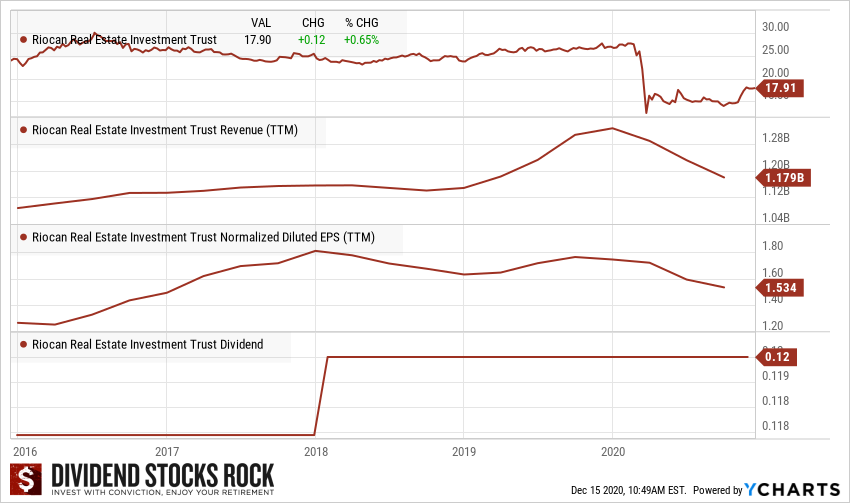

At the beginning of December, RioCan (REI.UN.TO) dropped a bomb for retirees: They slashed their dividend by 33%.

“As RioCan continues to navigate through the uncertain retail landscape created by the COVID-19 pandemic and faces an unknown length and breadth of closures, the Board has taken the prudent action of reducing our distribution. A more conservative payout ratio is important in this undeniably challenging environment despite our well positioned portfolio, solid base of tenants and deep liquidity,” said Edward Sonshine, Chief Executive Officer of RioCan. “At the same time, we believe the current circumstances present an opportunity for us to optimize our capital allocation towards accretive initiatives as we remain committed to driving value creation for our unitholders and increasing distributions from this new base as conditions permit.”

Source: RioCan Press Release

A lot of retirees have been devastated by that news. While I understand their pain and feel for them, I’m not so surprised. I didn’t like RioCan that much for many years. So here’s why it’s not part of my favorite REITs.

Business Model

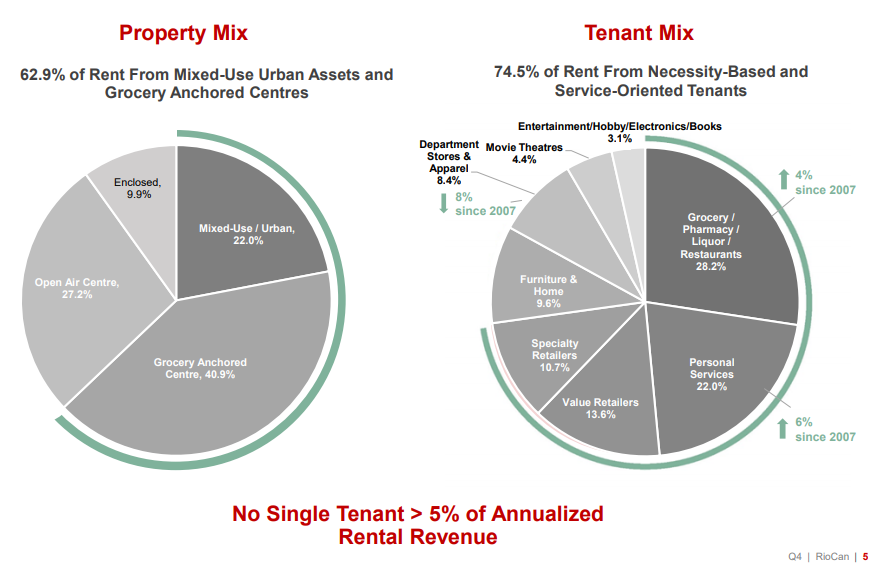

RioCan Real Estate Investment Trust is a Canadian real estate investment trust which owns, develops, and operates Canada’s portfolio of retail-focused (90%), increasingly mixed-use properties. The REIT’s property portfolio includes shopping centers and mixed-use developments, with most of its properties located in Ontario, Canada. RioCan’s tenants consist of grocery stores, supermarkets, restaurants, cinemas, pharmacies, and corporations. Geographically, the company operates in Canada, which generates the majority of its total revenue, and in the United States.

