The arrival of a Lump Sum of money would likely create mixed emotions. It could come from a former employer pension plan, an inheritance, the sell of a property or a business, or simply because you have been sitting on the market sideline for a while and you are now ready to invest. In any case, receiving an amount over $100,000 is quite exciting. You picture several projects and a world of possibilities open-up. Unfortunately, the sudden arrival of a Lump Sum of money comes with it loads of concerns. Today, I’m going to answer a crucial question:

How Do You Invest a Lump Sum of Money?

I once took less than 30 days to invest $76,000

If you have been searching the web for a methodology on how to invest a large amount of money, you’ve probably read tons of articles about how people would do it. I always had a problem with people knowing stuff, but not doing them. When it comes down to investing money, there is a huge gap between theory and reality. All the would, could, should take a whole different meaning when you hold a check with several zeros in your hand.

In 2017, I quit my job and decided to manage the commuted value of my pension plan. I received a lump sum payment of $108,760.02. This money was meant to be invested for my retirement. I invested the first $76,000 within a few weeks and completed my portfolio a few months later. The entire amount was invested in dividend growth stocks (50% Canadian, 50% U.S., no international companies).

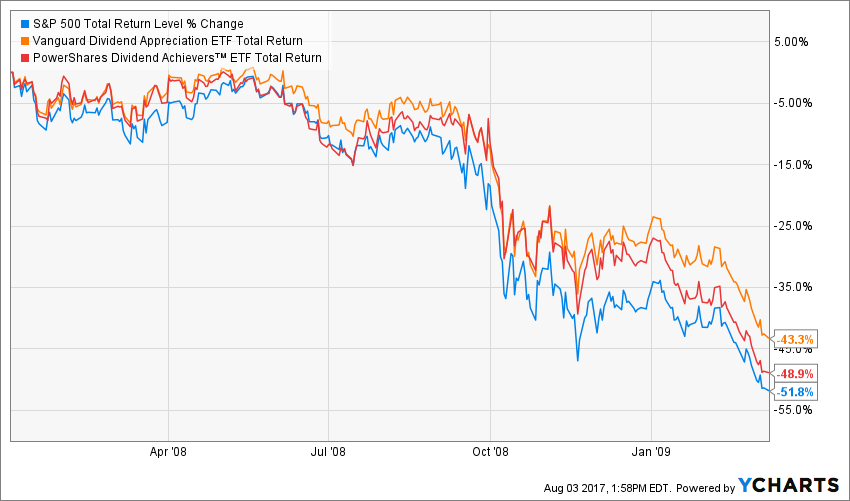

At that time, 2017 represented the stock market all-time high for both Canadians and Americans. How do you invest a Lump Sum of money when the market is at its peak? I was well aware of what could possibly happen if I had picked the wrong year to invest. From peak to bottom, investors saw the stock market lost about 50% of its entire value during the 2008 financial crisis:

Source: Ycharts

Just the thought of losing $50,000+ within a few months is enough to keep you waiting for a very long time before making an investment decision. But is waiting really the solution? You’re just postponing the inevitable: invest the money. Since it was my decision to quit the corporate world, I knew this money was coming. Here’s what I did before I received the money.

Investing a large sum isn’t easy: 3 Things to do before

First, planning is everything. Before you even get the money in your hand, you should consider what you want this money to do for you. Keep in mind that money is there to work for you and enable you to enjoy life, not the opposite. In my case, this lump sum amount needs to be invested for my retirement. The purpose of your money will determine how you will invest it (e.g. for the next 5 years or for the next 30 years). I determined I would invest this amount with a long-term investment horizon. If you don’t know if you should take the lump sum payment or keep your former employer pension, I’ve designed a decision grid to help you.

