WHY SHOULD I INVEST?

Before we even touch the topic of investing, I guess the most important thing to do is to understand why you should do it in the first place. I’ll be honest and blunt; investing in the stock market is not my favorite growth vehicle for my money. Yup, you read it right, there are tons of other way you can make your money grow and investing is just one of them. Personally, I rather use my money to grow my online business. This is usually the case with many entrepreneurs; the risk of investing in their own company is higher, but the reward is bigger. While investing, you should not expect returns of 30% per year for several years in a row. When you build a business, those numbers are easily achievable. Unfortunately, investing in a company isn’t a match on a very specific aspect of having money invested in the stock market; liquidity.

Are you liquid?

In your life, you will encounter people that have made a living off various investing vehicles. Some will swear solely in brick & mortars and will favors owning Real Estates stating it doesn’t lose in value. This statement isn’t true (remember the housing bubble in 2008) and still Real Estate investing isn’t liquid at all.

Others will invest in their career. I did this move for several years while I used my time and money to finance my CFP title, my MBA and my broker licence. Investing in my “employability” was a great move as I was independent and didn’t need to kneel in front of my employer. Still, investing in my career wasn’t putting money in a pot where I could dip in when I need cash.

My online income enabled me to travel across the world for a full year and it is now offering me a chance to live well without having to do the classic 9-5 rat race. Many companies have scalable models where constant effort of work is required, but the reward is growing exponentially. While my online income generates a constant flow of money each money, it is not as liquid as the stock market.

The biggest advantage of investing in the stock market is to be liquid. This liquidity is synonym of the flexibility you need, when you need it. I remember building a TFSA (tax free savings account in Canada) up to a few thousands before using it as an emergency fund to pay for car repair. If I needed to withdraw the same amount of money from the equity in my rental property or from my corporate account, it would have been quite a pain and have generated taxes in the latter.

The various purposes of investing

One of the biggest advantage of investing is to be able to set different accounts with the objectives of completing different goals. For example, I have a RESP account (Registered Educating Saving Plan in Canada) for my kids college education with a time horizon of 15 years. I also have a RRSP account (Registered Retirement Saving Plan in Canada) for my retirement with a time horizon of 50 years and a TFSA account as an emergency fund.

Each account is managed accordingly to achieves its purpose and nothing else. Each account follows a different investing strategies while still being connected to the big picture.

Investing in the stock market is probably the most flexible and useful vehicle to finance any projects. You can easily setup an investing account to finance your next trip to New Zealand, finance your children education or buy a rental property. The choice is yours.

What is important is not to put all your money in the same account and use it for various purposes. If you invested all your money in the stock market and you expected to use a part of this money as a cash down for your home next year, you may ended-up be buying a shack if you did this in early 2008. It is wiser to setup a money market account to save your money for short term goal instead of hoping for a good year to boost your return.

Another advantage of dividing your money into various accounts is to benefit from various account types. In both U.S. and Canada, the Government has setup different tax laws to meet various investing goals. For example, you can get a subsidy of 30% of your invested money if you open a RESP to finance your children education in Canada. The money can solely be used to this purpose but it is tax sheltered and comes with a strong benefit. My using advantages of each type of account, you maximise your investment returns without taking additional risk.

We all want to make more money and this is the reason why we invest. However, there is a time to be greedy and expect higher returns and there is a time to be conservative and be content of having cash aside. Answering the question “why you invest” will make you avoid this mistake. Instead of chasing returns, you should be chasing your goals and make them happen through disciplined investing.

Action of the day: define

Today’s action is quite easy and shouldn’t take much of your time. It is crucial you do it now before you continue your investing journey. Define why you invest. Write down your goals and separate them accordingly. Tell me, why do you invest?

I Buy Stocks at their 52 Weeks High, You Should Too

Summary:

#1 The stock market is breaking records highs almost on a weekly basis pushing many stocks to their 52 weeks high.

#2 Many investors avoid buying shares of those companies based in the fear their price will drop like a rock.