Investment Thesis

In July, the investment thesis DSR members could read was as follows:

“The REIT is showing an impressive occupancy rate of year after year. Over the past couple of years, REI sold non-core assets to concentrate on what they know best. We like management’s new focus and we think it will help build additional values for investors in the future. Unfortunately, the REIT must face constant headwinds coming from the retail brick & mortar industry. The situation has been aggravated by the Coronavirus where REI collected only 66% of its rent in April. Since then, shopping malls re-opened, but we expect many bankruptcies among retailers toward the end of 2020 and the beginning of 2021. The dividend will not be increase in the upcoming years, and even a cut is possible.”

I wrote this investment thesis back in July while many financial analysts were calling the dividend safe. They claimed the REIT had ample liquidity and showing a decent AFFO payout ratio. They were right about the fact RioCan could afford the dividend. However, it’s not because you can afford a brand new Tesla that you should have one in your driveway.

To prevent dividend cuts, I have set Three Red Flags rules:

- Listen to the Market: when the market doesn’t like a stock anymore, you need to do your homework and to try to find out why. A high yield is an invitation for investigation.

- Look for an Absence of Dividend Growth: this is the first step to a dividend cut. You must dig deeper.

- Look at the Dividend Triangle: If EPS growth, Revenue growth and Dividend growth are lagging or go down, the dividend will hardly be sustainable.

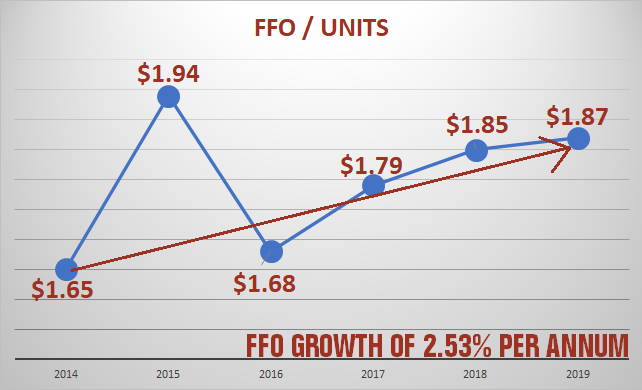

RioCan FFO/unit growth has been modest since 2014, limiting the REIT ability to increase the dividend more consistently.

A FFO/unit growth of 2.54% per annum since 2014 didn’t offer much flexibility to increase the REIT’s dividend. Therefore, shareholders only receive on paycheck increase between 2013 and early 2020. The absence of dividend growth combined with weak FFO/unit increase over the past 6 years were signs that something wasn’t right. No investor can read the future and I could have been wrong, but these three rules often lead to dividend cuts. I just thought there were better and safer options for investors.

I’ve explained my three rules and the overall context around REI more in details in the following video.

Potential Risks

The retail brick & mortar business isn’t exactly skyrocketing now. The fear of seeing other stores like Target and Sears closing is omnipresent. RioCan will be affected by such events. Considering the severe recession we will be in, expect more bankruptcies coming in the upcoming quarters. Many shopping malls have re-opened, but customers are still shy in their spending habits. The fear of future lockdowns creates lots of uncertainties. Rent collection is not so bad so far, but there will be more retailers struggling in 2021 as payment deferral and Government help created a distortion between collection rate and the real financial situation of many tenants.

Since REI is well-diversified, management will surely find a way to manage through these troubled waters. Nonetheless, we don’t see it thriving in the coming years. RioCan is multiplying investments in apartment buildings to improve diversification and offset the bearish trend around many retailers. Will it be enough? Only time will tell.

Final Thoughts

Remember that around 90% of its business is in the retail sector. Therefore, RioCan remains risky in the current economy. Don’t expect a dividend increase anytime soon. The company will need its money to fund their projects and continue the shift towards more mixed-use properties.

What’s left of the dividend should be safe though. If you decide to buy it, consider REI as a speculative play; avoid putting more than 5% of your portfolio into it.

The post I Didn’t Like RioCan (REI.UN.TO) Before It Cut Its Dividend; What About Now? appeared first on The Dividend Guy Blog.