Retiring is like learning how to skate. We all know how to stand and how to walk. Yet, once we put skates on, there is a whole new world of movements (and muscles!) that must work together to make sure you keep standing and, hopefully, moving forward.

You’ve spent your entire life working, saving, investing and now you must learn how to skate. Suddenly, there is no money coming in, but there will surely be money going out.

This article won’t touch the tax aspect as each situation is different and various rules and tax rates may apply. However, there are common situations we will all face upon retirement. Once your retirement strategy is outlined, you will be in a good position to meet with a tax expert to do some “tax tweaking”. Don’t do it the other way around.

This is a guide, not a book of law. This means that I will discuss how I will personally approach retirement with my portfolio and how my strategy makes sense for me. Maybe it’s not applicable to your situation, or maybe you will only see half of it as being relevant to you. There are obviously many ways to retire happy. This is one way I know will work for me and very possibly for you as well.

Let’s start with the basics: you retire, and you must create your own paycheck now.

How Does it Translate in Your Portfolio?

Imagine I need $30,000 per year once I have deducted the income I will generate from my pension or other sources of income from my total expenses. In an ideal world, I’d like to have at least that amount in cash in my portfolio if not double that amount. By keeping between $30,000 and $60,000 in cash, I know I have up to two years’ worth of my financial needs readily accessible without having to liquidate any long-term investments. Once I retire, my priority is to enjoy life, and to do that, I must sleep well at night.

Keeping such a level of cash will allow me to make the best investment decisions no matter what happens on the stock market. If I run into another March 2020 where my portfolio melts down by 30% overnight, I know that I don’t have to do anything as I can withdraw cash from my own “ATM” at the end of the month. I can take the time to deal with the crash later as it won’t affect my retirement for at least 2 years.

To build that amount of cash, we can do it through two simple methods:

#1 I stop reinvesting my dividends a few years before I retire and let the cash build in my account. It’s a simple way to put it on autopilot. On the other hand, I may need a few years to build such an amount and this means that the cash will not generate any meaningful returns during that time.

#2 I wait for day 1 of retirement to sell the equivalent of one to two years’ worth of my financial need. It enables my portfolio to work full speed until the very last minute. On the other hand, if I retired at the bottom of the market on March 23rd, 2020, I would be selling at a very bad time.

I’ll leave both options open to you. I think I will opt to build at least 1-years worth of my retirement budget by letting dividends pile up in my account in advance. Either way, you must have a cushion ready to retire. Then, everything is a lot easier going forward. Next step: how to make sure you always generate enough cash?

Let’s Build Your Safe Money Printing Machine

Once you have defined your financial needs and put some cash aside, you are ready for the real work of turning your portfolio into a safe money printing machine. The word safe is the operative concept. You have plenty of time to invest once you are retired. Assuming you retire between ages 60 and 65, you can assume a life expectancy of over 80 years old. Statista shows that once you reach 65 your odds of blowing more than 80 candles out on your cake are very good. This means you will no doubt live through multiple bull and bear markets. Let’s make sure you don’t outlive your portfolio, shall we? There are two common ways to generate income from your portfolio if you are a dividend investor. Let’s look closely at both.

The Dividend Option

This is the most classic option. It makes so much sense to do one simple calculation and then to think you are done. You need $30,000? Easy! Imagine you have $800,000 invested, you divide $30K by $800K and you make sure your portfolio averages 3.75% in dividend yield.

