I believe taking care of my portfolio is like taking care of my body. It requires simple actions that are difficult to maintain over the long run. I’ve recently discussed some basic principles to get your portfolio in shape in “How’s Your Beach Money?”. I wanted to go a little bit deeper with this post and describe a step by step methodology I use to make sure my portfolio is always in top shape.

It is one thing to build a great portfolio, it’s another to keep it at the top of its shape. Over time, you may have overlooked some of your holdings. Long-time bull markets have this effect on investors; it makes us complacent and we start to think we are geniuses. Here’s a checklist of items you must consider to make sure your portfolio don’t grow fat and lazy. After all, the whole purpose of investing money is to have it work harder for you, right?

Picture credit

Step #1 Track your portfolio quarterly

I personally track down results on a quarterly basis for all my holdings. I make sure each company performed well over the past quarter and assess their growth vectors going forward. I rather follow companies quarterly as I get consistent feedback on what’s is going on. I take notes each time and read what I wrote in the last 3 and 6 months. This is how I usually identify potential threats as they usually slowly develop one earnings report after the other. If you have missed a few quarters lately and you are satisfied by the fact the stock market brought back most of your stocks to peak value, then you probably keep stocks you shouldn’t.

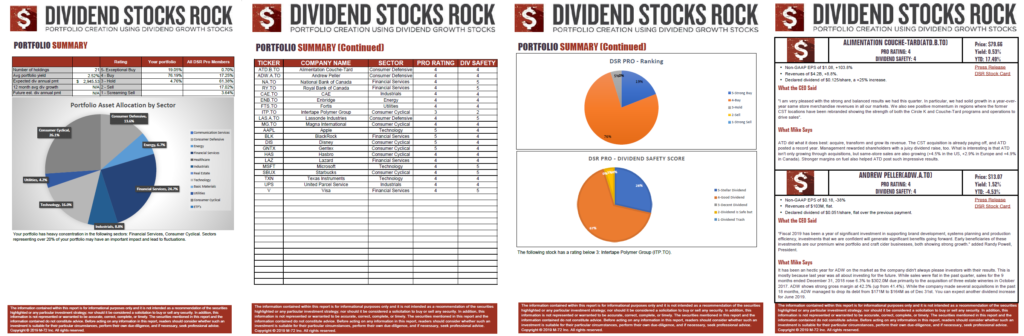

I’m now lucky enough to have my own portfolio reviewed by a tool I developed with my partner. Each quarter, we run an exclusive report for Dividend Stocks Rock (DSR) members called DSR PRO. The PRO report includes a summary of each company’s earnings report for the period. We have been doing this for an entire year now and I wanted to share my own DSR PRO report for this portfolio. You can download the full PDF giving all the information about all my holdings.

Download my portfolio Q1 2019 report

Tracking your investing results is like tracking your running performance or your weight on a regular basis. It’s very easy to relax over the weekend with a glass of wine and tell yourself you are too busy to run during week days. Do that for a few years without taking care of your body and you will wake up with several extra pounds one day. However, if you make sure to track metrics regarding your health on a regular basis, chances are you will put a plan in place to make sure you don’t go overweight. It’s exactly the same thing for your money. If you don’t track your quarterly results, you miss on where your portfolio goes.

Step #2 Clean your portfolio – get rid of that fat stock!

Some investors keep their winners forever.

Some others keep their losers until they worth nothing.

