Investing as a Canadian comes with it’s fair share of challenges. The first is that we come with a very biased background. We are fortunate to have the Federal Government to set protectionism rules around our banks and our telecom. This situation creates perfect oligopoly where everybody makes profit. While it is not optimal for consumers, it does ensure some stability.

The problem is that once we have purchased your favorite banks, you haven’t built a full portfolio yet. Buying the big 6 banks and 3 telecoms will not make it either. While regulations are in favor of investors right now, this could change at any moment. This is why you need to diversify into other sectors.

- How can you diversify into other sectors?

- How can you make sure you will post solid returns?

- How can you avoid dividend cutters?

Those are the questions I’ll answer in this article. Let’s see how you can invest as a Canadian and make money out of this crazy market.

PSST! I have a webinar this Thursday on Canadian investment!

Everything Begins with Sector Allocation

Most investors ignore it, but most of your investing return will be explained by how you invest. In other words, your asset allocation determines everything. Once you have selected the asset allocation you want (I’m 100% equity forever, here’s why), it will explain how you do on the stock market. This is your sector allocation. Since I am in the market, I will tackle this part.

In my personal opinion, I think that anytime you exceed 20% in a sector, you are looking for trouble. Certain sectors, consumers stables, consumer cyclical, and industrial, will show a large diversification across their sub-sectors. For example, you can definitely own shares of Canadian National Railways (CNR.TO), WSP Global (WSP.TO), CAE (CAE.TO) and Waste Connections (WCN.TO), and you will be perfectly diversified. Chances are that railways won’t fluctuate the same way aircraft simulators and waste management will. There will be trends, but those companies will not react to the same events in the same matter compared to how Telus, BCE (BCE.TO) and Rogers Communications (RCI.B.TO) will.

My Favorite Canadian Sectors

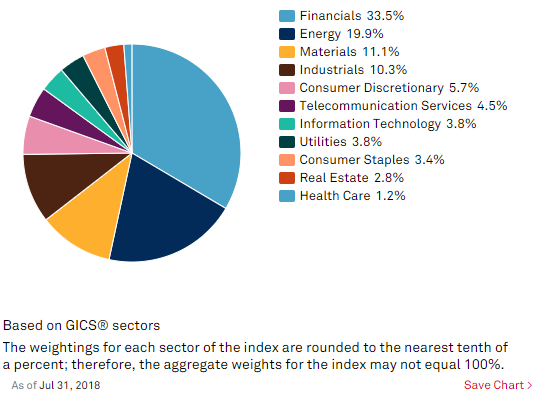

When you look at how the TSX is built; you notice that resources and financials occupy pretty much 50% of the Canadian market capitalization.

Source: Dividend Growth Investing & Retirement

We will all agree about financial and telecoms, but what about energy stocks? Should you consider them? For several years, energy stocks have been the pride and heart of the Canadian economy. The problem I have always noticed with them was their volatility. Their whole business model is based on a commodity price they cannot control. Furthermore, Canadian oilsands are among the most complex and expensive ways to produce oil.

Therefore, each time there is a slow down on the oil market, Canadians “eat dirt”. I have never been a big fan of this sector and do not believe I ever will. A similar rationale is behind the reason I am not big on the rest of the resources and basic materials. I dislike gold and wood for the same reason. Their trajectory on the market is very hard to predict and most experts are as good as meteorologists when it comes time to predict where gold or silver will finish that year. However, there are gems in many other sectors. They are yours to discover. Here are a few examples:

Consumer Cyclical

Canadians love their brands and they are willing to walk the extra mile to stick with them for the long term. This is how companies such as Canadian Tire (CTC.A.TO), Magna International (MG.TO) and Intertape Polymer (ITP.TO) could bring some growth to your portfolio.

Consumer Defensive

While Canada does not have companies that compare to Colgate Palmolive (CL) or Procter & Gamble (PG), they have a few businesses offering low dividend yield with great perspectives. Alimentation Couche-Tard (ATD.B.TO) and Andrew Peller (ADW.A.TO) are amongst my favorite.

