“It would be wonderful if we could avoid the common setbacks with timely exits.”

– Peter Lynch

Source: Ycharts

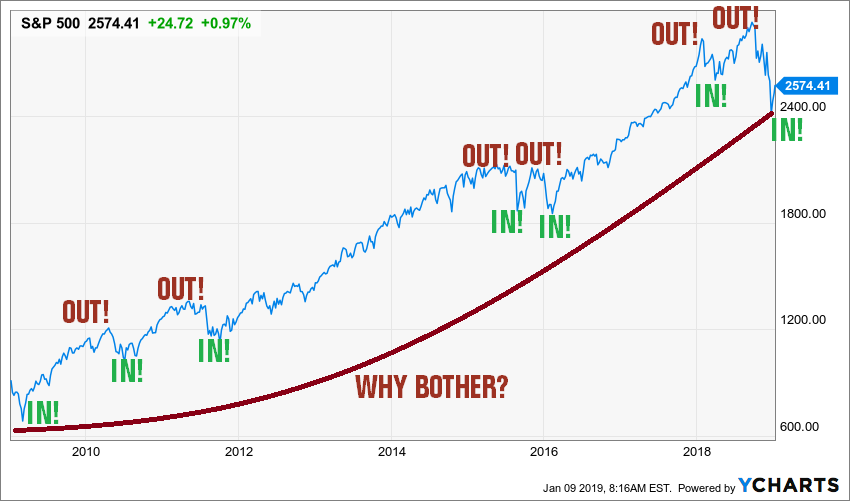

In a perfect world, we would be genius investors that always get out on time and invest all their monies right before the market jumps back up. While this last sentence may seem a pure heresy for many of you, many claim and believe there are ways to know the unknown.

Recently, I’ve read many articles from those bear lovers jubilating back in October-November 2018 as the market was finally dropping. The announcements and discussions about the “current” bear market were legions. According to the most commonly used definition for a bear market, it must go down by 20% to be confirmed. Depending on which metrics you use to track the bear, you may or may not have seen it. After all, the S&P 500 hit -19.8% at its lowest point:

Source: Ycharts

What about the next day? On December 26th, the market bounced back and the S&P 500 is now up by almost double-digit (+9.5%) before the market opens on January 9th ,2019.

So where does this leave us? In a perfect world of confusion and uncertainties.

Is this a market comeback?

Is this a pause for a larger drop in the next weeks?

Who finished the orange juice and left the empty pint in the fridge?

I tend to have a simple and rational way of looking at the market. Whatever will happen in 2019 will happen- no matter what I think, no matter how I invest. There is no point in guessing that. How should I invest my money in 2019? The exact same way I did in 2018, 2017, 2016…2010. This article includes my guidelines to build a safe dividend portfolio in 2019… and beyond.

Keep it Simple… Really?

My investing strategy evolves around a few simple but highly effective principles:

- Don’t lose money (more than you should)

- Know why you buy (so you’ll know why you sell)

- Follow a few key metrics (sophisticated approaches sound cool, nothing more)

- Trends are more powerful than numbers (numbers are words, trends are stories)

- Offense is the best Defense (in everything I do in my life)

Don’t Lose Money

Source: Ycharts

I know this principle seems obvious. The whole idea of investing is about making money, not losing some. However, avoiding companies that could kill your portfolio by a major drop isn’t that easy. The above-mentioned graph shows 7 companies that cut their dividend in 2018. At DSR, we had 5 of them rated as “sell” or “strong sell” at the beginning of 2018.

Dividend cutters often see their stock price drop in a similar manner. When a company cuts its payout, it basically fails its shareholders and breaks the bond of confidence with the market. While there are no crystal balls telling you which companies will fail you in your portfolio, there are some basic rules that can help you in identifying them.

