sentiment around the Canadian housing market.

- There is a big incomprehension about how the Canadian banking system works.

I used the margin space in my Smith Manoeuvre account to add shares of TD after it took a hit. The reason why I used my margin was to capture an opportunity. When I created my Smith Manoeuvre, I’ve mentioned I wanted to use the margin for such occasions.

The idea of using a margin account is to boost your return by borrowing money based on your investments. This is a high-risk strategy that is not recommended for most investors. I’m already taking some risks by borrowing money on my house instead of paying off my mortgage. I’m adding an additional layer of risk by lending money to my margin account.

Why take so much risk? First, because we are talking about small amounts. I took $500 on my margin to buy some TD before my $500/month deposit happened on April 1st. I can already confirm that I took an additional $500 on my margin (not reflected on the next page of this newsletter) to add a little bit more of TD following the news that TD is one of the most shorted bank stocks with 3.3% of short interest.

Second, I can afford to lose $1,000 on a trade, assuming TD’s value would drop to $0. But we all know that seeing TD going into bankruptcy is a fantasy scenario. First, TD is an incredibly solid bank that is well-capitalized. Next quarter, they will report juicy profits once again. Second, the Canadian Government would not let one of the Big 5 banks collapse. That would be like wanting to kill the entire Canadian economy.

Third, my Smith Manoeuvre account is built to generate a maximum total return by taking additional risks. I want this account to be aggressive. It will likely please my younger members that are looking for additional spice in their portfolios. If it’s not your “cup of tea”, please feel free to skip the SM updates and focus on the pension plan portfolio. I’m just sharing different strategies to assist you in defining your strategies ?.

Smith Manoeuvre Update

The SM strategy is back! When you attempt any kind of leveraged strategy, you must be certain to follow these rules:

#1 Have a long-term horizon (minimum 10 years) to benefit from a full stock market cycle.

#2 Be comfortable with market fluctuations (your portfolio could go down 20%, as it’s part of the game).

#3 Be comfortable financially (have an emergency fund + the ability to pay off the debt without liquidating the assets).

I followed my rules and took a break after spending a bit too much in creating lifetime memories with my family in Africa. I’m now back with a new $500 monthly since March 1st.

So far, the Smith Manoeuvre strategy has worked well as the portfolio shows a total return of more than 7% while I paid less than 6% in interest (which is tax deductible). My current interest rate is 6.72% but I don’t expect it to stay that high for long. In the meantime, I’m buying great companies at good prices, and I can handle the interest rate now.

Slowly but surely, the portfolio is taking shape with 6 companies spread across 5 sectors. I aim to build a portfolio generating ~5% in yield across around 15 positions. I will continue to add new stock monthly until I reach that goal. My current yield is at 4.65%.

Here’s my SM portfolio as of April 4th, 2023 (before the bell):

| Company Name | Ticker | Sector | Market Value |

| Brookfield Infrastructure | BIPC.TO | Utilities | $563.85 |

| Canadian National Resources | CNQ.TO | Energy | $476.40 |

| Exchange Income | EIF.TO | Industrials | $585.64 |

| Great-West Lifeco | GWO.TO | Financials | $612.85 |

| National Bank | NA.TO | Financials | $583.98 |

| Telus | T.TO | Communications | $485.46 |

| TD Bank* | TD.TO | Financials | 578.76 |

| Cash (Margin) | -$73.78 | ||

| Total | $3,313.16 | ||

| Amount borrowed | -$3,500.00 |

*Please note that I’ve added another 7 shares of TD on margin after this update.

Let’s look at my CDN portfolio. Numbers are as of April 4th, 2023 (before the bell):

Canadian Portfolio (CAD)

| Company Name | Ticker | Sector | Market Value |

| Alimentation Couche-Tard | ATD.TO | Cons. Staples | $24,228.91 |

| Brookfield Renewable | BEPC.TO | Utilities | $10,321.42 |

| CAE | CAE.TO | Industrials | $6,178 |

| CCL Industries | CCL.B.TO | Materials | $9,311.40 |

| Fortis | FTS.TO | Utilities | $9,729.90 |

| Granite REIT | GRT.UN.TO | Real Estate | $10,653.44 |

| Magna International | MG.TO | Cons. Discre. | $5,026.00 |

| National Bank | NA.TO | Financials | $11,776.93 |

| Royal Bank | RY.TO | Financial | $7,856.40 |

| Cash | $591.37 | ||

| Total | $95,673.77 |

My account shows a variation of +$1,503.31 (+1.60%) since the last income report on March 6th. There were a couple of companies left to report their earnings in March, and below is an update on those stocks.

Alimentation Couche-Tard made an acquisition!

