Last year, I claimed the Canadian market will continue its slowdown due to oil price but would finish in positive territory for 2015. I also mentioned the US market would outperform the Canadian’s. This gives me a 2 out of 3 batting average as the TSX will definitely finish in the red. At the time of writing this article (December 27th), the TSX was down roughly 9%, mainly dragged by recent events pushing the oil barrel near its lowest point in 10 years:

I don’t think there is room for panic. If you take a few minutes to calm down and think of what you read about the oil price back in 2008-2009, you will remember we were being told that the oil barrel would not hit the $100 level for a good decade. Funny enough, the barrel price went from $33 to $100 in roughly 18 months. There are lots of speculations making high variation around the oil price. The reasons to justify a low price are legions:

Production exceeding demand in general

US oil stock are increasing steadily

Iran producing more

Global economy slowing down leading to less consumption

OPEC keeping their price war by producing more

I could go on and on with more reasons, but you can read the news. On the other side, there isn’t much “news” to this. We always known about OPEC production ability, therefore, it shouldn’t be a surprise to see it in action. Same thing as oil reserve in Canada and US; they cost more to extract, but they are very important too. Therefore, we live in a world full of oil reserve at the moment and this situation will last for a while.

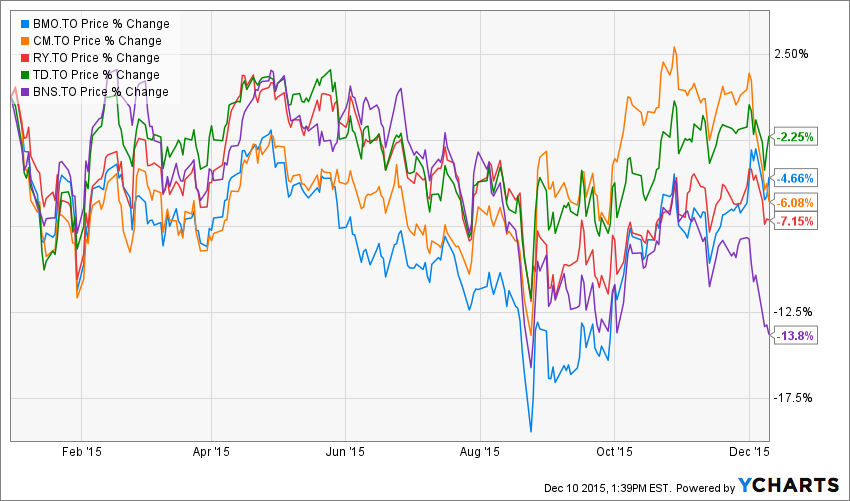

Besides resources related companies, banks were also affected by the oil price:

Banks are financing Oil exploring companies than they are also greatly dependent of the Canadian consumer health. While we are expected banks to have a rough time in 2015, they surprisingly offered decent results (and revenue growth!) for their year-end report.

Banks weren’t the only one to surprise the market as the global Canadian economy has shown some resilience. The weak dollar enabled other companies to pick-up and compensate for the slumping oil industry. Let’s not celebrate too early, but it seems the Canadian economy is stronger than expected.