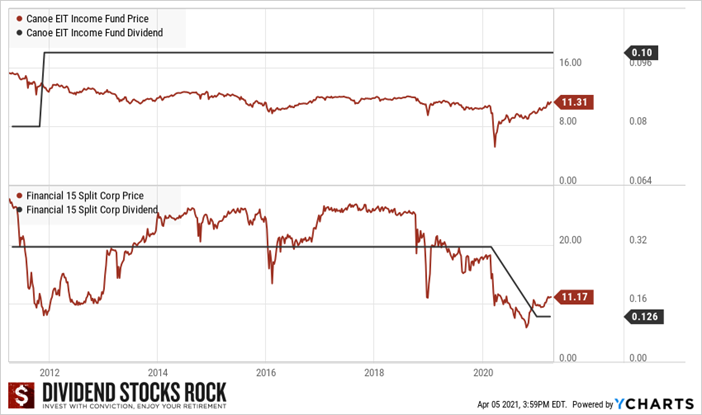

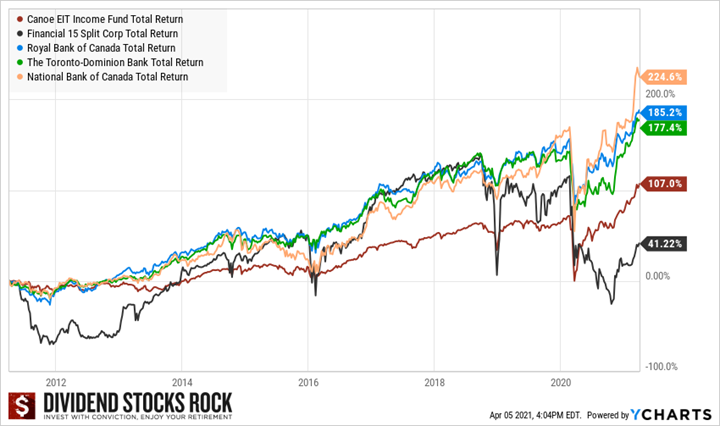

If your calculation leads to a portfolio yield of 3 to 4%, you won’t have to worry about much. In fact, you may be able to cut down your cash cushion to the 1-year worth of your retirement budget and you’ll be just fine. Unfortunately, many retirees will face a situation where they need $50,000 per year while having $600,00 invested. Then, generating an 8.3% yield isn’t that easy. Sure, you might tell me that you have found some generous MLP’s or split share products generating 8%+ yield. But, when you look at their long-term returns, you may want to revise your strategy. Here’s a quick example of the Canoe Income Fund (EIT.UN.TO) and Financial 15 split Corp (FTN.TO):

The first case (Canoe) is the “most successful one”. Your dividend income is getting eaten up by inflation year after year while your asset (the stock price) is slowly, but surely going down in value. If you are unlucky and bought the Financial Split 15, then you have suffered from both a revenue loss (dividend was cut in 2020) and a loss of capital (stock price was above $20 and now struggles to stay over $11). This is not what I call a safe money printing machine.

It’s important to note that Quadravest will describe the Financial Split 15 as a “high-quality portfolio consisting of 15 financial services companies made up of Canadian and U.S. issuers”. You could have saved yourself a lot of time and grief by buying your favorite top 3 Canadian banks and calling it a day.

Dividends Aren’t Guaranteed and They Aren’t Magical

As you probably already know, I’m a dividend growth investor who focuses on total returns. I use dividend metrics to select stocks, but my goal is to generate the best return possible. Many classic buy and hold dividend investors will tell me the following when they look at my portfolio:

“Mike, your portfolio and returns are great, but your capital gain doesn’t count. Capital gains don’t exist until you cash it. Therefore, it’s not as real as my 8% dividend yield being deposited in my account each month.”

This is where those investors are incorrect when they assume their 8% dividend yield is more “secure” than a total return portfolio offering an 8% return made up of 3% yield and 5% capital gain.

I understand the 8% yield is easier to calculate and looks more stable. After all, if the company pays 8% each year, you don’t have many calculations to do. You cash your dividends and you move on. However, how many of those 8% yielders eventually cut their dividend and you wake up to a massive capital loss as well?

The answer? Enough of them to kill your retirement portfolio.

Back in 2014, I had this conversation with a reader calling himself a well-seasoned investor with a portfolio filled with high yielder stocks. He offered four of his favorite picks back then as an example: (Kinder Morgan (KMI), Breitburn (BBEP), Starwood Property (STWD), Ares Capital (ARCC).

If you are looking for Breitburn on the graph you won’t find it because it went bankrupt in 2018 and became Maverick Resources. Therefore, out of 4 “safe” companies paying high yields, two of them barely made as much as a classic dividend growth ETF, one (KMI) crashed by 35% (including the dividend) and the last one (Breitburn) wiped out your money completely.

How many bad picks do you need to crush your retirement dreams? Imagine that you have 30 stocks in your retirement portfolio and if about 4 of them underperform then you may have a major problem. Especially now that we have ultra-low interest rates, picking up stocks with high yields is like skating full speed without knowing how to turn.

Managing a Monthly Budget with Quarterly Dividends

Then again, in an ideal world, we would have all monthly dividend stocks at retirement, and we won’t have to manage our budget.

Unfortunately, when you analyze the dividend stocks available, and when you take the time to rate them all from 1 to 5, you will notice that you don’t find many great monthly dividend stocks (rating 3 or more).

This means one must also pick among companies paying quarterly dividends. Should you match your dividend payments with specific months? Some investors like to play around with the “dividend cycles” and identify stocks according to their month of dividend payment:

- JAJO: January, April, July, and October

- FMAN: February, May, August, and November.

- MJSD: March, June, September, and December

Using that strategy, you could manage to have about the same dividend paid each month by distributing your assets through companies paying on various dividend cycles. While it looks nice on paper, I find this strategy restrictive and overly complicated.

It’s restrictive because it prevents you from investing in your favorite companies in each sector. You are condemned to picking stocks according to their dividend cycle and not by their fundamental value characteristics.

It’s overly complicated since one must monitor dividend growth for each cycle and make sure a group doesn’t overperform (or underperform). Over the long haul, a 3% rise in the dividend growth rate or a dividend cut would force you to redo all your calculations.

