Each year, they would receive juicy dividends, see their payments increasing and their portfolio growing in value. Wow! This really looks like buying a seafront house in Hawaii for $200K, doesn’t it? Unfortunately, however, many 5% yielders end-up cutting their dividend.

A 5% yield is only good if it keeps getting paid

Over the past few weeks, investors got hit by dividend cuts coming from well-known businesses. As I’ve highlighted last week in this article, large caps, dividend achievers and popular dividend paying stocks have their shareholders recently:

- General Electric (GE) destroyed 92% of its dividend payment;

- Owens & Minor (OMI) went for a 71% axe swing at its dividend;

- Anheuser-Busch InBev (BUD) killed 50% of its dividend;

- And Buckeye Partners (BPL) crushed its dividend by 41%.

So much for those who thought high yielders were safe, right? At the same time, it would be a false assumption of thinking that all high yield stocks would end up with a similar fate. If you follow strict investing rules, you may find those hidden gems that keep rewarding their shareholders with generous payments. I wanted to help you out through your research by sharing my (rare) favorite stocks showing a 5%+ yield.

My favorite 5 stocks paying over 5% yield

Five years ago, I started my investing platform, Dividend Stocks Rock. I’ve built and improve this service to become one of the most efficient tools to find dividend growing companies. For several years, I was reluctant to pick high yielding stocks. However, through additional research and by applying my 7 investing rules, I was able to find a few hidden gems. As I will celebrate Dividend Stocks Rock’s 5th anniversary in December, I thought of picking 5 Stocks with a 5%+ yield. Yield posted is as of November 7th.

Blackstone (BX) 6.88% yield

Blackstone is an asset manager with $456 billion in assets under management (AUM) that comes from private equity, real estate funds, hedge funds, and credit funds. BX doesn’t invest in the stock market but developed a strong expertise in alternative assets investing in the past 30 years. BX receives money from institutional clients or wealthy families and invests it as a general partner in the mentioned asset classes.

")

Source: BX Q3 2018

Blackstone is a complex beast. BX could look like another asset manager offering a generous dividend yield to shareholders. However, it is more complicated than that. Since Blackstone keeps a cut of the profit realized on its investment, both revenues and earnings go up and down from one quarter to the other. Moreover, the strong dividend payment is also based on performance. Still, the company shows steady assets under management growth and benefits from its good reputation.

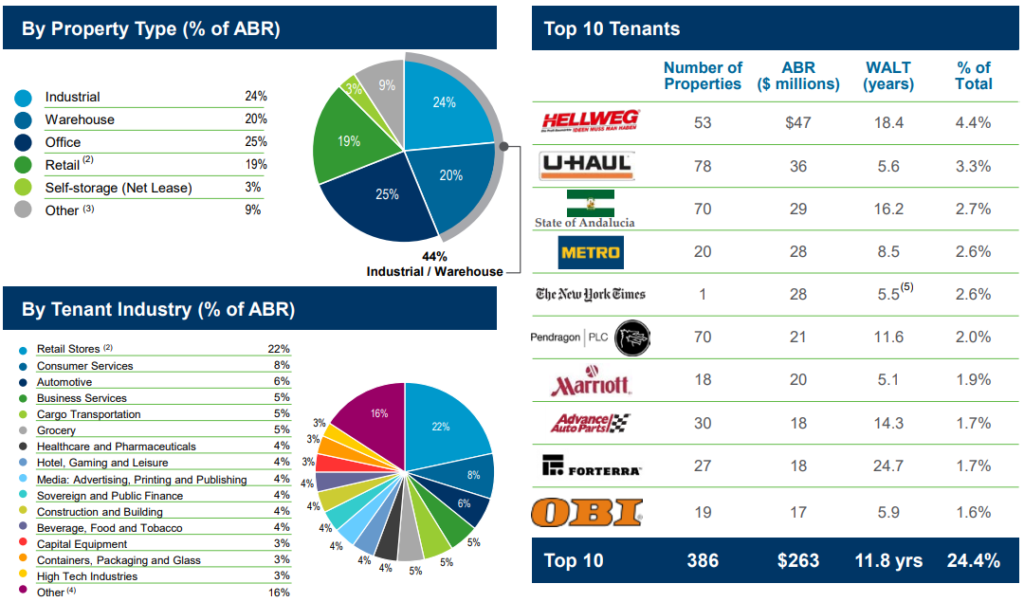

W. P. Carey (WPC) 6.25% yield

Founded in 1973, W.P. Carey is one of the largest diversified net lease REITs. WPC operates as a self-managed diversified real estate investment trust. The company owns and manages commercial real estate which is leased to companies on a long-term basis. The REIT manages 1,186 properties covering approximately 133 million square feet as of September 30, 2018 (including the merger with CPA:17). Its portfolio is located primarily in North America, Northern and Western Europe and is well-diversified by tenant, property type, geographic location and tenant industry.