What’s the best strategy? Is there a way to know which holding to keep and which one to let go? First, what happened in the past 12 months or 5 years, already happened. Therefore, if you hold a stock showing a 300% return, it just means you made a great investment. It doesn’t mean that it will continue to grow at this pace in the future. Some will, some won’t. A similar rationale can be applied to losers. Here’s my process to make sure I don’t get caught with bad holdings going forward:

Eliminate non-dividend-growers

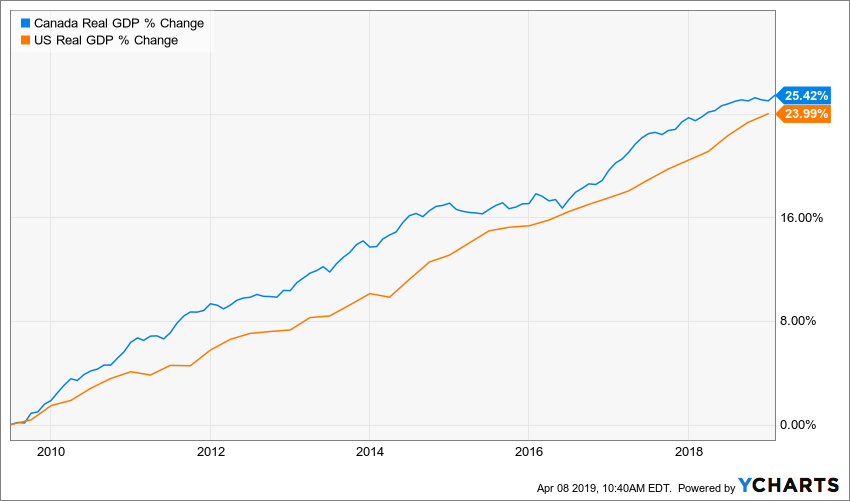

My first criteria to sell has been a dividend cut. This is an automatic sell for me. I’ve detailed the reasons why I think you should sell your shares the moment the company announces a dividend cut. The second reason why I get rid of a company is the absence of dividend growth. A company struggling to increase its dividend payment right now, is most likely the one that will cut it once we reach a recession. Over the past 10 years, both U.S. and Canadian economy found a way to steadily grow:

Source: Ycharts

When interest rates are at their lowest levels for a decade and the economy is growing, the least you can expect is a decent dividend growth from all your holdings. Those who failed you during this exceptional time, will continue to fail you in the future. Doing business is not going to get easier in upcoming years as many expect a recession sooner or later.

Eliminate those who don’t grow period

After looking at the company’s dividend growth policy, the second item on my list is the overall growth. Is the company growing its revenue? Earnings? Cash flow?

One basis of my investment strategy relies around the dividend triangle:

First, the company must make revenue. Without revenues, there is nothing, right? Then, those revenues must grow year after year to ensure the company’s sustainability.

Second, the company must be able to generate earnings from those revenues. Then again, if you are looking for dividend payment growth in the future, you need to see rising earnings as well.

Third, the company must pay an increasing dividend. If management is not on board with this policy, I quickly lose interest in the stock.

The rationale applicable to the dividend growth policy is also applicable to the company’s overall growth perspectives. A company that doesn’t show grow vectors right now should most likely be eliminated from your portfolio. We can’t predict or prevent the impact of the next recession on our portfolio. However, we can make sure we hold strong companies that already have a clear plan for growth in the upcoming years.

Disney (DIS) will start streaming this year, Apple (AAPL) is growing its service business like there is no tomorrow, Starbucks (SBUX) is opening a series of new restaurants in China, Alimentation Couche-Tard (ATD.B.TO) is always preparing its next acquisition, Enbridge (ENB) has for over $20B in projects for the upcoming years and Royal Bank (RY.TO) is targeting wealth management and the US market. Those are just a few examples picked from my current portfolio.

Finally, eliminate those who don’t make the cut anymore

Whenever you add a position to your portfolio, it’s because you found something interesting on the market. You have researched it well using your own investing rules (here’s an example of my investing process) and found enough reasons to pull the trigger and use your hard earned money to buy shares. This is commonly named your “investment thesis”.

Once you have reviewed basic metrics such as dividend growth, revenue, earnings and, cash flow, you are able to dive a little bit deeper and make sure the remaining companies still meet the reasons why you bought them in the first place. This is usually how I decide if I keep my winners or not. Some companies just did great for a while, but their business or environment changes and it’s now time to let them go. On the other hand, some companies keep reinventing themselves and find new growth vectors go keep-up with my expectations. A great example of such a firm would be Microsoft (MSFT). The company did well for a while with its Windows and Office suites. Now, it targets the cloud business and multiple their services offered to corporations.

