Several investors spend years working on their investing model. They are somewhat convinced they will find the magic formula nobody did before. I sometimes have the feeling that investors are just looking everywhere but right in front of them. I’ve always managed my portfolio having the word “efficiency” in mind. When you think about it, dividend growth investing foundation is linked to only 3 pillars I call the “Dividend Triangle”.

First, the company must make revenue. Without revenues, there is nothing, right? Then, those revenues must grow year after year to ensure the company’s sustainability.

Second, the company must be able to generate earnings from those revenues. Then again, if you are looking for dividend payment growth in the future, you need to see rising earnings as well.

Third, the company must pay an increasing dividend. If management is not on board with this policy, I quickly lose interest in the stock.

Now, let’s take a deeper look at each point of the Dividend Triangle:

Revenues

A business is not a business without revenues. Simple line, but many forgot about it during the techno bubbles! The “new economy” still has to bend to the “old economy” and showing revenues. What is the difference between a company making growing revenue from a company showing stagnating results? Competitive advantages.

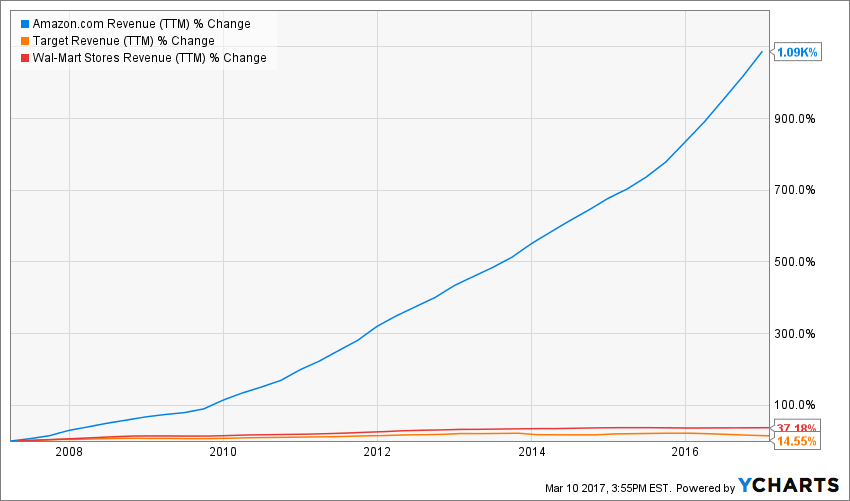

Can you tell me why Wal-Mart (WMT) and Target (TGT) revenues are stagnating while Amazon (AMZN) revenues are booming?

Source: Ycharts

Because Amazon is the leader in ecommerce, a growing industry. You are going to tell me that you don’t care about AMZN because it doesn’t pay dividend. I hear you. However, this also tells you a lot about TGT and WMT… do you still hold them in your portfolio? Because with limited revenue growth combined with competitors putting their competitive advantage in their face, I doubt TGT and WMT will be the most generous dividend growers in the next 5 years.

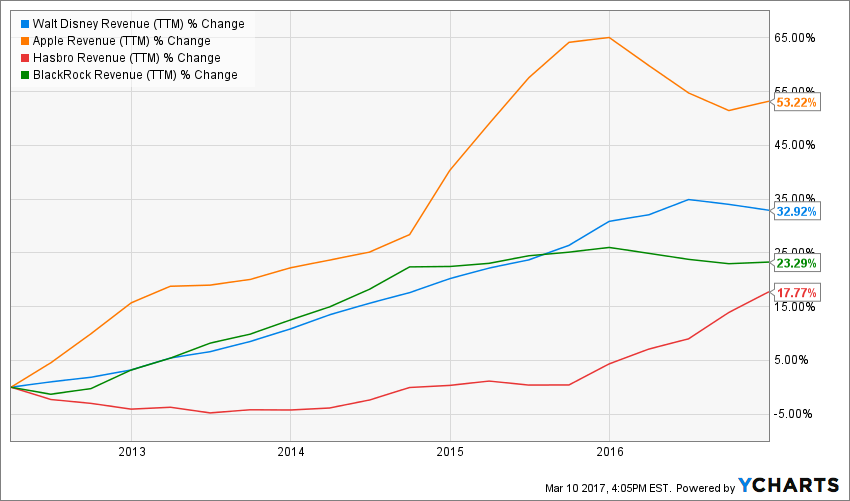

What you are looking for is company with strong competitive advantage enabling them to grow their revenue. Companies such as:

- Disney (DIS): The company has developed a strong expertise in starting from popular movies to cross-sell tons of products.

- Apple (AAPL): Their dominance among the smartphone industry continues to pay off.

- Hasbro (HAS): Their expertise in licensing other’s products have reached its climax when they stole Disney deal away from Mattel (MAT).

- BlackRock (BLK): The largest investment firm in the world… enough said.

source: Ycharts

Even in a tough market where revenue growth is hard to find, those companies are able to pull out some interesting numbers.

Unfortunately, revenues don’t always go up. Sometimes, you just need to be patient. There are currency headwinds, recessions or temporary situations that will crush a company financial statements from time to time. This doesn’t mean it’s a bad company or you should sell the stock. However, deeper analysis is then required to make sure the company still has what is necessary to grow in the future.

Earnings

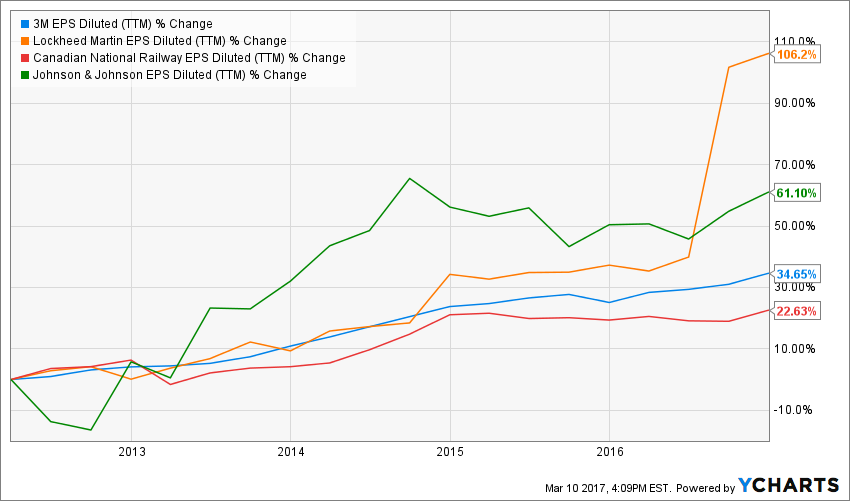

You can’t give money if you don’t make money, right? Then again, this is a very simple statement. Still, if earnings don’t grow strongly, there is no point of thinking that the dividend payment will increase indefinitely. Even through tough times, some companies can pull out great earnings numbers:

Source: Ycharts

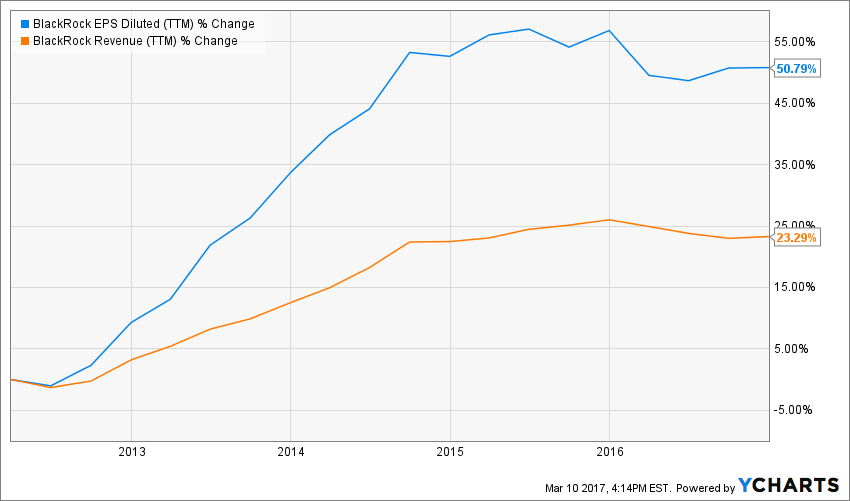

Similar to revenues, earnings don’t always go up. In a perfect world, all companies you pick would look like this:

Source: Ycharts

Even then, it’s not exactly perfect as I wanted to find a company showing a 50% growth for both EPS and revenues. I’m pretty sure you get the point: you should aim at company that are able to growth both revenues and earnings with a similar trend. Why? Because they become highly predictable in the future and when everything go up at the same time, life is a lot easier for management!

I must warn you of something though: earnings is an accounting number. This means it’s not related to what’s happening in the company’s bank account. Over the long run, no accounting tricks can convince an investor that the company is making money if it doesn’t. However, short term EPS peak could be the result of a one-time sale or one-time event that shouldn’t be factored in. For examples, Disney movie division had a very strong year in 2015 with the release of their first Star Wars episode. It’s great for earnings, but then, the company will have to find other blockbuster movies in the upcoming years to repeat their record year.

Dividend Payments

Last, but definitely not the least, dividend payments is the *obvious* backbone of any dividend growth investors. But I don’t mind the dollar amount or the yield, I solely focus on dividend growth.

When a company shows growing revenues and growing earnings, it can think about showing continuous dividend growth. Don’t forget that the money spent on shareholders is gone from the company. This means it will not help the business generate additional revenue in the future. This is why management must build a strong business model to ensure it can continue paying their shareholders.

I’ve repeated it many times on this blog, but if there is one metric I would have to follow, it would be dividend growth. Growing payments will cover inflation forever and boost your return. In fact, did you know that about half of the S&P 500 returns is coming from dividend payment? If you aim at dividend growers, you are basically picking up from the cream of the cream of the market.

However, I always doubt management when they are becoming overly generous. A double-digit dividend growth is surely fun, but it is not sustainable over the long haul. For this reason, I always use more conservative numbers than the past 5 years dividend growth when I use the Dividend Discount Model (DDM) to assess the value of my holdings.

Have you noticed yield isn’t part of the equation?

Yup, you read it right. The dividend yield is not part of my Dividend Triangle. In fact, I give very little weight in my investing process. Why is that? Because when you pick up a strong company growing its dividend, its yield become a minor play in the equation. What you “lose” in yield, you will get it back in stock appreciation. What do you prefer: having hold WMT shares over the past 10 years or DIS?

Source: Ycharts

I know DIS yield has been historically around 1% and 1.5%, but look at the stock return!

Get the Job Done for You!

Over the past decade, I’ve been blogging about dividend investing. My biggest achievement is Dividend Stocks Rock (DSR), a made-for-you dividend stock research service. Therefore, while you are at work, running at the daycare or simply golfing over the weekend, my team and I are researching the market full-time to find the best opportunities. In other words, you can hire us to become your stock research assistants.

How does it work?

We have built a whole platform with everything you need to build and manage your dividend growth portfolio:

- A monthly newsletter offering top picks for each industry;

- Taylor made portfolio models providing buy & sell alerts;

- 70+ stock cards to save you time doing research.

- 8 dividend stocks lists to simplify your stock selection process;

DSR has been built with the investor in mind. This is why it is way cheaper than mutual funds or broker fees.

Interested?

Click here to learn more about our services and the special price I have for you.

Disclaimer: I hold AAPL, DIS, HAS, BLK in my Dividend Stocks Rock Portfolio.