Source: Q3 investors presentation

WPC is a long lasting and well managed REIT offering a great solution with a solid yield and decent dividend growth perspectives for income seeking investors. WPC shows an impressive occupancy rate (around 99%) and a top 10 tenants concentration of 32%. WPC shows a great business model with diversified sources of income. WPC counts roughly 30% of its revenue coming from Europe. Considering the recent acquisition, WP is now a serious candidate for any retirement portfolio. The dividend will continue to keep up with inflation and shows a 6% yield. Finally, WPC is part of the dividend achievers list.

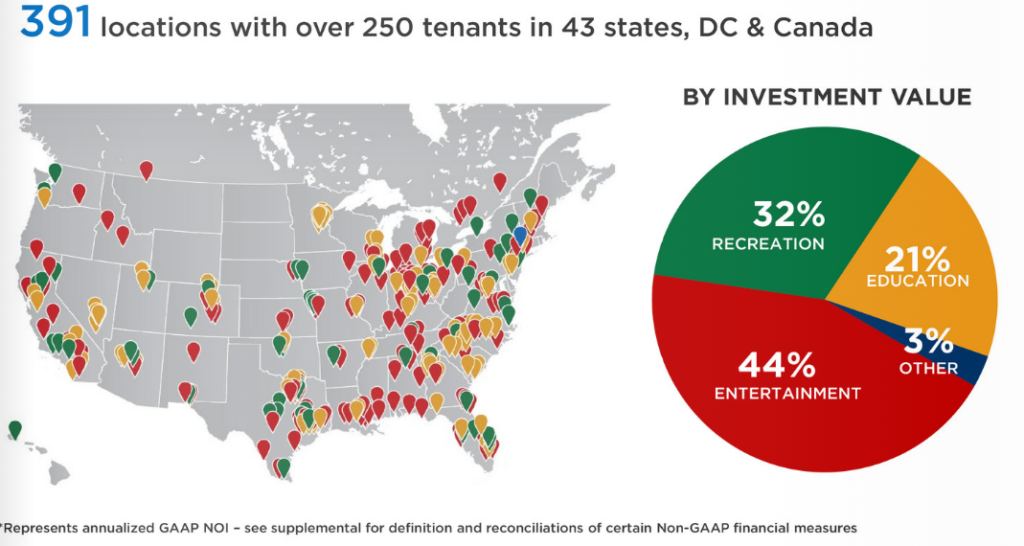

EPR Properties (EPR) 6.05% yield

EPR specializes in Triple Net Leases. This is when the tenant agrees to pay all real estate taxes, building insurance, and maintenance in addition to normal fees expected under the agreement (rent, utilities, etc.). EPR shows nearly 400 locations rented by over 250 tenants for a total asset book value of nearly $7 billion. EPR’s main business is focused on entertainment (158 megaplex theatres, 11 family entertainment centers), recreation (32 golf complexes, 12 ski areas, 21 attractions) and education (63 public schools, 14 private schools and 69 early childhood education centers).

Source: EPR investors presentation

EPR has a strong business model in a growing industry (entertainment). It will do well as the economy continues to grow. With the recent stock price drop (high of $84 back in 2016), this is a good opportunity to buy a high yielding REIT paying monthly dividends. EPR still shows an appetite for growth in the upcoming years and should benefit from the current economic tailwind well into the future. Management expects FFO/share of $5.75-$5.90 while paying $4.32 in dividend for 2018. The distribution is safe, sleep well.