Step #3 Don’t drink the high yield protein shake

Now that you have got rid of the fat in your portfolio, you may be tempted to take shortcuts. I remember the very first time I went to the gym. I got my personal trainer, did my tests and followed a personalized program. I was tracking my results, losing fat and gaining weight muscle. This felt great! Then, my trainer offered me to take protein shakes and stuff like that. It would enhance my performance and help me grow my muscle faster. While protein shakes seem to work very well, such products must be taken with moderation. If you go hardcore on shortcuts to get fit rapidly, you may end-up in the steroid game and won’t be a winner anymore.

I have a similar approach when I pick a dividend stock; I don’t go for the shortcut and pick the highest yielding companies. I wrote a detailed article about why I think High dividend yields don’t always equal high returns. I totally understand why income seeking investors are looking for generous companies. But many of those would not pass my second step as they won’t show any dividend growth.

If you selected companies that can increase (modestly) their dividend and offer a yield over 4%, that’s great! But keep in mind most of those Business Development Corporations (BDC’s) paying 8% to 12% yield weren’t there during the last crash. How do you think they will fare once they hit a brick wall? Do you think both your revenue and your share value will keep-up with your expectations?

Step #4 Sector allocation matter – it’s like your menu

One thing I’ve noticed after reviewing so many different portfolios through DSR is how so many investors think they are safe having 30, 40 even 50% of their money invested in a single sector. This reminds me of people eating a very strict diet revolving around 2-3 types of food. This may work over a short period of time, but if you want to live a great life and feel healthy, a balanced menu with no excess is a lot easier (and sustainable) to get results.

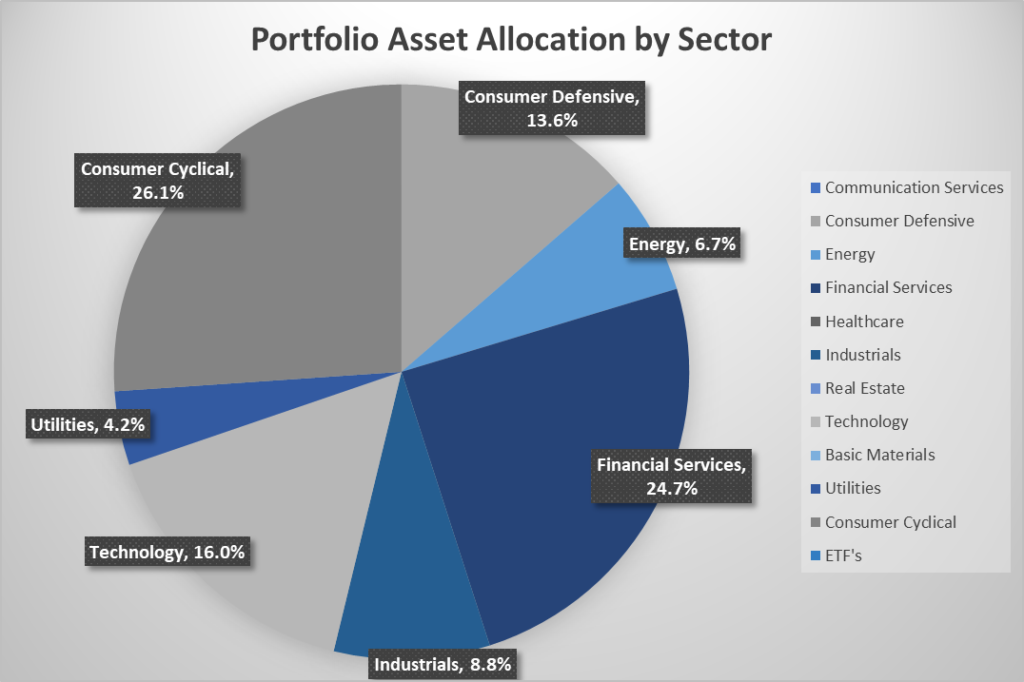

As you can see, my current sector allocation includes 8 sectors and none of them are more important than 26%:

Source: Author’s pension account sector allocation as of March 2019.

