From Chips to Chatter: Telecoms and Semiconductors Landscape – Subsectors Series [Podcast]

February 28, 2024

ASML Stock, AT&T stock, AVGO stock, BCE stock, Best Dividend stocks, best semiconductor stocks, best telecom stocks, blog, CMCSA stock, Comcast stock, INTC stock, KLAC stock, LRCX stock, NVDA stock, Podcast, QCOM stock, semiconductor subsector, semiconductors industry, T stock, T.TO stock, telecom industry, telecom subsector, Telus stock, TSM stock, TU stock, TXN stock, Verizon stock, VZ stock

0 Comment

Subscribe

The Communication Services and the Information Technology sectors have significantly evolved in recent years. More specifically, Telecoms and Semiconductors have faced many challenges. What are the pros and cons of these industries? Which companies should investors dive into? What can they bring to their portfolios? Let’s hit chips and chatter!

Subscribe to our newsletter to receive our Get the Best of 6 Sectors issue.

You’ll Learn

- Telecoms are part of the communication services sector, which has been dramatically transformed in recent years with big players such as Google and Disney. What else should investors know about this sector?

- The Telecom industry is capital-intensive and enjoys predictable cash flow. What other main characteristics does it have?

- On the other hand, debt can be a big struggle for them. Mike explains to what extent debt remains acceptable.

- There’s a big difference between Canadian and American telecoms, mainly explained by the oligopoly they benefit from in Canada.

- Would the oligopoly explain why Telus (T.TO) and BCE remain Mike’s favorites?

- We couldn’t do this episode without a few words about some US telecoms: Comcast (CMCSA), Verizon (VZ), and the good old (or not so good old) AT&T (T). What are Mike’s thoughts on them?

- Let’s move to the semiconductors, part of the Information Technology sector, which has significantly changed in the last decade to the point that it impacts the entire US market.

- We all remember the 2020 chip shortage, greatly affecting the semiconductor industry. What else is there to know about this subsector?

- When are semiconductor companies more prone to perform well, and when are they more at risk?

- Unlike Telecoms, the semiconductors we will discuss today are all on the US market. Among the ones with the best ratings at Dividend Stocks Rock (DSR), we can find Taiwan Semiconductor (TSM), Texas Instruments (TXN), Broadcom (AVGO), and Qualcomm (QCOM). What is there to like about them?

- Intel (INTC) and Nvidia (NVDA) are also well-known companies in the semiconductor subsector. However, they have a weaker rating at DSR with a 2 for Dividend Safety. What could explain that?

- We couldn’t end the episode without a few thoughts on semiconductor equipment businesses such as Lam Research (LRCX), KLA Corp (KLAC), and ASML. Mike explains more about them.

Related Content

Catch up on the series with the previous episode about Groceries and Restaurants.

A Deep Dive into Groceries and Restaurants: Pros, Cons, Best Stocks – Subsectors Series [Podcast]

Here’s the episode Mike did with European DGI, his EuroClone!

Dividend Growth Investing with European DGI [Podcast]

Subscribe

The Best Dividends to Your Inbox!

Download our Dividend Rock Star List now and do not miss out on the good stuff! Receive our Portfolio Workbook and weekly emails, including our latest podcast episode!

Follow Mike, The Dividend Guy, on:

- YouTube

Have Ideas?

If you have ideas for guests, topics for The Dividend Guy Blog podcast, or simply to say hello, then shoot me an email.

This podcast episode has been provided by Dividend Stocks Rock.

![]()

The post From Chips to Chatter: Telecoms and Semiconductors Landscape – Subsectors Series [Podcast] appeared first on The Dividend Guy Blog.

Canadian Low Yield Stocks Even Retirees Will Like

February 22, 2024

Discover great Canadian low yield stocks even retirees will like because of their solid growth potential. You’re decades away from retirement? They’re great for you too! None of the usual suspects this time though, no Alimentation Couche-Tard, Canadian National Railway, TFI International. Curious? Keep reading…

Why low yielders?

By selecting the right low yield stocks, you can enjoy both sustained dividend growth that exceeds inflation and capital appreciation. Actually, low yield high growth stocks very often outperform more mature high-yielding stocks in the long run, thus securing your retirement whenever that might be, as explained in Low Yield, High Growth Stocks for your Retirement.

The good news is that there are plenty to choose from, and in different sectors. If you have a retirement portfolio, they complement your income stocks often found in the Utilities, REIT, and Financials sectors and improve your diversification. Growth investors still in their accumulation phase will also reap the benefits. You might also like What makes companies pay a high or low yield?