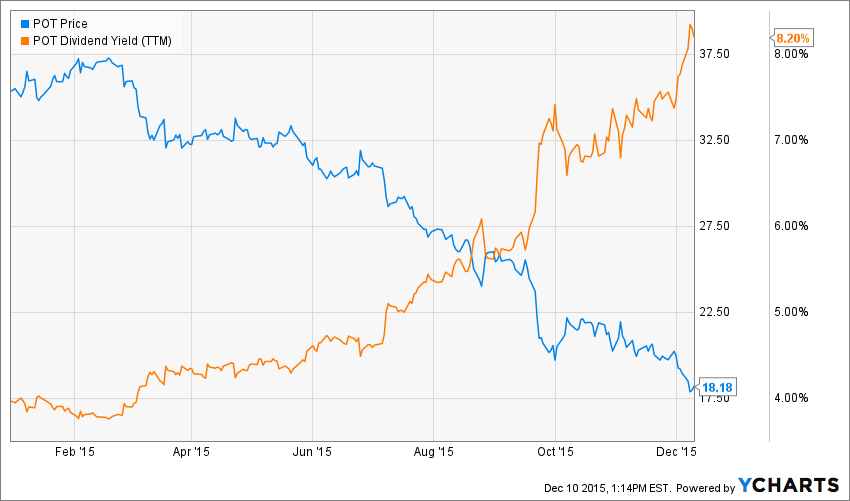

During the current downturn in the Canadian market; I believe it will be the time to pile up with good companies. One must stay away from the classic high yielding companies because they suffered an important drop. Companies like Potash (POT) for example could be interesting since it is now paying an 8% yield. However, the only reason the stock is “so generous” is because its price plummeted:

I’m not saying you should sell your POT shares if you have some, but I’m saying those “opportunities” are risky and it is not because there is a big dividend payment at the end of the month that you should automatically grab it. I rather offer you my own list of the top 3Canadian stocks to buy in 2016 while the market is not too interesting. However, you will have to be patient; I’m currently neutral for the Canadian market in 2016. But for a long term investor, this is the perfect timing to enter in a market when everybody else is looking elsewhere.

Emera (EMA.TO)

WHAT IT MAKES IT A GOOD COMPANY

Emera is an energy and service company. Emera’s main market is Nova Scotia as it owns Nova Scotia Power, the province’s main electricity provider. Emera actually owns power plants and distributes natural gas in Canada, the USA and the Caribbean. It is actively developing more energy projects in Eastern Canada.

INVESTMENT THESIS

As long as EMA is using this cash flow to generate more projects, we should see consistent sales growth. Notably, 2 projects (a participation in Maritime Link and an undersea power cable) should be under operation for 2017. The future looks bright for EMA as it shows several projects for the next decade. Both revenues and EPS are growing steady over the past five years and the dividend comes accordingly. EMA is definitely a strong utility to hold. EMA reported clockwork results on November 13th for its Q3. Earnings are up $0.04 EPS compared to last year. Management expects TECO acquisition should boost EPS by 5% in 2017 and growing to more than 10% by the third full year of operation (2019). EMA restated its dividend growth target of 8% through 2019 and expects to keep this pace past 2019. EMA continues to be a strong holding for any Canadian dividend growth investor.

POTENTIAL RISK

Considering EMA very good results in 2015, market expectation will rise in 2016. Don’t expect the company to outperform the market as it did in 2015. However, this is a strong paying dividend company that will help you smoother your return in 2016.

COMPANY METRICS

| Dividend Yield | 2.88% | P/E Ratio | 17.95 |

| 5yr Div Growth | 16.61% | ROE | 13.58% |

| Payout Ratio | 70.72% | 1yr Sales Growth | 33.26% |

| 5yr EPS Growth | 12.73% | 5yr Sales Growth | 14.91% |

COMPANY VALUATION

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 9.00% | 10.00% | 11.00% |

| 20% Premium | $83.11 | $62.23 | $49.71 |

| 10% Premium | $76.18 | $57.05 | $45.57 |

| Intrinsic Value | $69.26 | $51.86 | $41.43 |

| 10% Discount | $62.33 | $46.67 | $37.28 |

| 20% Discount | $55.40 | $41.49 | $33.14 |

Lassonde Industries (LAS.A.TO)

WHAT IT MAKES IT A GOOD COMPANY

Lassonde Industries develops, manufactures and markets fruit and vegetable juices. Their revenues comes massively from the retail market (89% of their total revenues). They own several well-known brands such as Oasis, Fruité, Fairlee, Rougemont, Allen’s, Everfresh and Del Monte. In mid-2014, it bought the US company Apple & Eve to improve their presence in the US market.