In my consumer cyclical picks, I have two auto part markets (Magna International (MG.TO) and Gentex (GNTX), a duct tape manufacturer (Intertape Polymer (ITP.TO)), a coffee shop operator (Starbucks) and an entertainment king (Disney (DIS)). They are not likely to get influenced by the same events.

I have a similar approached with different sub-sector in the financial services with 2 banks (Royal Bank (RY.TO) and National Bank (NA.TO)), two assets managers (BlackRock (BLK) and Lazard (LAZ) along with a payment processor (Visa (V)).

My portfolio would have been a lot more subject to fluctuations (and poor performances during downturns) if I had selected the 5 big banks for my financial services and picking Ford (F), GM (GM), and Harley Davidson (HOG) on top of my two auto part markets for consumer cyclical.

If you are overweight in a specific sector, maybe it’s time to revisit step #2 and apply it to that sector. Get rid of the fat and pick some super food in another industry!

Step #5 Muscle-up with dividend growth

Once you have cleaned-up your portfolio, you will likely have some cash in hand. I’ve recently explained why I think you should put all your money at work… all the time. In fact, I ran some calculations and showed that waiting in cash was likely going to play against you in pretty much all situations… unless you are incredibly lucky (check the results of those calculations here).

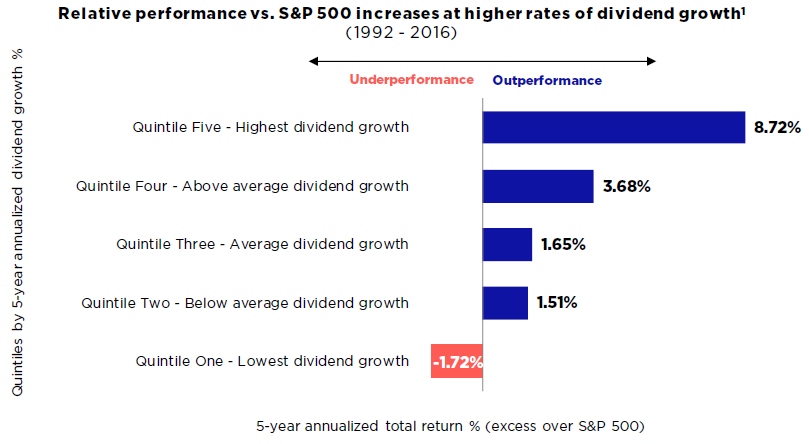

What better place to invest your money than in dividend growers? Those companies are usually doing well during the bull market and get less affected by bear markets. Following this strategy, I’ve finished 2018 in positive territories and started 2019 in full strength. Why? Because I kept my money invested. This is one of the lessons to get from 2018. But you don’t have to believe me, you can also trust this graph:

Source: Bloomberg, Reality Shares Research. Past performance does not guarantee future results.

Final Thought; Consistency is key

If you have been investing in the past decade, you probably show impressive results. Don’t get those returns blind you for the upcoming years. Staying in good shape and making sure your portfolio keeps posting strong results is a matter of consistency. Make sure you don’t sit back and enjoy the ride. Don’t be afraid to get rid of your past winners if they don’t have what it takes to keep-up. You can also keep your long-time performers if they consistently renew their business model and evolve with their environment. The same rationale applies to your losers. Don’t get rid of them for nothing, but if you do, make sure you invest your money in dividend growers.

The post Portfolio Fitness; Tricks to Train Your Money To Work Harder appeared first on The Dividend Guy Blog.