Second, will you take care of your investment or hand it over to an advisor? Money is a very personal matter and nobody cares more about your portfolio than you. However, if you lack time, interest, or knowledge, having a professional looking over your investments could be a smart thing to do. Since I’m passionate about finance and have plenty of time to manage my portfolio, I decided to trust my methodology. If you don’t feel comfortable managing your portfolio just yet, you can receive my portfolio update (I share everything) through my free newsletter:

Join 22K+ Serious Investors

Dividend Stock Ideas, Special Reports and Strategies.

Third, get an action plan ready. Actions speak louder than words. You can talk about investing your money for months and you will wake up a year later with nothing done. Before I even receive my check, I had built a buy list with all the stocks I trust to fund my retirement when I grow old.

Lump Sum Investing Vs Dollar Cost Averaging (DCA)

Now, the big day has arrived, and you wonder if you should invest all that money within a few days or weeks or if you should wait and invest a little every month. This strategy of investing a small portion of your lump sum over a 12 to 18 months period is called dollar cost averaging (DCA). For example, let’s assume you want to buy for $12,000 of shares of Johnson & Johnson (JNJ). The DCA approach would consist of investing $1,000 each month during a full year. If JNJ shares goes up or down during that time for an unexpected event, you will average the cost of your shares. The DCA is a seductive strategy when you fear JNJ shares will drop by 20% a few weeks after buying a lump sum of $12,000 in a single transaction.

Because there is no way I can predict what will happen in the next 12 months…

Because the more transaction I do, the more fees I pay…

Because I want my money to work for me and not me working for my money…

I decided to put all my money in the stock market as soon as possible. I don’t see a strong incentive to use DCA unless I was in early 2008 and knew what was coming. Keep in mind that seeing the market drop by ~50% during a short period is also a very rare phenomenon.

Here’s a very interesting article about the difference between lump sum investing and dollar cost averaging and a paper from Vanguard about the same topic.

How do you invest the money?

I like to keep things simple. I think that too many investors suffer from “paralysis by analysis” as they try to know and control everything. You can spend days, weeks, months looking at charts, metrics, comparisons and all you will do is waste valuable time and your money will still not be invested.

Here’s how Invested my lump sum of money:

#1 Build a virtual portfolio

Getting good results out of your investment is all about your asset allocation. If you don’t know in which asset class and in which sectors you want to be, there is no point in starting a stock filter and buy stocks. I started by selecting a portfolio model at DSR. They have been proven to post robust results since 2013 and performed well during the flash crash of 2018. You can get the results here.

#2 Build my watch list

Once I decided what my portfolio will look like in term of asset allocation, I spent time analyzing each stock in the portfolio model. I used the DSR stock cards and rankings to get a quick idea of which companies would fit well for my retirement portfolio. This is the hardest and longest part of the process as this is where you will wonder if you should or shouldn’t pick a company. Take the time to pick the right stocks, they will accompany your in your investing journey for a while after that.

#3 Get the Lump Sum work for you – buy now

As soon as you get your check, you should put that money to work. Invest the proceeds in the stock market now. When is now? It’s NOW.

Don’t wait to see what the next FED meeting will say.

Don’t wait for the next election round.

Don’t wait for the next earnings season.

Don’t wait for the “currently big conflict between countries” end.

Don’t wait for the next market crash.

Don’t wait for the time the market will be better valued.

Waiting isn’t paying. I agree with you that in an ideal world, you would buy stocks at the cheapest level possible. Unfortunately for you and me, those low price were 10 years, 25 years, 50 years ago. The good news is that in 25 years, the good timing to buy stocks will be… today.

Bear markets, as we like to call them, take on average 2 years to recover. Will you really wait 1 months, 1 years, 4 years before the next market crash only to realize it would take 2 years to recover your money?

I invested a large amount in the market in 2017. 2 years later, my account was showing a total gain of ~+38%. If 2017 was the year of a massive market crash, my portfolio would have shown a ~0% return in 2019. And from then on, my money would continue to work for me. Does waiting work? Not at all.

If you are looking for more tricks and tools I use, I describe the entire process of my investment right here.

The post How to Invest a Lump Sum of Money appeared first on The Dividend Guy Blog.