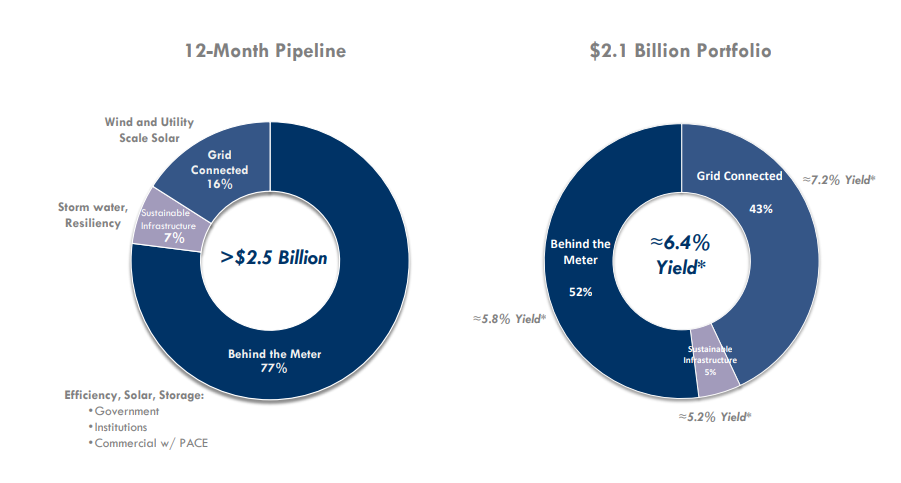

Hannon Armstrong (HASI) 5.74% yield

HASI provides capital and services focused on reducing climate changing greenhouse gas emissions (“GHG” or carbon emissions) as well as mitigating the impact of, or increasing resiliency to, climate change. It focuses primarily on energy efficiency, renewable energy, and other sustainable infrastructure markets. HASI shows about 175 investments and managed $4.8 billion worth of assets. It expects to invest around $1billion per year going forward. Its portfolio shows 47% of investment in solar, 26% in wind, 22% in efficiency and 5% in sustainable infrastructure.

Source: HASI investors presentation Nov 2018

It’s hard not to invest in a 6-7% yielder that believes in renewable energy. HASI shows confidence in its business model and is ready to invest about $1 billion each year to grow. We have clearly seen a trend towards solar and wind energy recently, and as oil prices pick up, you can expect the trend to continue to go stronger. Going forward, investors should expect a dividend policy matching inflation (2-3%). This is more than enough to beat inflation while enjoying a high yield.

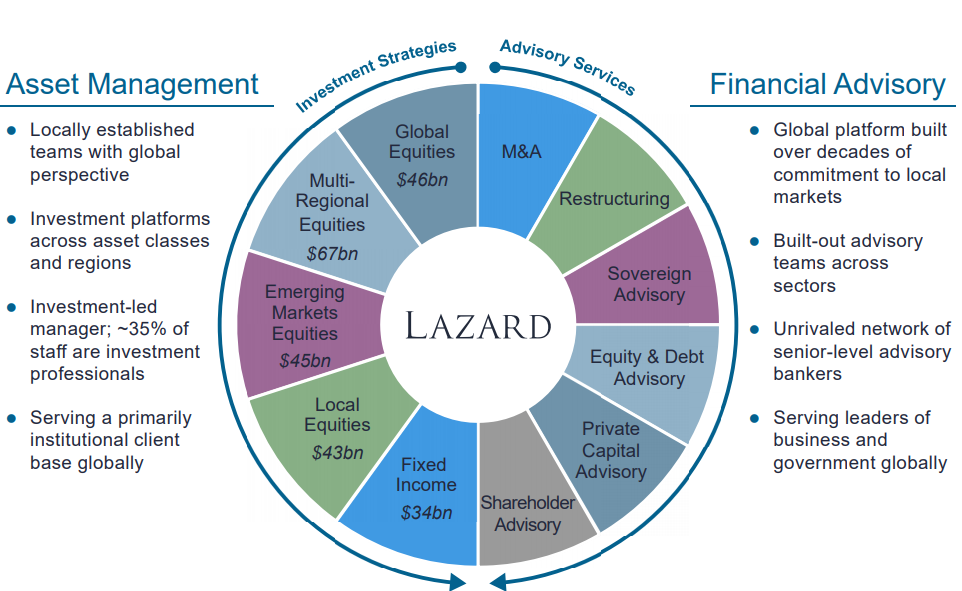

Lazard (LAZ) 4.14% yield, 7.25% with special dividend

Lazard, together with its subsidiaries, operates worldwide as a financial advisory and asset management firm. The financial advisory segment offers services regarding mergers and acquisitions, strategic advisory matters, etc. LAZ was founded in 1840 and manages over $189B. It is well known for its experience in asset management and in M&A.

Source: LAZ investors presentation

Lazard’s power resides in its quality advisory segment. LAZ is surfing on the current market tailwind in the M&A activities, while gaining market shares. LAZ has also developed a strong expertise in real asset management, which is gaining popularity among investors. Paying fees to have Lazard managing your money seems justified. Strong from its presence in 170 countries, Lazard aims to expand across the world. In late months, LAZ acquired a banking boutique in Canada in 2016 and opened a new office in Mexico in 2017. It has also built a strong brand in China for the past decade. The company has been beating down on the market recently creating a great opportunity. While the dividend yield is currently over 7%, it includes a special dividend. Management has started the tradition of rewarding shareholders in February with extra cash flow distribution for the past 4 consecutive years.

Tomorrow, I go Canadian!

Since I’m Canadian and I know lots of my readers are following this market, I’ll do the same exercise for Canadian stocks, stay tuned!

Featured Image Source: Pixabay

The post My Favorite 5 Stocks Paying a Juicy Yield Over 5% appeared first on The Dividend Guy Blog.