A few weeks ago, I wrote an article about my best investing moves and the worst ones. As investors, we live various experiences and have the chance to learn from them. My fellow blogger ATL at Amber Tree Leaves commented on this article telling he that if could go back in time and start over again, he would immediately start investing with a systematic plan. The idea is to invest, even a small amount of money, on a regular basis. You could do it once a month or, even easier, invest every two weeks at the same time you receive your paycheck. If you choose the latter, it’s like reducing your salary at first, but you won’t feel the difference after a short while. After reading his comment, I thought; this advice is so simple, and it’s the best advice for all investors.

Time in the Market is the Most Effective Investing Strategy

We can spend all day debating about the best investing strategy. Some will tell you passive indexing with ETFs is way to go, some others will choose investing with an advisor and others like me will put their focus on dividend growth investing. The fact is that while I’m a firm believer in my own investing strategy, the truth is that being invested in the stock market for a long time remains the best strategy above all no matter what you do with your portfolio.

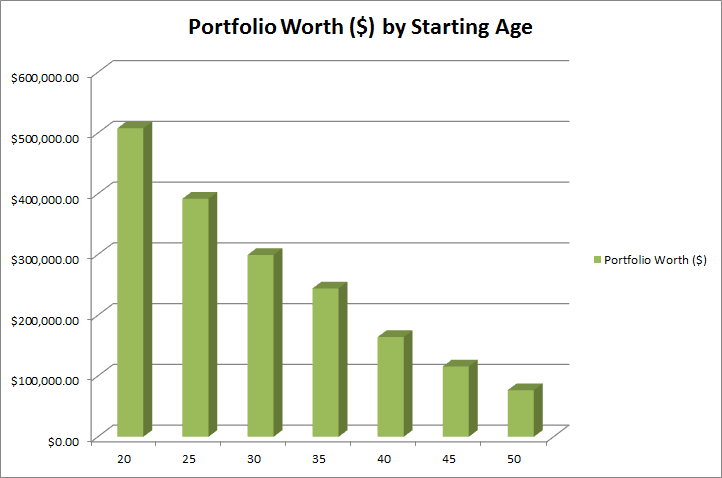

Let’s do some math to see how this works in real life. Assume you have $140 to invest bi-weekly. This would make a total of $3,640 per year. It’s not a big amount and it is easily affordable by just about anyone, at any age. I’ve used the Financial Mentor calculator to run several calculations. The idea is to start the scenarios at different ages, and stop at 65 to see how much your portfolio would be worth. I used a 4% investment return as a starting point:

source: author’s table

Data:

| Starting Age | Years Invested | Total at 65 |

| 20 | 45 | $507,810.53 |

| 25 | 40 | $391,898.63 |

| 30 | 35 | $299,322.34 |

| 35 | 30 | $244,379.51 |

| 40 | 25 | $164,272.61 |

| 45 | 20 | $115,777.11 |

| 50 | 15 | $76,933.18 |

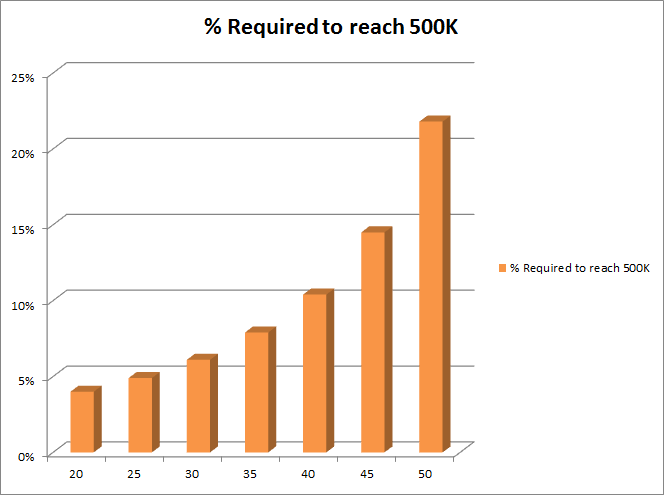

As you can see, it makes an incredible difference to start investing at the age of 20 ($507,810.53) vs starting only 10 years later ($299,322.34). In fact, starting 10 years later cost you over $200,000. Unless you are the next Warren Buffett, you will never able to compensate for this 10 years with better investing results. I’ve done some calculations to see what rate of return you need to achieve to compensate for not starting to invest at the age of 20:

source: author’s table

| Starting Age | Investment Return | Total at 65 |

| 20 | 4% | $507,810.53 |

| 25 | 5% | $504,913.29 |

| 30 | 6.10% | $501,553.57 |

| 35 | 7.90% | $509,782.21 |

| 40 | 10.40% | $504,570.31 |

| 45 | 14.50% | $504,410.92 |

| 50 | 21.80% | $502,293.74 |

You may think achieving 6.1% return is feasible if you start at the age of 30 and you are right. However, do you realize that this represents an increase of 52.5% on your original rate of return? And if you think it’s still not the end of the world, maybe you will change your mind if I tell you that if you start investing at the age of 20 and average a 6.1% return, you will reach the $1 million dollar mark at the age of 65 by simply investing your small $140 bi-weekly (total amount is exactly $1,023,697.93).

These calculations show us something that is now obvious: not matter how you invest, if you start early, you don’t need an astronomical rate of return to acheive financial freedom.

Invest Every Two Weeks and Reach Financial Freedom

I’m writing this article mainly because I wish I had read something similar when I was still in University. I would have spent less money on beer and clothing then I would have started investing this magical $140 bi-weekly. Even if I had invested this amount in a balanced mutual funds, I would still reach a 4% investment return over a long period of time and build a solid nest egg.

We all make the same mistake; we think saving money will be easier when we will make more. The problem is that more expenses come with a higher salary. In my early 30s, I was already a homeowner and a father of three. This makes my budget a lot higher and if I hadn’t started saving already, starting now would be extremely difficult. Since you don’t spend what you don’t have, if you invest the money directly into your retirement account right from your paycheck, you will just get used to living without this money.

This is very simple advice, and yet, it is the best you could ever give to a young person.