INVESTMENT THESIS

Lassonde’s wide variety of brands enables them to occupy an important space in grocery stores. There aren’t many consumer products in Canada that offer such great metrics. I know that the dividend yield is somewhat low (1%) but you have to keep in mind the company shows almost double digit dividend growth policy over the past 5 years and the payout ratio is still under 25%. Since there isn’t many “consumer defensive” stocks on the Canadian market, LAS.A should be on your watch list right now.

POTENTIAL RISK

Lassonde is battling against major brands such as Minute Maid (Coca-Cola) with larger budgets. This could result in affecting their sales over the long run as they can’t really compete fairly with them. The fact the company entered more significantly in the US market shows management isn’t afraid of competing, but this confidence could penalize them if it becomes arrogance.

COMPANY METRICS

| Dividend Yield | 1.02% | P/E Ratio | 21.07 |

| 5yr Div Growth | 10.37% | ROE | 12.65% |

| Payout Ratio | 21.32% | 1yr Sales Growth | 13.54% |

| 5yr EPS Growth | 6.97% | 5yr Sales Growth | 17.64% |

COMPANY VALUATION

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 8.00% | 9.00% | 10.00% |

| 20% Premium | #DIV/0! | $232.22 | $115.72 |

| 10% Premium | #DIV/0! | $212.87 | $106.08 |

| Intrinsic Value | #DIV/0! | $193.52 | $96.43 |

| 10% Discount | #DIV/0! | $174.17 | $86.79 |

| 20% Discount | #DIV/0! | $154.82 | $77.15 |

*The 8% discount rate doesn’t provide a valid number as forever dividend growth rate is 8% as well.

Agrium (AGU.TO)

WHAT IT MAKES IT A GOOD COMPANY

Agrium is the largest global retail and distributor of crop inputs. It is also the leader of agricultural nutrients providing farmers with all they need to improve their production. The company shows a less dependent link to potash prices as it counts on other products such as: seed, nutriments, crop protection, nitrogen and other merchandises & services. It offers a better alternative to Potash (POT) mentioned previously.

INVESTMENT THESIS

The fact that the ratio of arable land per person is continuously declining puts a constant pressure on farmers to become as efficient as possible. The first solution for farmers is to improve their production with additional fertilizer. A second solution is to protect the crops they own and make sure their land is protected from any catastrophe that would affect their production. Management expects a strong Q4 based on a longer than average fall leading to longer fertilization and crop protection application periods. The company continues its focus towards dividend increases and free cash flow expectation remains the same for the next four years.

POTENTIAL RISK

the price of fertilizer is definitely a source of revenue fluctuation in the future. As we have seen in the past, high fluctuation affects AGU’s cash flow greatly and shows a weakness in its business cycle. AGU doesn’t control the price of potash and it also subject to nitrogen price fluctuation. Unfortunately, the price of nitrogen is under strong government influence through its subsidies and state-run companies.

COMPANY METRICS

| Dividend Yield | 2.58% | P/E Ratio | 17.81 |

| 5yr Div Growth | 89.71% | ROE | 12.90% |

| Payout Ratio | 55.82% | 1yr Sales Growth | 9.37% |

| 5yr EPS Growth | 15.69% | 5yr Sales Growth | 11.29% |

COMPANY VALUATION

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 10.00% | 11.00% | 12.00% |

| 20% Premium | $217.56 | $162.68 | $129.77 |

| 10% Premium | $199.43 | $149.12 | $118.96 |

| Intrinsic Value | $181.30 | $135.56 | $108.14 |

| 10% Discount | $163.17 | $122.01 | $97.33 |

| 20% Discount | $145.04 | $108.45 | $86.51 |

Want More? I have 7 other Canadian Dividend Stock Picks in my Book!

I’ve compiled a list of 20 dividend stocks to do well in the market for 2015. You just read about four of them, but there are still lots to discover in the book! The book includes the 20 dividend stock analysis plus 10 Canadian dividend stocks. That’s 40 pages worth of information for only $4.99.

Click here to get your copy!