How can I pay for my children’s tuition fee?

This is a question we often ask ourselves when we see our kids blowing their candles on their 16th birthday (like it or not, they will still accept candles if they get a bigger piece of the cake!). At that point, it is sometimes too late to think about funding their education. Hopefully you read this article before it happens.

I’m going to do a brief review of how to start saving for your child’s education and I will quickly jump to what is of interest: how do you build and manage a children’s tuition fund?

First, you need a 529 plan or an RESP

If you are in the U.S., the 529 savings plan seems appropriate. From my understanding, this is a flexible investment account where you can shelter funds from taxes as long as you use it to fund your children’s education. For the rest, I’ll let my fellow blogger Jeff Rose explain it to you.

If you are Canadian, then you are blessed! On top of being a tax sheltered account, the Registered Education Saving Plan (RESP) also grants you with both federal and provincial subsidies. Where I live, in Quebec, each time I invest $100, both gov’t get together and add another $30. This rules work up to $2,500 per year per children (imagine how much it makes sense I have three!). If you want to read more about it, I suggest you go over Mike Holman’s monk work about the RESP.

Second, you need to invest each month

Forget about the “oh, I’ll do it later” and start saving now. When you think about your retirement, you probably have 20, 30 maybe 40 years in front of you. This is not the case for your children. Depending on the situation, you will start withdrawing between the age of 18 and 20. Therefore, if you wait just a few years, you will be late. I’ll be honest with you, I only started when my oldest son was 7… Fortunately, tuitions costs in Quebec are a fraction of what it is elsewhere in Canada or the U.S.

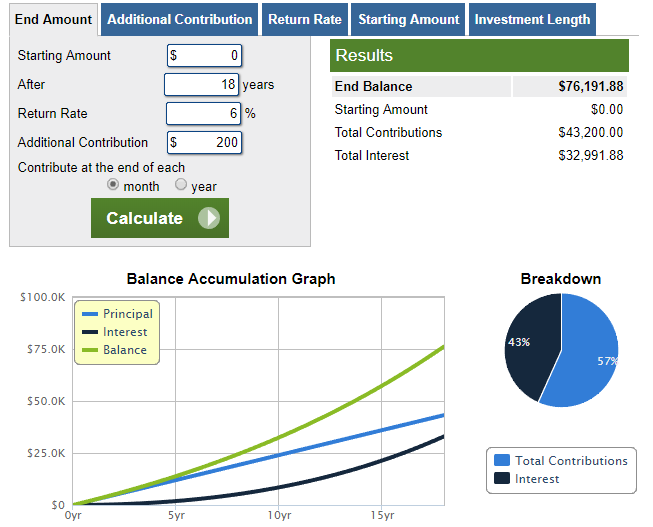

If you start saving money right when your child is born, you can achieve miracles. I love the easy to use the calculator at Calculator.net:

As you can see, $200 per month for 18 years at 6% and you have over 76K to fund your child’s education. That’s a very cool 18th birthday gift if you ask me!

Now; How do you build your education fund portfolio?

Savings account rules and calculators are nice, but it doesn’t tell you what to do with your money. While I was doing research on the internet, I noticed that there are lots of articles about the former topics, but a lot less about the latter. Your “children fund” has a shorter lifespan than your retirement account. You have less time to save and a shorter withdrawing period. Both facts have a tremendous impact on how you should manage this account. Obviously, this should be managed apart from your retirement strategy.

If you start early, you can still aim at an aggressive portfolio. This is what I did when I chose to invest 100% of my money in equities. I’m saving money on a monthly basis and add a new position each time I reach about $2,000. This goes quite fast as I combine my monthly savings, the government’s’ subsidies and the dividend I receive from my holding.

At first, I used the DSR Start portfolio as a source of inspiration. This portfolio has been created for beginner investors who have little money to invest. Therefore, we start with 4 companies. It is hard to diversify your investment when you have only a few thousands to distribute among 3-4 companies, right? For this reason, this portfolio aims at “sure shots”. Companies with a business model offering more diversification than balanced mutual funds with a stellar dividend history. Here are a few ideas for “starters”:

3M Co (MMM): 3M Company is definitely more diversified than a balanced mutual fund. It is present in various consumable product areas and the bulk of its sales comes from business-to-business transactions. Roughly 50% of its products are consumable, which implies a very high rate of repeat business year after year. Product diversification is at the center of MMM business which offers continuous growth opportunities.

Procter & Gamble (PG): If you buy shares of PG, your goal must be to earn a steady and increasing flow of income. Procter & Gamble is probably more stable than most bonds and pays a higher yield. There are no threats around this company that will jeopardize its dividend in the future. PG is a strong core holding, no matter how much you pay for it. However, don’t expect to see the stock price surge!

Johnson & Johnson (JNJ): JNJ is a powerful engine that is continuously being fueled to turn even faster. An investment in JNJ is an investment in a world-class company. You buy a complete brand portfolio with only winning products. The company is well diversified among its product offering, its pharmaceutical division along with its world diversification. Despite its relatively low yield, the company will not only reward you with a constant and increasing dividend, but also with a steady capital appreciation.