For those reasons, I prefer to have a 12-24-month cushion and withdraw some money from it during lower months and let the extra cash accumulate during the more generous dividend revenue months. In the end, years go by so fast that I don’t think one should focus on the moment or frequency with which dividends are paid. The work should be put towards building a portfolio filled with amazing companies showing stellar fundamentals from various sectors instead of “OK” companies paying a dividend during the right month. Now, let’s talk about those stellar dividend growers.

The Make Your Own Dividend Option (My Favorite)

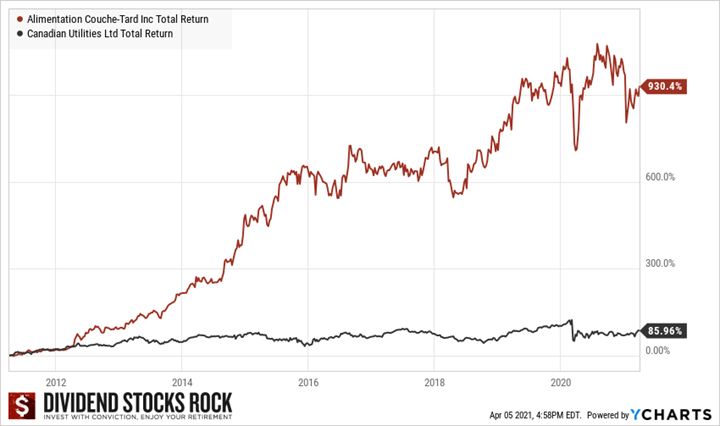

I had another great conversation with a DSR member recently. She was comparing stocks like Canadian Utilities (CU.TO) and Alimentation Couche-Tard (ATD.B.TO) from a retirement perspective. In other words, she was trying to determine which stock would be a better fit to generate income.

On one side, you have a utility with limited growth potential, but an impressive dividend growth history (49 years!). With a yield of 5%, it looks like a no-brainer. I agree.

On the other side, you have a growth-oriented company with an impressive dividend growth rate (24% CAGR over the past 5 years), but with a mediocre yield (0.80%).

How much time it will take Couche-Tard (0.80% yield) to reach Canadian Utilities’ yield? Short answer: forever.

Verdict? Pick Canadian Utilities and ignore Couche-Tard!

Not So Fast.

Let me remind you of the concept of total returns ?. As I mentioned earlier, dividends aren’t guaranteed and let alone magical. Couche-Tard offers a low yield because the company is heavily focused on growth. It pays a small yield but uses most of its money to grow the business and create added value for shareholders.

Finance 101: if a company finds opportunities to generate value for shareholders, it must use its cash flow. If it can’t, then the dividend appears to allow shareholders to allocate capital in a more optimal way.

Now, instead of wondering how much time Couche-Tard will take before it generates an interesting revenue coming from its dividend alone, you should wonder how Couche-Tard’s stock price could rise faster than Canadian Utilities. The answer? Quite shocking if you look at the past 10 years.

That’s right, over the past 10 years, ATD surged by almost 1,000% while Canadian Utilities didn’t even hit 100%. If I had invested 100K in ATD in 2011, I would have nearly $1M to fund my retirement today. With CU? Less than 200K. Which amount will generate the most income? At this point, it’s a rhetorical question.

The solution is not to invest in all the Couche-Tard’s of this world and ignore the Canadian Utilities. If you are retired, you want some “sure shots” like CU in your portfolio. This type of company brings stability and a decent expectation you will generate good income year after year.

I used this extreme example because I wasn’t cherry-picking as it originated from a real-life example from a member. Also, it shows that a balance between low yield, high growth stocks, and classic “retirement stocks” such as utilities and REITs could create the perfect blended retirement portfolio.

As I mentioned earlier, dividends aren’t magical. Therefore, instead of getting a high yield from Couche-Tard, you get high growth. Once retired, you can easily take your “one-million-dollar investment” and generate your own dividend by selling a few shares on occasion.

Remember this: the value is either in the dividend or it’s the share value. It’s the exact same thing. If you focus on building a portfolio filled with amazing dividend growers, you won’t have to worry about your average dividend yield. However, it doesn’t mean you can’t increase it!

Final Thought

There are no secret ways to create your retirement portfolio. In fact, while this “new” portfolio must sustain your retirement, it doesn’t mean it should be completely changed from your previous portfolio. The strategy you used for all those years to grow your portfolio is still valid once you are done with the growth phase.

I can see myself keeping stocks like Couche-Tard, Visa, or Apple along with Fortis, Enbridge, and Telus. I think the combination of both income-focused and growth-focused stocks will allow me to have the best retirement possible.

The post How to Turn Your Portfolio Into a Safe Money Making Machine appeared first on The Dividend Guy Blog.