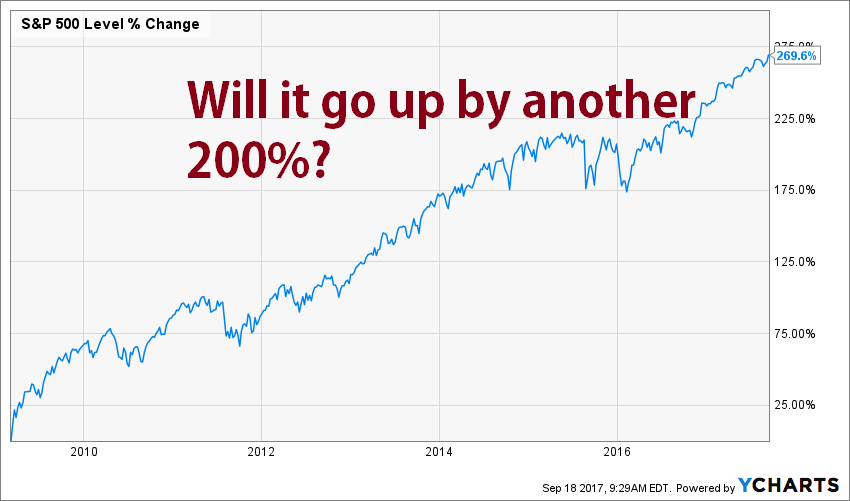

Last week, I told you I was getting ready to invest $100K in the stock market. You who told me to wait, I appreciate your concerns I know, the stock market is high, but my premise is that it will continue to rise. If you want to bring history to the table, let’s take a different look at it. Did you know that after Black Monday of October 26th 1987, the stock market humped on a bullish market for over a decade?

Source: Ycharts

All right, there was a bumpy ride in 1990, but the ride was pretty cool. For those who wanted to wait a little, there was an extra + 134% to be made if you were willing to take the drop in 1998 and wait 2 years. If you compare this bull market to the current one, we have a long ride ahead of us:

Source: Ycharts

Maybe I’m right and the stock market is only halfway through its bull market. Maybe it’s about to plunge 30% down. You know what? It doesn’t matter who is right or who is wrong. Because what matters is that dividend payments will rise anyway.

For this reason, I decided to add two more companies to my portfolio.

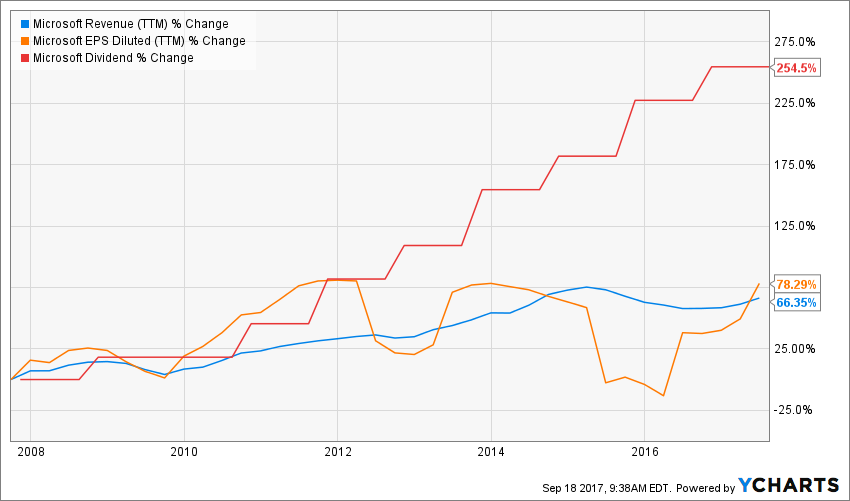

I Bought 60 shares of Microsoft (MSFT)

I must admit it, I like techno stocks. I know they are quite popular these days, but there are some obvious reasons why:

- A) They are full of cash;

- B) They started to share the wealth with investors;

- C) Their dividend growth profiles are quite impressive.

For this reason, I bought some shares of Microsoft.