Industrials

It is fascinating how you can find great companies when you dig a little more. Canada has the most amazing railroads operators through Canadian Pacific (CP.TO) and Canadian National Railway (CNR.TO). I also like CAE that has been built a very strong reputation in the aircraft industry.

REITs

I do not expect to touch this money for at least 30 years, so I am not actively looking to generate income. However, Canada shows a stable economy and one of the most solid banking systems. This is a great foundation for building healthy REITs in many sub-sectors. You can then find retirement, apartment, industrial REITs showing great yield, and dividend growth perspective. Among my favorite, you will find Brookfield Property (BPY.UN.TO), CT REIT (CRT.UN.TO) and Granite REIT (GRT.UN.TO).

Utilities

Similar to the REIT sector, utilities are also strong companies evolving in the Canadian landscape. Many of them have built a strong core business in Canada and then grew through acquisitions in the U.S. Companies like Fortis (FTS.TO) and Emera (EMA.TO) shows more US revenues than Canadian now.

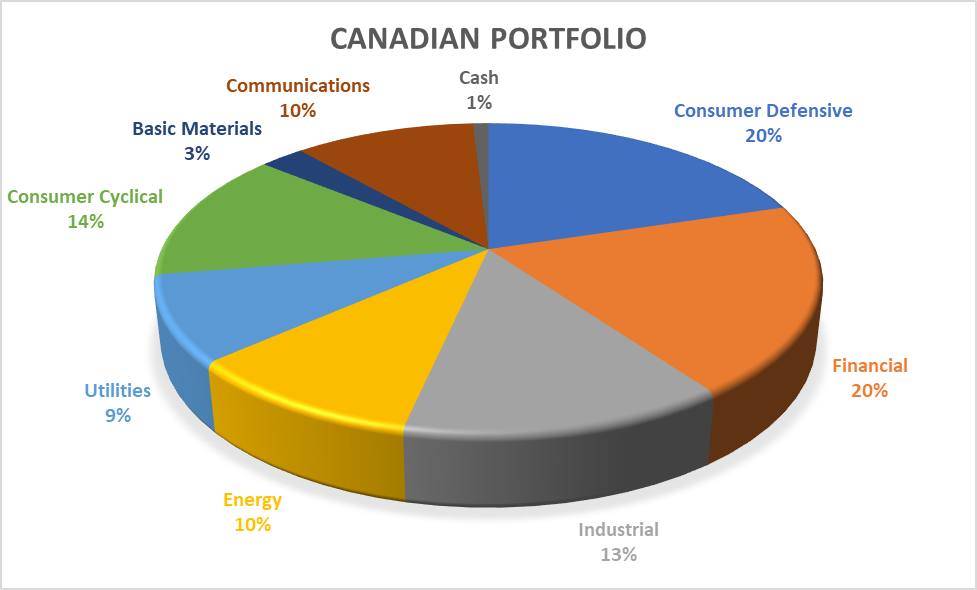

My Sector Allocation

For the sake of this exercise, I will use my pension plan account combined with my RRSP. They were built at different times, but they have the same goal; offer a maximum total return over the next 30 years. Here is what my total Canadian portfolio looks like as of February 20th 2018.

| Company | Ticker | Sector | Value |

| Alimentation Couche-Tard | ATD.B.TO | Consumer Defensive | $6,285.74 |

| Andrew Peller | ADW.A.TO | Consumer Defensive | $5,419.90 |

| National Bank | NA.TO | Financial | $7,543.14 |

| Royal Bank | RY.TO | Financial | $6,107.40 |

| CAE | CAE.TO | Industrial | $5,532.00 |

| Enbridge | ENB.TO | Energy | $7,710.29 |

| Fortis | FTS.TO | Utilities | $4,589.64 |

| Intertape Polymer | ITP.TO | Consumer Cyclical | $5,648.99 |

| Lassonde Industries | LAS.A.TO | Consumer Defensive | $3,843.42 |

| Magna International | MG.TO | Consumer Cyclical | $4,791.50 |

| Canadian National Railway | CNR.TO | Industrial | $4,706.09 |

| Gluskin Sheff | GS.TO | Financial | $1,578.24 |

| Nutrien | NTR.TO | Basic Materials | $1,973.71 |

| Polaris Infrastructure | PIF.TO | Utilities | $2,248.35 |

| Telus | T.TO | Communications | $8,109.80 |

| Cash | Cash | $691.09 | |

| Total | $76,779.30 |

Here is my Sector Allocation:

While this portfolio does not resemble the TSX at all, it is still very well diversified across 8 different sectors, with none exceeding 20%. However, I still have US holdings.