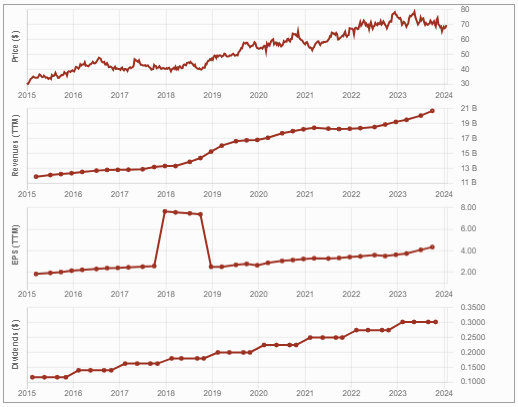

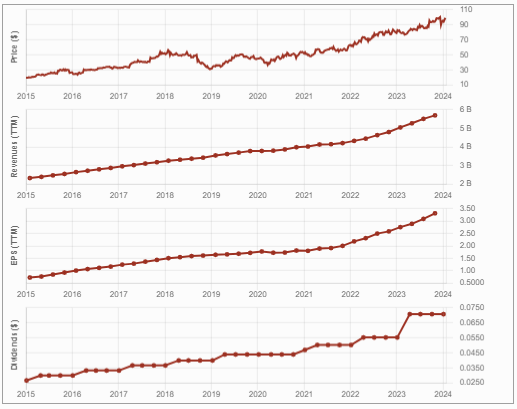

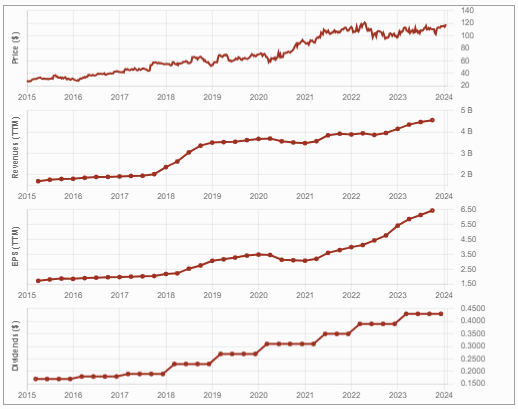

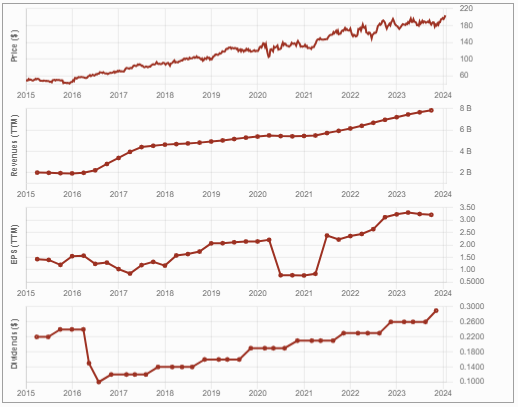

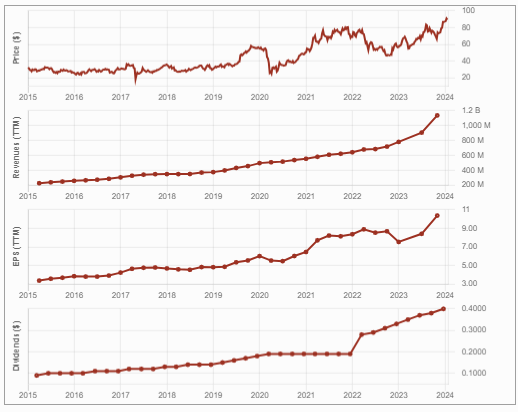

For each stock I selected below, I tell you why I like the stock, and include a graph showing the stock price evolution over 10 years and the dividend triangle (the revenue, earnings per share (EPS), and dividend payment trend over 10 years). I also highlight some risks the companies face.

For more stock ideas, download our Top Stocks for 2024 booklet.

Metro (MRU.TO) – Consumer Staples

The smallest, yet fastest growing grocery store in Canada. Metro focuses on the Quebec and Ontario markets where population growth and the economy are quite healthy. Metro has emphasized its private-label brands, which sell for 20% less than original brand products. In a world where price is the main consumer driver, this is a key advantage. Metro is also pushing its online services to gain customers. The grocer is impressive as it increases sales while keeping expenses under control in this high inflation environment. So far, Metro has kept healthy margins, and benefits from higher inflation to boost its sales.

Metro also profits from its strong Brunet and Jean-Coutu drugstore network. However, with 71% of its food stores and 82% of its drugstores found in Quebec, there’s limited growth opportunities there; Metro must expand in other provinces where competition is fierce. Finally, Metro could unlock more value by spinning off its real estate properties and Loblaws and Empire did a while back with Choice Properties and Crombie.

Dollarama (DOL.TO) – Consumer Discretionary

You won’t pay your utility bills with your Dollarama’s dividend yield. Management doesn’t share the wealth with shareholders yet, mainly because it sees so many growth opportunities. By acquiring 51% of Dollarcity, DOL has international growth potential in Latin America. At the same time, DOL continues to enjoy a stable Canadian economy, with over 1500 stores in the country.

With a possible recession looming, Dollarama is definitely a stock to look into. Many Canadians shop at DOL regularly to cut down their expenses. DOL generates high gross margins (44%) on the many private label products (63%) it sells. The company’s growth plan is to open more stores and expand in Latin America.

Although Dollarama dominates in Canada, similar U.S. chains (e.g., Dollar Tree) are eyeing the Canadian market. Latin America shows strong potential but comes with volatility due to occasional political and economic instability. Another problem is pressure on margins due to inflation making harder to sell inexpensive items, even with large volumes. So far, DOL’s proven highly resilient and shows a strong dividend triangle.

Toromont Industries (TIH.TO) – Industrials

If you want to make a play on infrastructure spending, Toromont is a good candidate. Toromont is one of Caterpillar’s largest dealerships in Canada. TIH covers industries from roadbuilding to mining and telecommunications to food and beverage processing. In addition to relying on mining (20%) and construction (38%) to grow organically, TIH also buys smaller dealerships, such as Hewitt (acquired in 2017). Revenue growth wasn’t impressive since the pandemic, but has picked up in the recent quarters.

TIH continues to face construction delays and inflationary pressure. Its mining and construction customers have cyclical and capital-intensive businesses that are sensitive to high interest rates and a slowing economy. A recession would cause weaker results.

Considering the massive infrastructure spending needs in Canada in the coming years though, Toromont could do very well. Want to know more about Toromont Industries, check out our Buy List Stock of the month article.

For more stock ideas, download our Top Stocks for 2024 booklet.

Waste Connections (WCN.TO) – Industrials

An integrated solid waste services company, WCN provides non-hazardous waste collection, transfer and disposal services, and resource recovery through recycling and renewable fuels generation. So long as we consume stuff, demand will be high for WCN services. Waste Connections is a classic “I like this business, but it’s too expensive” play.