Source: Ycharts

MSFT doesn’t show a perfect revenue & earnings uptrend as I like them. However, I focus on what is coming up next: the cloud is booming. MSFT is already #2 behind Amazon (AMZN) for public cloud services with Azure, which has doubled its revenues over the past 12 months. MSFT is not only strong with consumers, but also with corporate America with over 800 case studies on its website. I believe the cloud will be a source of growth for at least a decade and Microsoft is already a strong player now.

The company will benefit from stable income generated by its software suites and business services. This is still about 70% of its business model. I expect to see this part of the business to remain strong and give MSFT enough flexibility (read cash flow) to grow in other markets (mostly in the cloud services). I expect their Intelligent cloud segment to represent 40%-45% of their business in 10 years from now.

In term of dividend growth perspective, management has increased its payout by 13.48% CAGR over the past decade. After such a great ride, the payout ratio is still under control at 55% and the cash payout ratio at 38%. What is not to love?

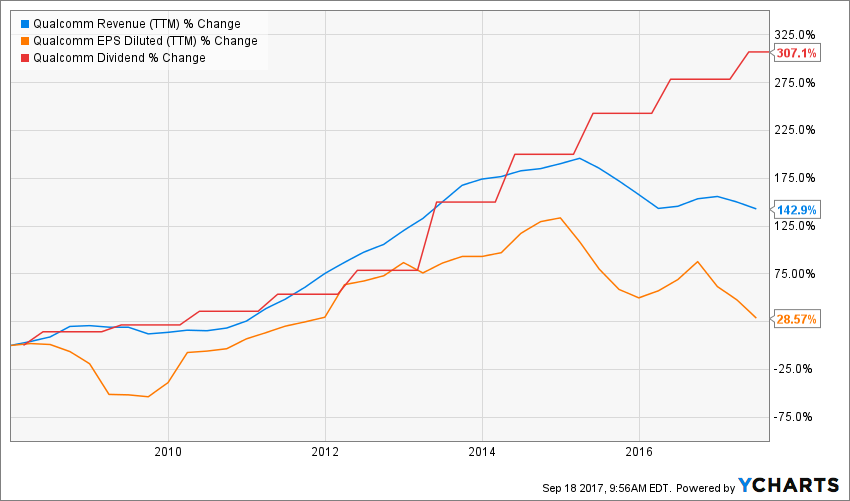

I Bought 80 shares of Qualcomm (QCOM)

With my second buy in the techno world, I’m taking a bet. I’m not the kind of investor who only purse big old dividend aristocrats (I prefer Achievers for the record). I seek a balance between a core holding (composed with companies that are “buy and sleep” holdings) and a growth segment where I can see shares jump by 30% over 12 months. I think this is the case with Qualcomm. Since the beginning of the year, QCOM shares are being hit right, left and center with bad news uppercuts. After antitrust issues with China a couple of years ago, QCOM is back in court. This time, its opponent might be even more furious as Apple (APPL) started the hostility with a lawsuit combined with a payment suspension. In an effort to diversify, QCOM issued a bid to buy NXP Semiconductors (NXPI), the biggest supplier of chips used in the automotive industry. Unfortunately for them, it seems the $47 billion bill will increase if management wants to close this deal. NXPI shareholders think they can get a better deal and this is why shares are currently trading over the QCOM offered price of $110.

Source: Ycharts

Then again, both revenues and earnings went up strongly and now have been on the downside for the past couple of years. Make no mistake, this is a risky play. However, I believe QCOM will settle its lawsuit with AAPL and will complete the purchase of NXPI. Once it moves past these events, QCOM shares might jump very high. In the meantime, the company continues to be a leader in its industry and earn solid royalties from its chips technology.

QCOM is also a solid dividend payer showing an annualized growth rate of 15% for the past decade. Considering the latest stock drop, I am now the happy share owners of a 4%+ yielder. Both payout ratio and cash payout ratios are under control at 82% and 84% respectively. This is a bit high, but considering the storm the company is going through, it still has enough room to manage their distributions. Management is confident enough that it has increased its payout by 7.5% during last summer.

More Buys to Come

I will definitely not fill my pension account with volatile companies like QCOM. My goal is to have around 20 different companies, where I will take higher risks on maybe 2 of them. I want the rest of the portfolio to be rock solid and provide me with constant dividend growth.

You like my stock ideas? I have plenty of them over here.