#3 I will show you that the 52 weeks high stats is completely useless and you should not use it at all.

Since 2009, we can tell the stock market has been running one of the most prolific bullish ride for decades. This phenomenon obviously pushes many company shares to their highest price of the past 52 weeks, or even to their highest price ever. For this singular reason, many investors prefer to wait until the stock price eventually drop. They are making a huge mistake. No matter what is happening with the stock market or the price of a particular stock you are following, you should enter the stock market without hesitation. This article will demonstrate that buying 52 weeks high trading stocks should not be ignored for this reason and that the fear of seeing the market drop because of the “gravity effect” is purely an invention.

Time in the market is stronger than market timing

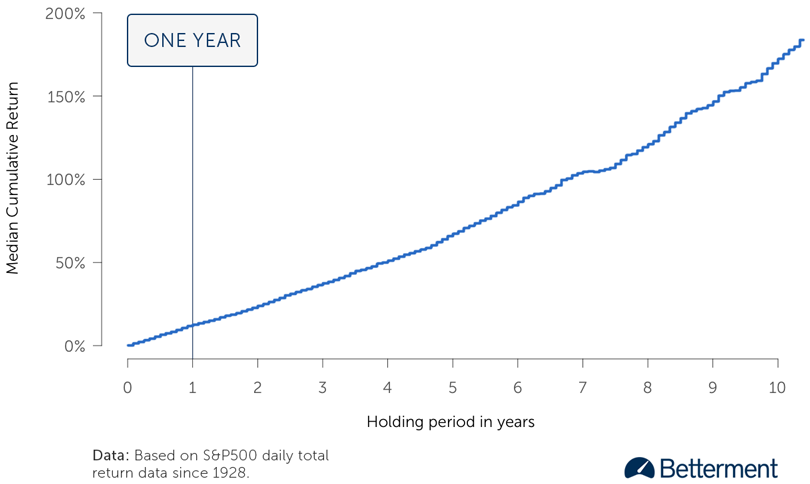

While of educated investors already know this thesis, many of them tend to forget how to apply it to their own portfolio on a regular basis. The longer you stay in the market, the better will become your investment return. But you don’t have to believe me, you only have to be able to read graphs of various financial studies. Let’s start with this one:

Source: Betterment

This graph shows the median cumulative return of the S&P 500 since 1928. It clearly shows that for any inventors who stays invested for more than 5 years, his expected return would dramatically increase year after year. In other words, if you invest, you should keep your money in for more than 5 years.

Okay, but how about buying when the market is low and stay the course then? Obviously, most investors will not argue by looking at the above mentioned graph. However, they will come up with the objection that currently, the market is over valued. That currently, this great company is overvalued. They rather wait until the next market drop and then enter for the long haul. Unfortunately, they decide to ignore another brutal graph:

Source: SchwabCenter for Financial Research (Investopedia)

This graph explains that if you miss the 30 top days in any trading years, you will most probably end-up in the red. Why? Because the market is going ups and downs but no one can really know when it will happen. Therefore, those who try to find the great entry point will most probably never find it.

How does those 2 graphs translate into portfolio management strategy? I’ve found two examples where I decided to buy stocks trading at their 52 weeks high.