The company shows an impeccable dividend triangle as it continues to grow by acquisition. Management has been adept in integrating their acquisitions. Therefore, it’s not only growing, but becoming more profitable.

EQ Bank (EQB.TO) – Financials

EQB supplies diversified banking services through its EQ Bank platform and has two divisions: Personal Banking and Commercial Banking. Its non-conventional business (including online presence and reverse mortgage products), along with its aggressive dividend growth policy, made EQB popular among investors. The innovative bank shows impressive growth across all loan products and deposits over the past 5 years.

EQB built a fast-growing business while being surrounded by giants. This small fish in a big pond is going for quickness, simplicity, and seamless digital banking. Let’s just admit the big six are decades behind in that regard. While I’m a big fan of National Bank, I must admit that EQB shows quite the record in the past few years.

EQB has a very strong dividend triangle but keep in mind that higher interest rates have a lagging impact on the economy. Make sure it just doesn’t look good on Prom night; review quarterly results to detect growth slowdowns or higher provisions for credit losses.

Final Thoughts

As a dividend growth investor, I prefer low yield high growth stocks. Retirees often hesitate to buy such stocks for various reasons, some explained in Why Ignore Low Yield Stocks when Planning Retirement? I believe that income-seeking investors benefit immensely by having a balance in their portfolio between low yield high growth stocks and more traditional retirement high yield stocks.

The post Canadian Low Yield Stocks Even Retirees Will Like appeared first on The Dividend Guy Blog.

A Deep Dive into Groceries and Restaurants: Pros, Cons, Best Stocks – Subsectors Series [Podcast]

February 21, 2024

AW.UN.TO stock, best consumer discretionary stocks, best consumer staples stocks, Best Dividend stocks, best grocery stocks, best restaurant stocks, blog, EMP.A.TO stock, Empire Stock, grocery stores industry, grocery stores subsector, KR stock, Kroger Stock, MCD stock, Metro stock, MRU stock, Podcast, QSR stock, restaurants industry, restaurants subsector

Subscribe

How do industries help investors diversify their portfolios? What are the main strengths and weaknesses of the Consumer Discretionary and Cyclical sectors? More specifically, what are the characteristics of the grocery and restaurant subsectors? Learn the pros, cons, and best stocks of these industries!

Subscribe to our newsletter to receive our Get the Best of 6 Sectors issue.

You’ll Learn

- First, let’s address how to use subsectors to diversify an investor’s portfolio. At DSR, we believe that investors should not invest more than 20% in a single sector. We also think that investors should only invest in sectors that they understand. Mike explains why we believe that and how looking at each sector’s different industries can help.

- Some sectors are more diversified than others. Which ones could investors invest in more than 20% without too much risk?

- And what about companies that fit into multiple sectors or subsectors? How to classify them?

- Grocery stores are part of the consumer staples (or consumer defense) sector. Let’s do an overview of this sector’s strengths and weaknesses.

- The Grocery Stores industry is stable, recession-resistant, and easy to understand. However, high competition and thin margins can make things complicated.

- Of course, grocery stores are essential, so they seem reliable at any time. But what makes them perform at their best? And when are they negatively impacted?

- Metro (MRU.TO), Empire (EMP.A.TO), and Kroger (KR) represent the industry well. What makes them among the best stocks for this subsector?

- We could make a direct link between Groceries and Restaurants. Yet, they’re not in the same sector. Restaurants are part of the Consumer Discretionary (or Consumer Cyclical). What’s the main difference for this sector?

- Restaurants are pretty easy to understand, but there are almost two industry types in the same subsector: steak and burger!

- Restaurants are more inclined to perform well during good economic situations. Convenience, brand name, and economies of scale are other strengths to consider.

- On the other hand, the franchise system is a double-edged sword.

- We selected three companies that are direct competitors in the fast food restaurants: Restaurant Brands International (QSR), A&W Revenue Royalties (AW.UN.TO), and McDonalds (MCD). Why are they part of the best restaurants?

- Then, we have Starbucks (SBUX), the deluxe coffee shop, and Keg Royalties (KEG), a well-known steakhouse and bar chain. How do they differ from fast food, and does Mike like them both?

Related Content

Catch up on the series with the first episode on Pipelines and Utilities.

Unveiling the Dynamics of Pipelines and Utilities: Pros, Cons, Best Stocks – Subsectors Series [Podcast]

For more analysis of companies offering luxury treats at cheap prices, watch this video below!

Subscribe

The Best Dividends to Your Inbox!

Download our Dividend Rock Star List now and do not miss out on the good stuff! Receive our Portfolio Workbook and weekly emails, including our latest podcast episode!

Follow Mike, The Dividend Guy, on:

- YouTube

Have Ideas?

If you have ideas for guests, topics for The Dividend Guy Blog podcast, or simply to say hello, then shoot me an email.

This podcast episode has been provided by Dividend Stocks Rock.

![]()

The post A Deep Dive into Groceries and Restaurants: Pros, Cons, Best Stocks – Subsectors Series [Podcast] appeared first on The Dividend Guy Blog.