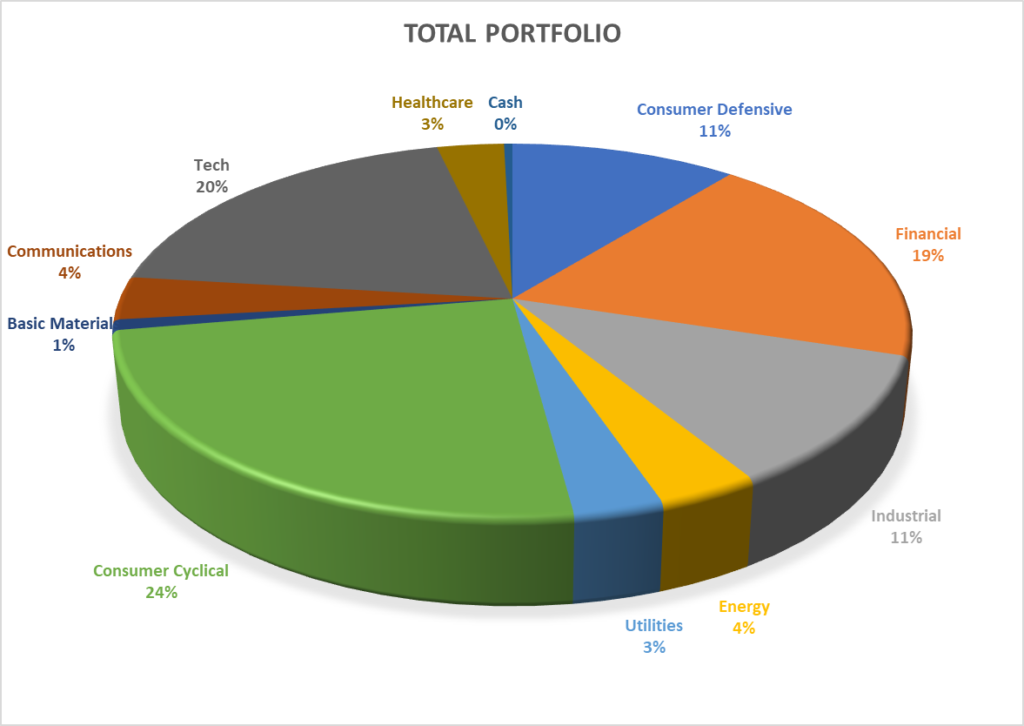

Here is the second part you have been missing:

| Company | Ticker | Sector | Value |

| Apple | AAPL | Tech | $20,275.71 |

| BlackRock | BLK | Financial | $7,954.06 |

| Disney | DIS | Consumer Cyclical | $15,110.22 |

| Garrett Motion | GTX | Industrial | $64.45 |

| Gentex | GNTX | Consumer Cyclical | $6,346.35 |

| Hasbro | HAS | Consumer Cyclical | $5,302.49 |

| Lazard | LAZ | Financial | $4,972.79 |

| Microsoft | MSFT | Tech | $8,554.08 |

| Resideo Tech | REZI | Industrial | $169.23 |

| Starbucks | SBUX | Consumer Cyclical | $7,864.51 |

| Texas Instruments | TXN | Tech | $7,069.75 |

| United Parcel Services | UPS | Industrial | $5,401.81 |

| Visa | V | Financial | $9,518.60 |

| Amazon | AMZN | Tech | $6,435.45 |

| Bank OZK | OZK | Financial | $3,675.63 |

| Coca-Cola | KO | Consumer Defensive | $8,035.68 |

| Johnson & Johnson | JNJ | Healthcare | $6,974.73 |

| Lockheed Martin | LMT | Industrial | $8,848.99 |

| Lowe’s | LOW | Consumer Cyclical | $7,982.73 |

| Cash | $182.23 | ||

| Total | $140,739.48 |

*Amounts of my US holdings are in CAD using my broker’s conversion rate of the day at 1.318.