Royal Bank (RY.TO): As the largest Canadian Bank (sometimes 2nd behind TD depending on which metric you follow), Royal Bank makes money from various segments. While their classic “savings & loans” division is making steady money from both commercial and retail clients, RY has growing interest for capital markets and wealth management.

Emera (EMA.TO): Emera is a very interesting utility now that it has completed the purchase of the Florida-based TECO energy last year. EMA now shows $28 billion in assets and will generate revenues of about $6.3 billion. It is well established in Nova Scotia, Florida and four Caribbean countries. This utility counts on several “green projects” with hydroelectricity and solar plants. This decreases the risk of future regulations affecting its business as the world is slowly moving toward greener energy.

Canadian National Railway (CNR.TO): Canadian National Railway is the most productive railroad company with the best operating ratio of the industry (55.1%). At a 1.64% yield, we can’t talk about a “strong” dividend payer. However, after digging further, I realized how strong the company’s fundamentals are. CNR has a very strong economic moat as railways are virtually impossible to replicate. Therefore, you can count on increasing cash flow coming in each year. Plus, there isn’t any better way to transport most commodities than by train.

*Those companies description has been taken from useful 2 pagers documents I call Stock Cards. They include all relevant information you need to decide if a company fits in your portfolio.

As your portfolio grows, your core will take form and you may want to add one or two “growth” stocks. Still, I’m not too keen on “playing” with my children’s education money does not appeal me. I decided to keep my decisions of buying Amazon (AMZN) and Shopify (SHOP.TO) in my own retirement portfolio. I decided to focus solely on strong dividend growth companies to build my kid’s school savings account.

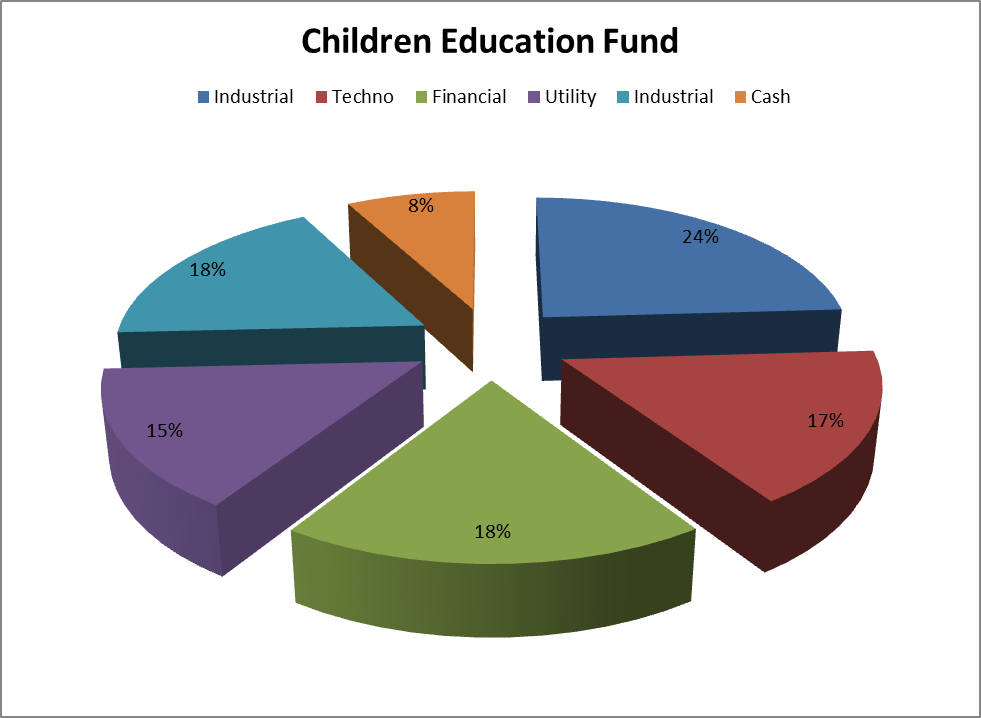

Here’s what mine looks like

I’m pretty sure looking at my portfolio will give you an idea on how to build yours. Therefore, here’s a quick peak of what it looks like:

| Company Name | Ticker | Sector | Value |

| 3M Co | MMM | Industrial | $3,803.00 |

| Apple | AAPL | Techno | $2,623.00 |

| Royal Bank | RY.TO | Financial | $2,917.00 |

| Emera | EMA.TO | Utility | $2,386.00 |

| Union Pacific | UNP | Industrial | $2,825.00 |

| Cash | Cash | $1,246.00 |

As you can see, I couldn’t resist adding AAPL to this account too. I bought UNP when the whole railroad was undervalued back in 2016 (I bought CNR.TO in my retirement portfolio at the same time). At this pace, I should be able to add a new position early in 2019. I may look at a consumer stock to improve my diversification again.

Since I have three children that are now 12, 10 and 5, I still have several years in front of me to manage this portfolio. I will start withdrawing money for my oldest son in about 8 years. If I can’t save more money than I am right now, I should be able to give $15,000 to each kid. I wish to increase my savings in 2019 as my business grows. So far, I’m able to put $100 per month aside (+$30 in subsidies). Hopefully I’ll be able to double that amount next year!

The post How to start an education fund for your kids appeared first on The Dividend Guy Blog.