Favorite Mid-Yielders – January Dividend Income Report

February 15, 2024

best mid-yield stocks, blog, dividend guy portfolio, dividend guy portfolio results, Dividend Guy portfolio returns, Dividend Income Report, Medium yield stocks, mid-yield dividend stocks, mid-yielder stocks, mike heroux portfolio, stocks mid yield canada, stocks mid yield dividend, stocks mid yield US, stocks with mid-yield, the dividend guy portfolio

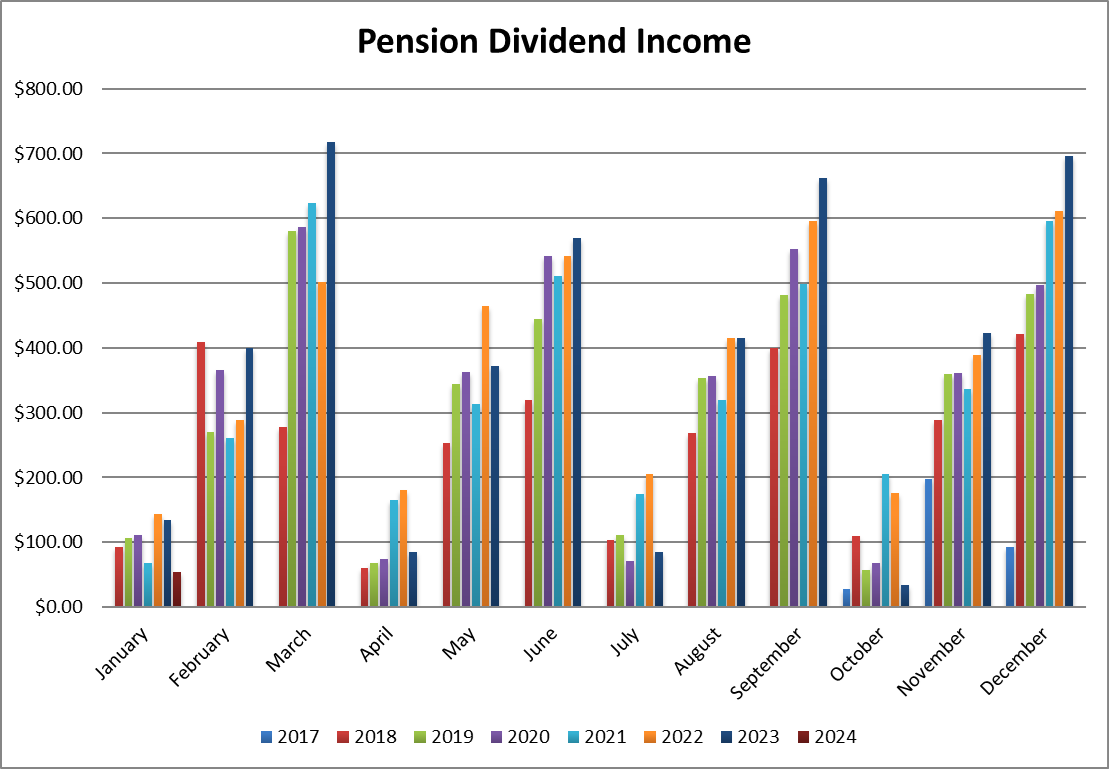

In September of 2017, I received slightly over $100K from my former employer, representing the commuted value of my pension plan. I decided to invest 100% of this money in dividend growth stocks.

Each month, I publish my results on those investments. I don’t do this to brag. I do this to show my readers that it is possible to build a lasting portfolio during all market conditions. Some months we might appear to underperform, but you must trust the process over the long term to evaluate our performance more accurately.

Recently, there were many DSR members who replied to my last newsletter about the “yield battle” between low yield high growth companies with a yield under 2% but with a generous dividend growth, and high-yielding companies offering a yield above 5%. Some also inquired about what we should do with the medium yielders with dividend yields of 2-5%.

To be clear: I’m a big fan of mixing medium yielders with 2-5% dividends with low-yield, high-growth stocks.

If you look at my portfolio, you will find that mix where there is a stable foundation from the “usual suspects” offering a decent yield. On top of that foundation, you will find the low-yield, high-growth stocks propelling my portfolio value higher.

There are obviously more candidates in this category but I have tried to select my favorites while also making a diverse selection across industries. The mid-yielders must offer a decent dividend, but also a decent dividend triangle. You will notice that some of them will look a lot like a low-yield, high-growth company and some will be closer to the high yielders. Today, I share this selection with you!

Performance in Review

Let’s start with the numbers as of February 5th 2024 (before the bell):

Original amount invested in September 2017 (no additional capital added): $108,760.02.

- Portfolio value: $243,431.98

- Dividends paid: $4,510.78 (TTM)

- Average yield: 1.85%

- 2023 performance: +20.69%

- SPY= +26.19%, XIU.TO = +11.87%

- Dividend growth: +1.7%

Total return since inception (Sep 2017-Dec 2023): 123.82%

Annualized return (since September 2017 – 77 months): 13.38%

SPDR® S&P 500 ETF Trust (SPY) annualized return (since Sept 2017): 13.31% (total return 122.90%)

iShares S&P/TSX 60 ETF (XIU.TO) annualized return (since Sept 2017): 8.99% (total return 73.75%)

Canadian Favorite Mid-Yielders (2-5%)

I thought it would have been easier to find 12 stocks in the Canadian market that would meet my criterion. But If I want to be a bit more diverse and not select just financial stocks and utilities, I had to dig a little bit more than expected.

Before we jump to the mid-yielders list, here’s a thought-provoking investment strategy that relies on low-yield, high dividend growth stocks for retirement.

Brookfield Infrastructure (BIPC)

The biggest downside of BIPC is its complex structure. However, management has delivered constant distribution increases for over a decade. They always give what they promise. BIPC is an “ETF” of utilities with its incredible diversification (from pipelines to data centers and electric transmission to railroads).

Brookfield Renewable (BEPC)

Similar to BIPC, Brookfield Renewable financial statements are complex, but the distribution increases don’t lie. The company shows ~50% of its assets in the hydroelectric industry and operates worldwide.

Canadian National Resources (CNQ.TO)

I could have selected Imperial Oil (IMO.TO) that is the other exception in the energy sector when it comes to dividend growth. CNQ owns high quality assets and its vertical integration allows it to make a profit at each step of the oil industry. It’s profitable even with a barrel of crude oil priced at $35-$40!