My investing platform, Dividend Stocks Rock, recently celebrated 5 years of existence. I’m proud that none of our holdings have suffered a dividend cut in 5 years and only a handful of them missed increasing their payouts each year. In October 2018, we hosted a free webinar explaining our methodology in avoiding dividend cuts (you can watch the replay for free here).

We make sure each company we keep in our portfolios shows the following characteristics:

- #1 They are dividend growers

- #2 They show growth vectors

- #3 They show reasonable payout ratio (cash payout ratio or AFFO payout ratio)

- #4 They don’t pay a high yield (or we get very cautious)

If you want to learn more about those characteristics and how I look at them, you can read my quick guide to avoiding dividend cuts.

Know Why You Buy

After making sure that none of my companies may cut their dividend, I move to the second principle: know why you buy. I regularly review each of my holdings to make sure my investment thesis still works. Before I purchase any stocks, I make sure to write down my investment thesis and highlight precisely why I think this company will do well in the future.

Since I know very well I can be wrong (remember; nobody has a crystal ball), I review my positions quarterly and make sure my investment thesis stands. If I know why I buy a stock, I’ll know when to sell. That moment happens when my investment thesis doesn’t work out (or never did) anymore.

Key Metrics

More technical investors will appreciate if I dive into more concrete and raw data to analyze stocks. After all, guessing which company will cut their dividend or knowing how a company business model will thrive in the future is soft guidance for investors.

This is why I also have my set of metrics I follow as a starting point. Those metrics will help me in getting rid of many stocks before I spend my precious time in analyzing a business model inside out. Since it’s impossible to cover 5,000+ stocks, you need some help to reduce this list.

I use Ycharts as a stock screener and use a few metrics to start my research:

- Dividend Yield over 2% and under 6%

- 5 Year Revenue Growth positive

- 5 Year EPS Growth positive

- 5 Year Dividend Growth positive

- Payout Ratio over 0% and under 85%

- Cash Payout Ratio over 0% and under 85%

It’s important to understand that this is not the only metric I follow and that even those metrics are not set in stone. For example, I own shares of many dividend paying stocks showing a yield under 2%. Many of those holdings are performing very well (just think of Visa (V) or Disney (DIS) for example).

Unfortunately, no matter how many metrics and how you play with them, some events remain out of control. One must remember that metrics tell you a story that already happened. The future yet remains to be written. Companies that looked nice on paper could eventually burst in your face.

Real Life Example

Altagas (ALA.TO) is a good example. Altagas is a natural gas company. It operates 3 business segments. The Gas division includes natural gas gathering and processing, natural gas liquids extraction and separation, transmission, storage, and natural gas marketing, as well as AltaGas’ indirectly held one-third interest in Petrogas Energy Corp. The Power division includes generation assets located across North America with more than 1,688 MW of gross capacity, all from natural gas and renewable sources. Finally, the Utilities division serves about 575,000 customers with natural gas. In 2017, Alta acquired WGL holdings for $8.4 billion for economies of scale and additional growth opportunities.

With 50% of its business in Canada and the other 50% in the U.S., ALA shows a well-diversified business. ALA has shown expertise in growing its assets from $3 billion of value in 2010 to $10 billion in 2018. ALA achieved this growth through a mix of new projects and acquisitions.

As you can see, everything looked good on paper. The company showed relatively good metrics, but something didn’t add-up. When we first analyzed ALA at the beginning of 2018, we couldn’t determine why the yield was so high and stock went sideways for a couple of years (2016-2017). We ended our report by the following line: “This sounds like a “run if you don’t get it”. This is why ALA is not in DSR portfolios”. Then, in late 2018, management explained that the company needed more cash flow following their major acquisition (WGL). This is when everything went wrong:

Source: Ycharts.

I can say that we were somewhat lucky to not have fallen for this great company with a great yield. My number one rule always applies above everything else: invest in what you understand.

Trends are Often More Powerful than Numbers

The previous metrics will give me about 400 companies to search. I usually know more than half of them by name or because I’ve investigated them in previous years. Then, I could use many other metrics to refine my work.