ATD reported a good quarter with revenue up 9% and adjusted EPS up 6%. The company experienced inflation in their costs, but the good margins on fuel sales more than compensated. Same-store merchandise revenues increased by 4.8% in the United States, by 3.5% in Europe and other regions, and by 2.3% in Canada. Same-store Road transportation fuel volumes decreased by 2.3% in the United States, by 1.2% in Europe and other regions, and increased by 0.5% in Canada. ATD also announced their firm offer to acquire 2,193 stores from TotalEnergies for €3.1B. This represents 100% of their retail assets in Germany and the Netherlands as well as a 60% controlling interest in the Belgium and Luxembourg entities.

Granite REIT is solid like a rock (see what I just did here?)

While the market remains unsure about Granite REIT, the company continues to report double-digit growth in revenue (+19%) and FFO per unit (+17%). AFFO payout ratio was 75% for the fourth quarter of 2022 compared to 84% in the fourth quarter of 2021. You can expect another distribution increase in 2023! Granite achieved average rental rate spreads on new and renewal leasing of 24% over prior or expiring rents driven primarily by renewals in Canada executed at 78% over the expiring rent, and by new leases and renewals in the United States executed at an average of 24% over the prior or expiring rents.

Here’s my US portfolio now. Numbers are as of April 4th, 2023 (before the bell):

U.S. Portfolio (USD)

| Company Name | Ticker | Sector | Market Value |

| Activision Blizzard | ATVI | Communications | $9,898.28 |

| Apple | AAPL | Inf. Technology | $12,462.75 |

| BlackRock | BLK | Financials | $9,329.74 |

| Disney | DIS | Communications | $4,489.20 |

| Home Depot | HD | Cons. Discret. | $8.931.90 |

| Microsoft | MSFT | Inf. Technology | $15,797.65 |

| Starbucks | SBUX | Cons. Discret. | $8,912.25 |

| Texas Instruments | TXN | Inf. Technology | $9,208.00 |

| Visa | V | Inf. Technology | $11,450.00 |

| Cash | $521.44 | ||

| Total | $91,001.21 |

The US total value account shows a variation of $3,974.50 (+4.57%) since the last income report on March 6th. All companies were covered during our February and March updates. We’ll receive more news next month!

I have discussed many of my holdings representing Opportunities from The Dividend Rock Star List in the podcast episode below.

Best Opportunities from the Dividend Rock Star List [Podcast]

My Entire Portfolio Updated for Q1 2023

Each quarter we run an exclusive report for Dividend Stocks Rock (DSR) members who subscribe to our very special additional service called DSR PRO. The PRO report includes a summary of each company’s earnings report for the period. We have been doing this for an entire year now and I wanted to share my own DSR PRO report for this portfolio. You can download the full PDF showing all the information about all my holdings. Results have been updated as of April 6th, 2023.

Download my portfolio Q1 2023 report.

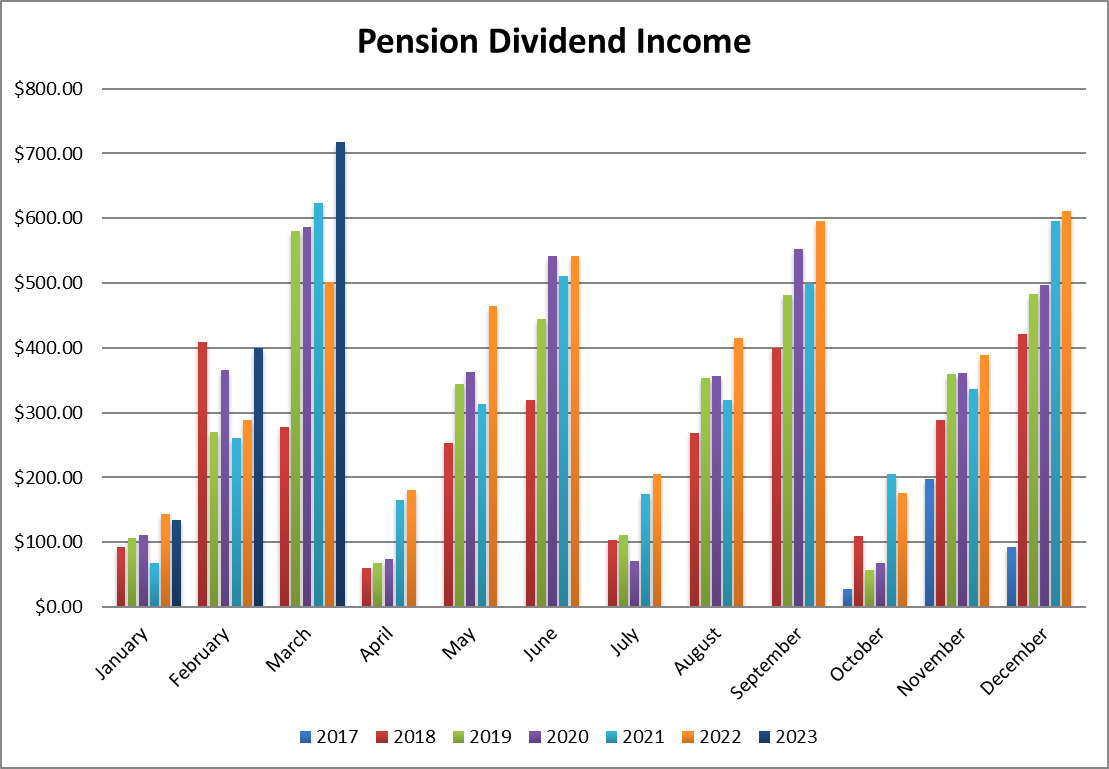

Dividend Income: $717.14 CAD (+42.88% vs March 2022)