Fortis (FTS.TO)

Fortis is probably the most boring stock I own. 99% regulated, classic distribution and transmission energy company operating utility assets in North America and the Caribbean. With a stellar management team in place, the company has delivered 50 consecutive years of dividend increases. I won’t break records with this one in my book, but it will always participate in my retirement plan!

Granite REIT (GRT.UN.TO)

Here’s a rare REIT combining a decent yield with decent growth. Granite is still exposed to its major tenant (over 25% of assets leased to Magna International), but it has lowered this exposure each year. There is a high demand for industrial properties and Granite has a large development pipeline.

Intact Financial (IFC.TO)

Selecting IFC is almost cheating as it is very close to paying a yield under 2% and it definitely has the low-yield, high-growth profile. IFC is the largest player in Canada, giving them a large amount of data to optimize its underwriting process. The company also grows by acquisitions and now has a foot in the U.S. and in Europe.

Jamieson Wellness (JWEL.TO)

Be careful with JWEL. While its narrative (selling vitamins and nutriments to an aging population) and its numbers include consistent revenue growth and generous dividend increases making the company quite seductive. Jamieson Wellness, however, remains a small cap. You know it could go both ways for them. JWEL’s biggest challenge going forward will be to maintain its growth, but also to maintain its margins so it shows some EPS growth.

Magna International (MG.TO)

Magna is highly cyclical and if you invest in this one, be ready for a wild ride. While it’s one of the world’s largest auto parts makers, the automobile industries is subject to ups and downs on regular cycles. However, management has shown it was fast to act and able to expand margins while being under pressure.

National Bank (NA.TO)

One of my all-time favorites, National Bank, continues to be at the top of my bank rankings. NA shows the most generous dividend growth while maintaining the lowest payout ratio amongst the big 6. NA’s business is well diversified and since it’s the smallest of the big guys, it can usually be nimbler in its decision-making process.

Restaurant Brands (QSR.TO)

I can’t say I’m excited about Restaurant Brands, but I can’t say I found a major flaw either. The company operates iconic brands such as Burger King and Tim Hortons. It grows organically across the world and finds a few good brands to acquire periodically. It shows good stability.

Royal Bank (RY.TO)

Royal Bank is my second most favorite Canadian bank, mostly due to its size and diversification. The company generates only 50% of its revenue from classic banking activities. I think there is more money to be made in wealth management (considering the wealth transfer between boomers and the next generation) and in capital markets. In all honesty, I could have put more banks and a life insurance company on this list as well.

TMX Group (X.TO)

TMX operates a unique business model in Canada that is often ignored by many investors. The company operates a sticky business model with several recurring revenue streams from clearing trades and derivatives, to issuing shares/IPOs, providing training and being a data provider.

U.S. Favorite Mid-Yielders (2-5%)

This is probably where it was harder to make choices. The U.S. market is filled with great companies offering a decent yield and a good dividend triangle. Many other choices could have been part of this list. Here’s a short list of stocks that have been considered but are not included in this group: American Tower, Alexandria REIT, Colgate-Palmolive, CME Group, Cummins, Equinix (too close to a low yield), Honeywell, Hershey, Coca-Cola, McCormick, Nextera Energy, Bank OZK, Qualcomm, Robert Half, Texas Instruments, WEC Energy and Xcel Energy… phew!

AbbVie (ABBV)

Depending on the day you look at it, ABBV could be a high-yielder or a mid-yielder. Its stock price fluctuates greatly according to how well its drug pipeline is developing. It’s a classic story for many big pharmaceuticals. Fortunately, its aesthetic segment (driven by Botox) is offering more stability.

Automatic Data Processing (ADP)

This one is very close to being a low-yield, high-growth company and definitely has the profile with its very strong dividend triangle. ADP operates a nearly perfect business model where it combines both stickiness (employers are not changing their payroll system often) and recurring revenues (employers don’t stop paying their employees!). However, ADP faces a lot of competition and may also suffer setbacks during a recession.

Air Products and Chemical (APD)

You will rarely find a company in the Material sector with over 40 years of consecutive dividend increases. APD has a diverse way of positioning its business in a sector where most are stuck with commodity price fluctuations. As a provider of industrial gases, APD signs long-term contracts with its customers. It provides a crucial element for many businesses which makes their business model both sticky and recurring.

BlackRock (BLK)

BlackRock is the largest asset manager and the largest ETF manufacturer in the world. Their size alone ensures stability and organic growth. While BLK stocks will fluctuate according to Mr. Market’s mood, it can count on its long-time relationship with institutional investors.

Genuine Parts (GPC)

Genuine Parts is the type of business you buy, and you forget about. It provides car repair parts across North America and it is now growing in Europe. GPC is known to grow both organically and through a series of small acquisitions in a highly fragmented market. It’s not an exciting company, but it surely does something right with its more than 60 consecutive years of dividend increases.

Home Depot (HD)

This is another company that could fit in the low-yield, high-growth model (you can see I’m not trying to cheat and show weaker stocks in the mid-yielder section!). HD is the world’s largest home improvement retailer, with more than $150B in sales. HD has built a strong relationship with PRO builders as it can make everything they need available when they need it. As we expect lower interest rates later this year, this may give a small boost to the construction industry, and improve HD’s results as well.

Johnson & Johnson (JNJ)

JNJ is one of the first stocks I bought when I switched my strategy over to dividend growers. It’s definitely a classic selection that doesn’t get old. JNJ makes most of its profit from its pharmaceutical division that specializes in specialty drugs, which makes it difficult for generic drug manufacturers to compete. I think JNJ’s Pharma segment continues to offer a promising outlook due to strong prospects on existing key drugs such as Stelara, Imbruvica, and Darzalex, along with a robust drug pipeline of 14 novel drugs.