And now the complete Sector Allocation:

As a whole, my portfolio shows 2 more sectors (we are currently at 10) including a larger proportion to “growth sectors”, such as Tech and Consumer Cyclical. This is thanks to the U.S. Market. Due to the currency factor, many investors will not bother. They see their Loonies being crushed by the Greenback and they fear of losing more money upon the conversion. Let’s take a look at this point.

Why the Currency Factor Does Not Matter in the Long Term

Why in the world would I waste 30% of my hard-earned money to invest in the US market?

This is often the question I get from Canadian investors whey they consider investing in another currency. After all, our weak dollar does not help us to buy shares of American companies. Many think the 25%-30% currency impact will affect their portfolio over the long run.

Canadians prefer to invest 100K in Canadian stocks, than 70K in US ones. But besides a ~2% conversion fee (which can easily be avoided through an ETF strategy), I don’t see what prevent Canadians from getting stocks coming from the other side of the border.

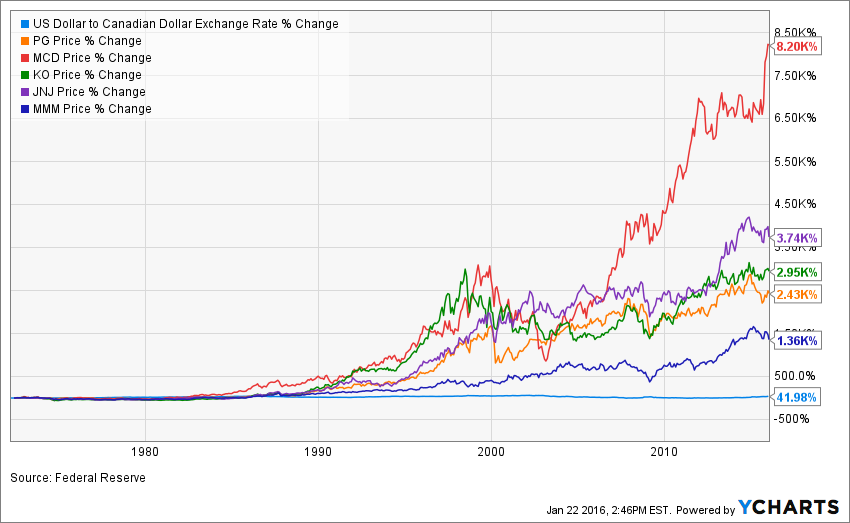

44 Years History Shows There is No Impact

Back in 2016, I wrote about the currency factor on this blog. I went back as far as Ycharts would let me to see how the CAD vs USD factor would influence my investment. I went back in 1972 and watched what happened back then. Here’s the chart I got back in 2016:

Source: Ycharts

As you can see, the greenback gained 42% in value compared to the loonie. This is probably the worst-case scenario. Even then, we are talking about 42% total change in 44 years. Therefore, it’s not even a difference of 1% annualized return. Look at how classic dividend payers you can only find on the US market performed during those 44 years.

We obviously cannot predict the future. Keep in mind that both US and Canadian economies are relatively stable (meaning a total collapse of one economy vs the other is unlikely) and our both countries enjoy political stability (then again, we are not going to get a coup anytime soon). Therefore, the odds that one currency jump by 500% in the next 20-30 years is very unlikely. And if this ever happens, trust me, you will have a lot of more important problems than what is happening with your portfolio.

What the U.S. Market offers you Vs the Canadian Market

If you look at how I invested my money, you will note I found companies on the U.S. market that has unmatched comparable on Canadian soil. The tech sector, especially for dividend investor, is nearly non-existent for Canadians. However, you can find dozens of high-quality dividend tech stocks (here’s the complete list) on the US market.

