I don’t usually cover small caps on this blog but one of my readers asked me to take a look at Supremex (SXP.TO), the largest envelope maker in Canada. Supremex Inc is engaged in the manufacturing and sale of standard and custom envelopes, labels and related products. Its products portfolio includes Stock envelopes, RFID card protectors, File folders, Bubble mailers and Degradable window film.

As I mentioned previously, the company is a small cap (not even $140M) but pays a dividend yield of 4.21% and the stock exploded by over 50% since the beginning of the year. Since it’s a leader in its industry, I decided to take a deeper look and analyze the company.

DSR Quick Stats

Sector: Basic Materials

5 Year Revenue Growth: -4.52%

5 Year EPS Growth: -6.00%

5 Year Dividend Growth: 9.86%

Current Dividend Yield: 4.21%

What Makes Supremex (SXP.TO) a Good Business?

After looking at the DSR quick stats, I’m not sure it’s worth thettime to continue, right? But there must be a reason why the stock grew so fast recently. Supremex owns 60% of the envelope making industry in Canada, a dying business to be honest. This is why revenues and earnings are on a slump over the past 5 years.

But here’s what happened recently; SXP’s efforts to build a new business segment is paying off. While regular envelope packaging is heading nowhere, special packaging requirements coming from the online industry is booming. The point is we don’t send letters anymore and companies bill us “electronically”, but we spend more and more time buying online. These purchases have to be delivered, and guess what; Supremex understood the market needs in terms of delivery options.

This is not only a booming industry, but it is also offering higher priced products since you don’t want to receive a broken box after ordering from Amazon.

How SXP fares vs My 4 Dividend Investing Metrics

We all have our methods for analyzing a company. Over the years of trading, I’ve evolved through several stock research methodologies from various sources. This is how I came up with my 7 investing principles of dividend investing. The first four principles are directly linked to company metrics. Let’s take a closer look at them.

Principle #1: High dividend yield doesn’t equal high returns

In the past few years, the dividend yield climbed and went up to 12% in 2013. The market didn’t like SXP’s main industry (I can’t blame investors for being smart!) and the stock price was very low pushing yield to a ridiculously high level.

We rarely see this, but the company was able to reverse the trend and catch investors’ attention once again. We can’t say this new trend will remain, but the dividend yield is now back to a more reasonable level. Therefore, it currently meets my first criteria.

Principle#2: If there is one metric, it’s called dividend growth

SXP doesn’t show a very long dividend payment history. I usually prefer companies with stronger history providing me more metrics to look at. However, I can’t say it is headed in the wrong direction either. The board increased the dividend by 25% last year through two consecutive dividend increases.

Principle #3: A dividend payment today is good, a dividend guaranteed for the next ten years is better

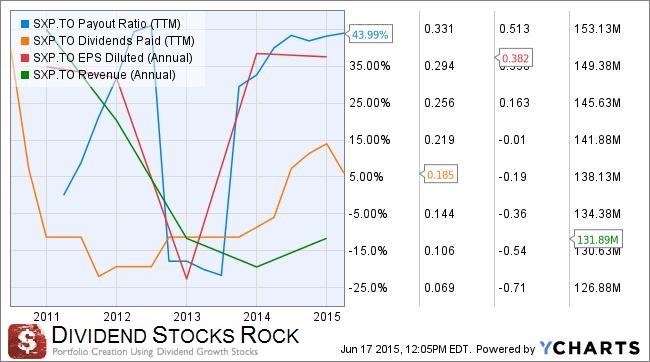

Then again, SXP shows an interesting payout ratio. At 44%, the company is able to keep its dividend payment and probably increase it again in the future. However, we have to go beyond the metrics; right now, we have a relatively low payout ratio, but will business continue to generate higher profits or is this just a value trap?

Principle #4: The Foundation of dividend growth stocks lies in its business model

Metrics are interesting to look at but they only tell you about a story that already happened. It’s harder to see what is coming. I understand the evolution of the business planthat Supremex has implemented, results are there to support their move, but still, I’m not convinced.

The company also focuses on increasing its presence in the US market. So far, it has paid off and the weak Canadian dollar has pushed profits up for this initiative. While playing with our southern neighbors is paying off right now, Supremex might hit a wall as competition is much stronger on the other side of the border.

What Supremex Does With its Cash?

Supremex did a good marketing job catching investors’ attention with 2 dividend increases in 2014. This is how SXP used its cash recently; by paying a juicy dividend. The company is generating positive cash flow and is showing good payment sustainability.

Should You Buy SXP.TO at this Value?

I’m not going to use the Dividend Discount Model or the P/E ratio analysis for this company. In fact, the metrics are too hectic to use any kind of valuation without calling it witchcraft.

I would simple mention that SXP.TO represents a fair share of risk in a portfolio:

#1 It’s a small cap

#2 It is evolving in a dying industry (revenue from classic envelopes is expected to decrease by 4% annually through 2016)

#3 Special packaging business is growing but other competitors might enter the market

What I Would Do With SXP.TO if I Had 10K in Hand

I’m known to take risk in my dividend portfolio. Since I hold a “growth” section and a “core” section, some riskier picks are allowed in my investing strategy. At the moment, I don’t see enough of a good thing to invest in SXP.TO and would not invest in this company. Now the dividend yield is around 4% in a very slow business, I don’t see how you can make more money vs how much you can lose in the short term. Because I don’t believe this business will surge, I won’t consider SXP.TO for my portfolio.

Disclaimer: I do not hold shares of SXP.TO at the moment.