Lockheed Martin (LMT)

There were some great candidates in the defense industry, but I decided to go with one of the largest players. Lockheed has the largest military contract with the Pentagon with its F-35 program. It has been able to consistently offer growth and increase its dividend. With political tension growing, I expect LMT to leverage its expertise in defense across the world.

McDonald’s (MCD)

MCD is definitely a classic on the U.S. landscape with over 40 consecutive dividend increases. MCD enjoys strong brand recognition and is the world’s largest fast-food retailer. MCD is attentive to its customers and has introduced many changes to its menu over the years, such as all-day breakfast and healthier options. Management came with a strong and ambitious growth plan for the coming years, and I’m convinced they will do well!

I have covered more in-depth ADP, HD and MCD in the video below:

PepsiCo (PEP)

PepsiCo has been in the middle of a lot of noise as of late. First, Ozempic (a drug now used to fight obesity) will prevent millions of consumers from eating Doritos and drinking soft beverages going forward. Second, Carrefour is the first in a long line of merchants that will ban all their products. You can guess that I’m being a bit sarcastic here. PepsiCo benefits from strong non-carbonated drink brands such as Gatorade and Tropicana. PEP’s snack division is a strong leader in this industry with a 64% market share in the U.S., 60% of Brazil’s market, and 46% of the U.K. market.

Procter & Gamble (PG)

I could plead guilty for a lack of original choice, but why go for something exotic when good old classic consumer stocks work? PG is a truly diversified fund, with its 21 brands each grossing over $1B, in 5 segments, sold in over 180 countries. Procter & Gamble is probably more stable than most bonds and pays a decent yield. There are no immediate threats that come to mind that will jeopardize its dividend in the future.

Starbucks (SBUX)

Starbucks is a good example of what a low-yield, high-growth company looks like after its fast growth period is over. While SBUX can continue to grow organically in North America and shows interesting growth potential in Asia, they are far from the company they were 10 years ago. Nonetheless, I expect SBUX to maintain a generous dividend growth policy and maintain a mid to high single-digit growth rate for revenue and earnings going forward. Consumers proved their love for Starbucks coffee despite recessions and inflation in the past!

Smith Manoeuvre Update

Slowly but surely, the portfolio is taking shape with 10 companies spread across 7 sectors. My goal is to build a portfolio generating 4-5% in yield across 15 positions. I will continue to add new stock monthly until I reach that goal. My current yield is 5.04%.

Adding more of Canadian Tire (CTC.A.TO)

It’s relatively hard to find new ideas offering a yield above 4% that is not in the energy or REIT sector these days. Since Canadian Tires was my smallest position, I used my $500 to help balance my portfolio a little by buying additional shares. I get more exposure to the consumer discretionary sector by adding shares of this depressed stock. Since my goal is to keep my Smith Manoeuvre portfolio for over 10 years, I don’t mind a little volatility!

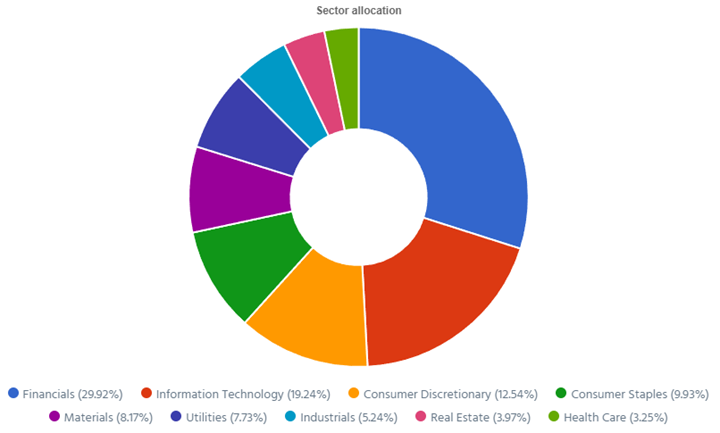

Here’s my SM portfolio as of February 5th, 2024 (before the bell):

| Company Name | Ticker | Sector | Market Value |

| Brookfield Infrastructure | BIPC.TO | Utilities | $969.80 |

| Canadian National Resources | CNQ.TO | Energy | $897.82 |

| Capital Power | CPX.TO | Utilities | $558.82 |

| Canadian Tire | CTA.A.TO | Consumer Disc. | $1,024.24 |

| Exchange Income | EIF.TO | Industrials | $1,039.72 |

| Great-West Lifeco | GWO.TO | Financials | $758.88 |

| National Bank | NA.TO | Financials | $616.20 |

| Nutrien | NTR.TO | Materials | $892.32 |

| Telus | T.TO | Communications | $905.92 |

| TD Bank | TD.TO | Financials | $1,135.40 |

| Cash (Margin) | -$50.24 | ||

| Total | $8,748.66 | ||

| Amount borrowed | -$8,500.00 |

Let’s look at my CDN portfolio. Numbers are as of February 5th, 2024 (before the bell):

Canadian Portfolio (CAD)

| Company Name | Ticker | Sector | Market Value |

| Alimentation Couche-Tard | ATD.B.TO | Cons. Staples | $23,937.94 |

| Brookfield Renewable | BEPC.TO | Utilities | $9,422.16 |

| CCL Industries | CCL.B.TO | Materials | $8,015.00 |

| Fortis | FTS.TO | Utilities | $9,211.77 |

| Granite REIT | GRT.UN.TO | Real Estate | $9,568.00 |

| Magna International | MG.TO | Cons. Discre. | $5,369.00 |

| National Bank | NA.TO | Financials | $12,426.70 |

| Royal Bank | RY.TO | Financial | $8,529.30 |

| Stella Jones | SJ.TO | Materials | 11,675.62 |

| Cash | $436.71 | ||

| Total | $98,592.20 |

My account shows a variation of -$1,592.11 (-1.59%) since the last income report on January 9th.