Companies among consumer cyclicals are legions on the U.S market too. Can you name one Canadian company showing similar growth vectors such as Disney’s (DIS) or Starbucks’ (SBUX)? A similar question could apply to almost all sectors. I just saw more opportunities in the consumer cyclical sector according to my 7 investing principles.

In other words, the US market offer you a unique access to companies doing businesses across the world. Instead of searching for the next emerging market boom, just invest in companies exploring those markets for you. They have an advantage others don’t; they benefit from a strong core business model from the US (generating lots of cash flow) and use their expertise to grow offshore. This can’t get any better.

Downsides of investing in US stocks as Canadians

Unfortunately, there are some downsides to buy US stocks if you are Canadians. While the currency factor isn’t a real one over the long haul, rapid FX changes could hurt your short-term investment return. While it was a very smart idea to invest massively in US currency between 2012 and 2013 (the CAD was once worth more than the USD!), my investing return got hurt a few years later as the CAD bounced back after 2016. If was following my short-term returns, I would be greatly worried to see m portfolio dropping by 7-8% solely based on currency fluctuation. Fortunately, I invest for the next 30+ years and I don’t really mind what is currently happening.

The second downside of investing in foreign countries is obviously taxes. If you invest outside a retirement account (TFSA, RESP or non-registered account), you will have to pay taxes on your dividend. Rules vary from one account to another and I’m not a tax expert. Just keep for granted you will not keep the dividend payment to yourself, you will have to share a part of it with the US Government. Then again, think about it. Imagine I invested $8K in BlackRock in a cash account. I’ll receive about $240 per year in dividend. I’ll have to pay 15% taxes to the Uncle Sam. Therefore, I will have $204 left in my pocket for an effective yield of 2.55% instead of 3%. This is not exactly a catastrophe either.

Final Thoughts

When I look solely at my portion of Canadian stocks in my portfolio; I can say I can build a solid dividend growth portfolio with only Canadian stocks. At DSR, we even managed to build a solid retirement portfolio (4.5%+ yield) with Canadian companies only.

However, when I add US stocks to my portfolio, I optimize my diversification and increase my growth perspectives for both capital appreciation and dividend growth. If I had to invest more money in a TFSA or a cash account, I would likely optimize my portfolio by selecting Canadian stocks only. Then, I would sell my Canadian holdings in my RRSP and pension account to replace them with US stocks. I would then show the same sector allocation when I combine all my account together, but I would not be paying taxes to Uncle Sam for nothing!

Want more? Here’s Webinar for Canadian Investors

As a Canadian investor, I’m sure you have tons of questions. More than often, it’s hard to find answers as Canadian investing resources are limited.

- Will you keep-up with energy stocks, banks and telecoms?

- Are you going to buy U.S. stocks with such a weak Canadian dollar?

- Are we going to get crushed by a housing bubble?

To shed some light on those questions (and more), I’m hosting a free webinar this Thursday.

Register here (it’s free and you’ll get the replay a few a hours after we are done) (email required)

Topic: Investing the Canadian Way – How to Build a Safe Portfolio in 2019

Date: Thursday, February 21st at 1pm EST

Description:

- In this webinar, I’ll discuss my strategy to find safe Canadian dividend growth stocks in this crazy market and we will look at sector allocation (get rid of energy?), currency factor (investing in US stocks?) and I’ll share a few of my favorite picks.

- You must register with Webinar Ninja to attend (if you did it in the past, no new registration is required). This is completely free and the webinar is free also. Webinar Ninja is the platform we use to run all our webinars. It works well and provides an optimal experience for everybody.

- The presentation is about 35 minutes.

- There will be a Q&A session of about 25-30 minutes.

- The webinar works on Google Chrome or Safari from a laptop or computer. (It is not compatible with smartphones or tablets.)

- If you can’t make it on time, there will be a full replay available, but you must register to access it.

Register here (free) (email required)

The post Investing the Canadian Way – Tricks I use to Boost My Returns appeared first on The Dividend Guy Blog.