Unfortunately, metrics are just numbers like words on a page. You need to read the whole book to fully understand what is happening. Some metrics could seem high or low for a specific company or a specific sector. It’s important to compare metrics with other peers in the same industry.

I like to look at long-term debt level, margins and cash flow from operations. However, I usually prefer to look at them in term of trends instead of numbers. Trends are telling a more complete story to understand. Is a gross margin of 35% good or not? This could be the industry standard or it could be a lot better. What really matters to me is to know what the margin was 1, 2, 5 years ago. If the gross margin is continuously decreasing, there is a story I need to discover. Reading financial statements should tell me more about what is happening.

This is often when the “monk’s work” start. I like looking at 5 year trends to identify potential stories. When there is a bump or a drop form one year to another; there is a story to understand. This is how I identify most companies with an Achille’s Heel and don’t buy them.

Offense is the Best Defense

Speaking of trends and their stories, my three favorites are all about growth: revenue, earnings and dividend.

First, a company with a strong business model will find ways to grow their revenue. It could be through organic growth or with a major acquisition. When you look at a 5-year trend, you can easily determine if the growth is coming from a one-time event (e.g. an acquisition) or if it’s in the company’s DNA.

Second, when revenue grows, chances are earnings will follow. Now I must warn you; EPS is far from being a perfect number. The fact that EPS is calculated using GAAP makes it imperfect. In 2018, many companies had to declare provision for taxes or enjoyed a strong EPS jump. This was all related to the Tax Bill. This situation caused lots of EPS ups and downs that has nothing to do with the business model. By looking at a 5-year trend, you get a better picture of what the company is really doing.

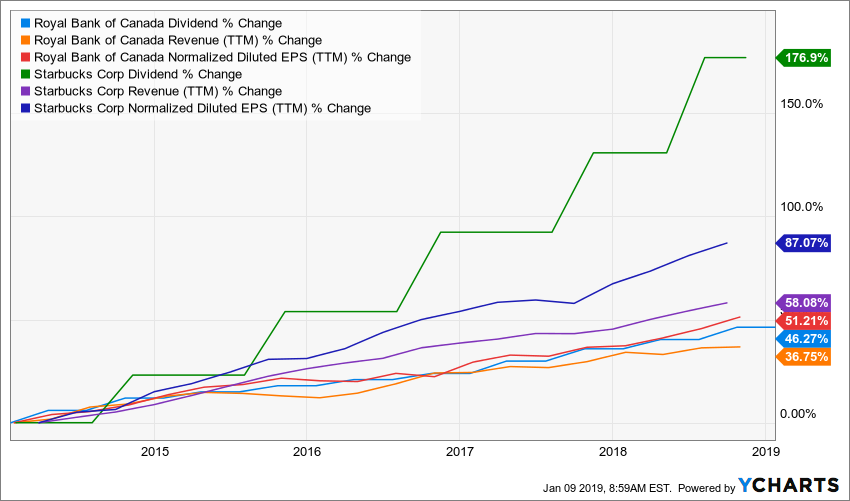

Third, if revenue and earnings are going up, chances are the dividend will follow. Dividend growth is my favorite metric to follow by far. When management decides to grow its payout year after year, it’s only because it knows it can afford it. This shows confidence in their business model, confidence in their future and revenue and earnings growth potential over the long haul. Companies like Royal Bank (RY.TO) and Starbucks (SBUX) are great example of a perfect dividend triangle:

Source: Ycharts

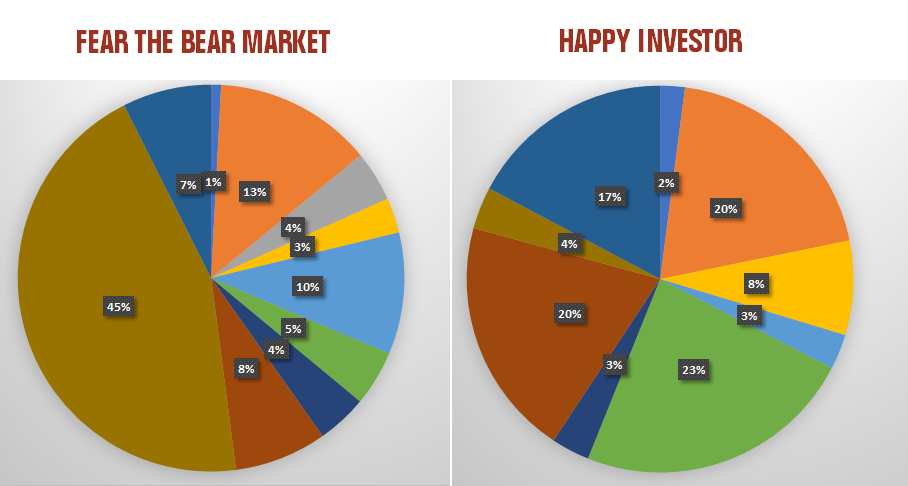

Sector Allocation… That Good Old Friend!

Another obvious advice that is often not followed by investors is to build a great sector allocation. As I mentioned; everybody looks good on Prom night. If you were looking at tech stocks (especially semiconductors) a year ago, you would have probably bought them all. They were all showing steady growth in all aspect of their business. Then, toward the end of 2018, revised guidance started to appear and 2019 should not post similar growth trend.

This is why I try to keep the weight of any sector in my portfolio under 20%-25%. From time to time, I might hit 30%, but those are moments where my portfolio is at greater risk. Investors who concentrate most of their holdings in a single sector will either have a really good year or a terrible one.

Showing a balance across various sectors is often boring. When a sector picks up, you have no more than 20-25% of your portfolio surfing the wave. You are then a spectator watching other investors talking big about their clairvoyance. However, you are also a spectator when a sector is burnt to ashes and you don’t have a large exposure.

Final Thoughts on Metrics and a Safe Investment

I had a hard time writing this article. In fact, it took me all morning to get my head around it. I wish there was a more mathematical way to identify great stocks. I looked back at many previous articles, at my notes and work at DSR. I wish I could give you a list of “10 ultimate metrics” where you can roll out a search and pick any stock from this list. Unfortunately, there isn’t.

This is especially true when in a market like this one. Since we have been running on a long economic growth streak, it seems that many companies show great numbers. Everybody looks good on their Prom night. It’s not always the case the next morning. This is where the “soft” or qualitative analysis comes in handy.

This Thursday, I will host a free webinar about building a safe portfolio and I will share my methodology to avoid major pitfalls. We all know how painful it is to see one of our holdings going down 40%. There are ways you can avoid making those mistakes (most of the time!). If you read this post late, you can still use the link to watch the free replay.

Click here to register to the Webinar

You can still register even if you’re late and get access to the free replay instantly!

Topic: Investing in 2019 and Beyond ; How to Build a Safe Dividend Portfolio?

Date: Thursday, January 10th at 1pm EST

Description:

- In this webinar, I will discuss the stock market in general and will offer you my perspectives for 2019. We will discuss which sectors to invest in and which ones to avoid. I will also tell you about the investing methodology I used to avoid major pitfalls in 2018.

- You must register with Webinar Ninja to attend (if you did it in the past, no new registration is required). This is completely free and the webinar is free also. Webinar Ninja is the platform we use to run all our webinars. It works well and provides an optimal experience for everybody.

- The presentation is about 30-35 minutes.

- There will be a Q&A session of about 25-30 minutes.

- The webinar works on Google Chrome or Safari from a laptop or computer. (It is not compatible with smartphones or tablets.)

- If you can’t make it on time, there will be a full replay available, but you must register to access it.

Register here (free)

The post Investing in 2019 and Beyond; How to Build a Safe Dividend Portfolio appeared first on The Dividend Guy Blog.