Since most companies will report during February, I’ll wait for next month to do a big review.

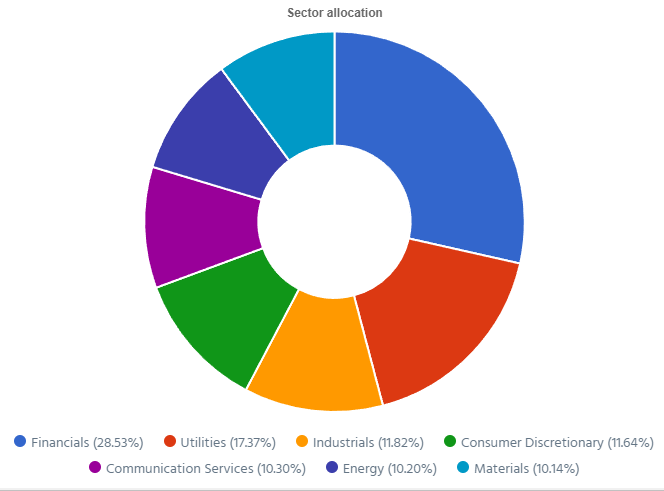

Here’s my US portfolio now. Numbers are as of January 9th, 2024:

U.S. Portfolio (USD)

| Company Name | Ticker | Sector | Market Value |

| Apple | AAPL | Inf. Technology | $7,434.00 |

| Automatic Data Processing | ADP | Industrials | $89,454.78 |

| BlackRock | BLK | Financials | $11,032.00 |

| Brookfield Corp. | BN | Financials | $13,435.31 |

| Home Depot | HD | Cons. Discret. | $10,716.90 |

| LeMaitre Vascular | LMAT | Healthcare | $5,870.00 |

| Microsoft | MSFT | Inf. Technology | $19,327.34 |

| Starbucks | SBUX | Cons. Discret. | $7,904.15 |

| Texas Instruments | TXN | Inf. Technology | $7,960.00 |

| Visa | V | Financials | $13,859.00 |

| Cash | $247.58 | ||

| Total | $107,241.06 |

My account shows a variation of +$2,604.57 (+2.50%) since the last income report on January 9th.

There were lots of companies reporting earnings over the past 30 days. Let’s review what they did!

Apple has some issues in China

02-01-2024, Apple reported a decent quarter with revenue up 2% and EPS up 16%, but the market was more concerned about China. Sales from China were $20.8B during the period, which was well below the $23.5B that analysts had expected and also showed a 4th consecutive quarter of sales declines. Here’s the sales breakdown by segments: iPhone: $69.7B (+6.0 % Y/Y); Mac: $7.78B (0.5 % Y/Y); iPad: $7.02B (-25.2 % Y/Y); Wearables, Home and Accessories: $11.95B (-11.4 % Y/Y); Services: $23.12B (+11.4 % Y/Y). It was a bit of a hit-and-miss quarter depending on the segment. AAPL generated nearly $40B in operating cash flow this past quarter.

Automatic Data Processing: strong quarter, strong guidance!

ADP reported another strong quarter with revenue up 6% and EPS up 9%, and beating analysts’ expectations. Employer Services revenue increased by 8% and PEO Services (employment administration outsourcing solutions) revenue increased by 3%. Management reaffirmed its guidance for 2024: revenue growth to be between 6 and 7% and adjusted EPS should be up by 10 to 12%. Guidance includes Employer services revenue growth of 7 to 8% while PEO services revenue is expected to grow by 3 to 4%.

BlackRock sees its dividend safety score drop!

Blackrock reported a solid quarter with revenue up 7% and EPS up 8% which handily beat analysts’ expectations. The company also agreed to acquire Global Infrastructure Partners to create a combined infrastructure platform of more than $150B and is reorganizing some of its other platforms including its Aladdin investment tech platform and illiquid alternative investments. Another good news item was their long-term quarterly net inflows were $95.6B, versus $3B of net inflows in Q3. BLK increased its dividend by a meager 2% so we had to decrease its dividend safety score from 4 to 3.

Starbucks brews more growth

Starbucks reported a good quarter with revenue up 8% and EPS up 20%. Global comparable store sales rose 5%. The average sales ticket value was up 2% and the overall transaction count was 3% higher during the quarter. In North America, operating margins jumped to 21.4% of sales in the region from 18.5% a year ago, primarily driven by in-store operational efficiencies and sales leverage. Active membership in Starbucks Rewards in the U.S. rose 13% to 34.3M during the quarter. In China, sales increased by 10% but the operating margin decreased from 14.3% to 13.1% due to higher wages and benefits. SBUX opened 549 net new stores so their growth story continues to evolve.

Texas Instruments hit a roadblock

Texas Instruments disappointed the market with declining numbers (revenue down 13%, and EPS down 33%). Results were affected by declining demand from both industrial and automotive industries. This is one more sign telling us a recession may be looming. Over the past 12 months, TXN generated $6.4B from operating cash flow and $1.3B in free cash flow. The company pays a little more than $4.5B in dividends per year. It means we could see a dividend growth policy slow down this year. We will follow the coming quarters with great attention.

Visa drives volume no matter what

Visa reported another solid quarter (what’s new?) with revenue up 9% and EPS up 25%. Payment’s volume increased 8% Y/Y in constant dollars with cross-border volume up 16% and processed transactions rising 9%. That compares with Q4 payments volume growth of 9%, cross-border volume growth of 16%, and processed transactions growth of 10%. While we expect the economy to slow down, it seems Visa continues to enjoy strong volumes.

My Entire Portfolio Updated for Q4 2023

Each quarter we run an exclusive report for Dividend Stocks Rock (DSR) members who subscribe to our very special additional service called DSR PRO. The PRO report includes a summary of each company’s earnings report for the period. We have been doing this for an entire year now and I wanted to share my own DSR PRO report for this portfolio. You can download the full PDF showing all the information about all my holdings. Results have been updated as of January 10th, 2024.