This was a huge month as I received my dividend from Enbridge and then sold my shares. Therefore, I don’t expect such strong months going forward. I also received my first dividends from Home Depot and CCL Industries. Since I added more shares of Brookfield Renewable over the past 12 months, I show over $100 in dividend payments this month (compared to $17 last year).

Currency factors also contributed to boosting my US dividends by 7.5%.

Here is the detail of my dividend payments.

Dividend growth (over the past 12 months):

- Fortis: 82.4% (added more shares)

- Enbridge: +3%

- Magna: +11%

- Granite: new

- CCL Industries: new

- Brookfield Renewable: up from $17.07 (added more shares)

- Visa: +20%

- Microsoft: +9.68%

- Home Depot: new

- BlackRock: +2.46%

- Currency factor: +7.53%

Canadian Holding payouts: $458.44 CAD.

- Fortis: $96.62

- Enbridge: $142.89

- Magna: $43.90

- Granite: $34.13

- CCL Industries: $37.10

- Brookfield Renewable: $103.80

U.S. Holding payouts: $192.60 USD.

- Visa: $22.50

- Microsoft: $37.40

- Home Depot: $62.70

- BlackRock: $70.00

Total payouts: $717.14 CAD.

*I used a USD/CAD conversion rate of 1.3432

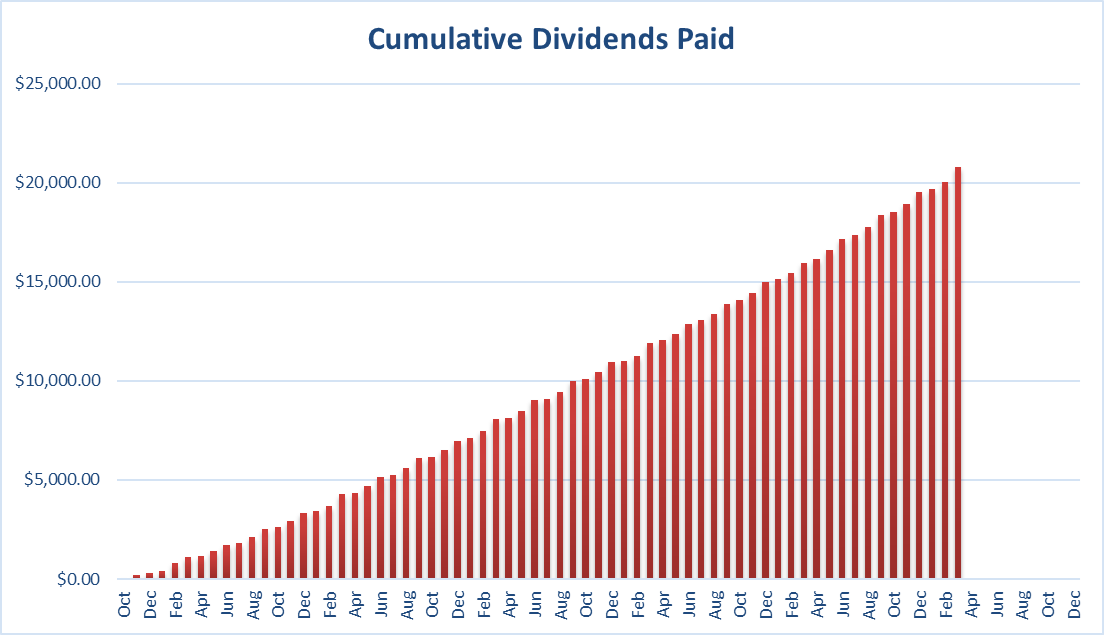

Since I started this portfolio in September 2017, I have received a total of $20,773.26 CAD in dividends. Keep in mind that this is a “pure dividend growth portfolio” as no capital can be added to this account other than retained and/or reinvested dividends. Therefore, all dividend growth is coming from the stocks and not from any additional capital being added to the account.

Final Thoughts

The recent spring cleaning has positioned my portfolio on a strong track. I’m confident that 2023 will be a great year for dividend increases. As for the total return this year, it will be highly contingent on whether or not we enter a recession during the course of the year.

I’m building some liquidity in this account which currently has slightly over $1,000 in cash assets. I’ll be looking to invest this money soon. I don’t expect to start a new position but rather to invest additional funds in an existing position. I like using dividends to rebalance my portfolio!

Cheers,

Mike.

The post Trading on Margin and Quarterly Performance Review – March Dividend Income Report appeared first on The Dividend Guy Blog.