Download my portfolio Q3 2023 report.

Dividend Income: $53.43 CAD (-60% vs January 2023)

This is quite ironic that my dividend payment is down 60% vs last year, but my portfolio value is way higher (+32K or up 15%). That’s because I received my last dividends from Algonquin in early 2023 and sold my shares right after.

I guess that’s a good example of how you can improve your portfolio’s health by saying “no” to bad income!

Dividend growth (over the past 12 months):

- Granite: +3.10%

- Disney: a small parting gift ?

- Currency: +2%

Canadian Holding payouts: $35.20 CAD.

- Granite: $35.20

U.S. Holding payouts: $13.50 USD.

- Disney: $13.50

Total payouts: $53.43 CAD.

*I used a USD/CAD conversion rate of 1.3506

Since I started this portfolio in September 2017, I have received a total of $24,166.93 CAD in dividends. Keep in mind that this is a “pure dividend growth portfolio” as no capital can be added to this account other than retained and/or reinvested dividends. Therefore, all dividend growth is coming from the stocks and not from any additional capital being added to the account.

Final Thoughts

There will be a lot of information to digest in February and March as more earnings reports come in. Don’t make rash decisions. Often, stocks will move by 5-10% on earnings day. Trying to make a play on that day is playing against institutional traders who already have their trade instructions planned for many scenarios. By the time you read and analyze the new information, the trades have been accomplished way before you focus your eyes on your brokerage account.

It’s best to take a deep breath and read the reports a few days (or even a month!) after they come out.

Less stress = better decisions!

Cheers,

Mike.

The post Favorite Mid-Yielders – January Dividend Income Report appeared first on The Dividend Guy Blog.

Unveiling the Dynamics of Pipelines and Utilities: Pros, Cons, Best Stocks – Subsectors Series [Podcast]

February 14, 2024

AWR stock, BEP stock, Best Dividend stocks, best energy stocks, best pipeline stocks, best utility stocks, BIP stock, blog, EMA stock, enbridge stock, energy subsector, EPD stock, ET stock, FTS stock, Hydro One stock, Innergex stock, KMI stock, NEE stock, NEP stock, Pembina stock, pipeline canada, pipelines industry, pipelines subsector, Podcast, subsectors of energy, TRP stock, utility industries, utility subsectors, WEC stock, XEL stock

Subscribe

It’s one thing to know the 11 sectors, but it’s another to understand what each subsector does and how you can benefit from it as an investor. This first episode of our subsector series unveils the dynamics of pipelines and four industries of the utility sector. Learn about their pros and cons and the best dividend stocks.

Subscribe to our newsletter to receive our Get the Best of 6 Sectors issue.

You’ll Learn

- The Energy sector includes three main categories: Upstream, Midstream and Downstream. Mike explains the difference between them.

- We continue by summarizing the sector’s strengths and weaknesses, including a hedge against inflation and high volatility.

- For the episode, we focused on Oil & Gas Midstream, better known as pipelines. Why is this industry attractive?

- In which context do pipelines show a strong performance and when are they lagging the market?

- For years, Mike told us he did not like the energy sector except for pipelines. However, he sold the ones in his portfolio and the DSR portfolio models. Why is it so?

- Let’s now discuss our favorites in the subsector. In the Canadian market, we have Enbridge (ENB), TC Energy (TRP), and Pembina Pipeline(PPL.TO). Why are they worthy of mentioning?

- In the US, we can’t ignore Energy Transfer (ET), Enterprise Products Partners (EPD), and Kinder Morgan (KMI).

- Vero noticed that most pipelines have a PRO Rating and a Dividend Safety Score of 3 at Dividend Stocks Rock, including Mike’s picks. So then, how can we know they’re among the best choices?

- Let’s move to the utilities. In this case, we discuss various subsectors to understand their pros and cons. Simply put, utilities can be divided into regulated and non-regulated ones. But what’s the difference between them?

- When are utilities more prone to performance? And why has the market not embraced them much in recent years?

- Let’s discuss some stocks! In the Renewable Energy industry, Mike selected Brookfield Renewable (BEP), NextEra Energy (NEE), NextEra Energy Partners (NEP), and Innergex Renewable Energy (INE.TO). Mike describes them and tells why they’re among the best stocks.

- There are also many good options in the Regulated Electric industry, namely Hydro One (H.TO), Fortis (FTS), Emera (EMA), Xcel Energy (XEL), and WEC Energy Group (WEC). Of course, we all need power, but what else makes them attractive?

- An excellent example of the Regulated Water subsector would be American State Water (AWR). This Dividend King has a lot of acquisition potential.

- To end this episode, we also need to mention that there are diversified utilities. An example is Brookfield Infrastructure Partners (BIP). How would you analyze a diversified utility?

Related Content

For more details about the reasons why Mike sold Enbridge (ENB), watch the video below!

This episode hit our second-best record of all time. Don’t miss it!

Best Income Stocks 2024 – Part 2 [Podcast]

Subscribe

The Best Dividends to Your Inbox!

Download our Dividend Rock Star List now and do not miss out on the good stuff! Receive our Portfolio Workbook and weekly emails, including our latest podcast episode!

Follow Mike, The Dividend Guy, on:

- YouTube

Have Ideas?

If you have ideas for guests, topics for The Dividend Guy Blog podcast, or simply to say hello, then shoot me an email.

This podcast episode has been provided by Dividend Stocks Rock.

![]()

The post Unveiling the Dynamics of Pipelines and Utilities: Pros, Cons, Best Stocks – Subsectors Series [Podcast] appeared first on The Dividend Guy Blog.

© Copyright 2013 Adividend