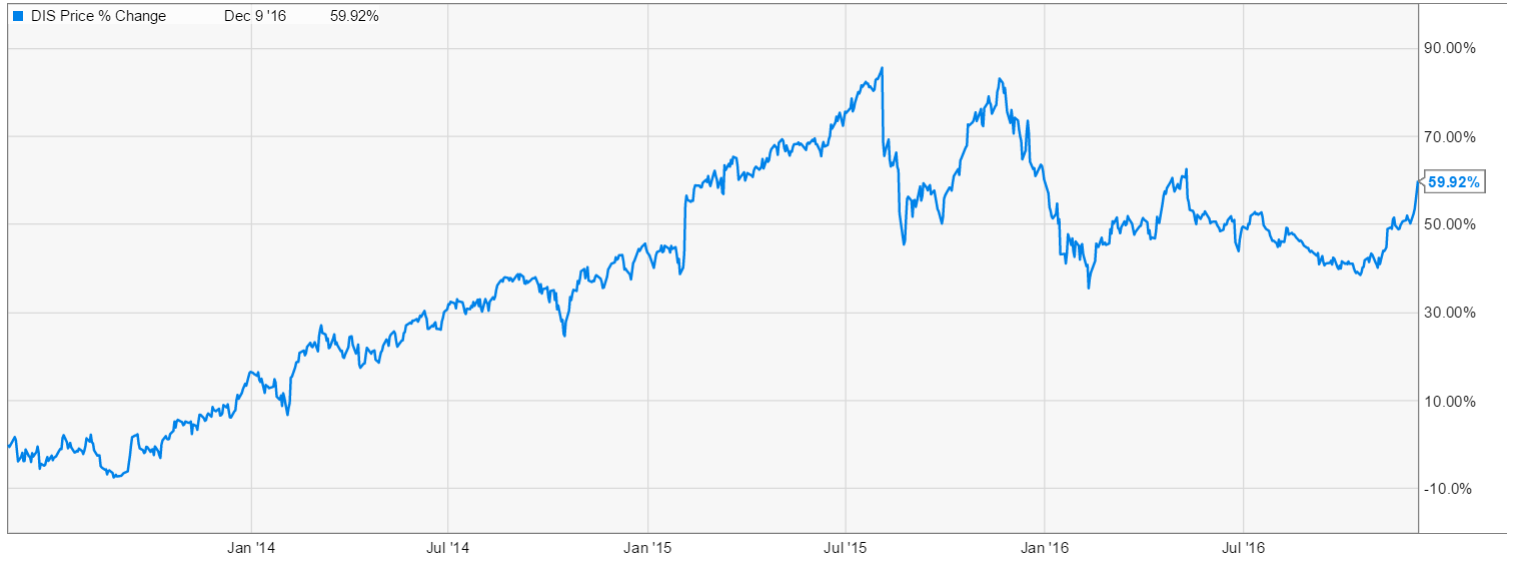

Example #1 Disney (DIS)

I purchased Disney in the middle of a very strong bull trend:

Source: Ycharts

*disclaimer: I bought DIS on May 22nd 2013.

Investment thesis at that time: DIS has become more than entertainment parks and Mickey. It is now the largest entertainment business in the world. Walt Disney is divided into five different segments: Media Networks, Parks and Resorts, Studio Entertainments, Consumer Products and Interactive. The Media division (ABC, The Disney Channel and ESPN) leads DIS revenue shares with 44% of the company total sales.

Disney divisions will benefit from the US consumers spending more, especially with the coming of the new Star Wars trilogy. Finally, Disney is the strongest brand for family entertainment and this competitive advantage is nearly impossible to replicate.

In fact, it was probably worst than buying DIS at its 52 weeks high, it was more like buying DIS at its 5 years high. A “rationale” investor would decided to wait for the next stock drop. Guess what… this investor is still waiting today:

Source: Ycharts

(stock capital gain since my purchase: 59.92%, dividend received: $4.97 per share for 7.59% of my purchase price ($65.49).

While Disney stock is currently going through a more difficult period since July 2015 (when ESPN concerns rose stronger), I’m still showing a very strong investment return of 67.51% over 3 years and a half for a CAGR of 15.88%.

Example #2 Lockheed Martin (LMT)

Similar to my Disney fairy-tale story, I bought shares of Lockheed Martin at their peak:

Source: Ycharts

*Disclaimer, I bought LMT on January 22nd 2014

Investment thesis: One of the reasons why I like LMT so much is that it barely evolves in a monopoly. They have obviously lots of competitors, but LMT has become THE defense company the U.S. government go to when it comes down for airplane firefighters for example. Lockheed Martin has done what BlackBerry did a few years ago by controlling the market. Fortunately for them, it is a lot harder to copy a F35 than a smartphone!

LMT clients are closely bond to them for several reasons. First, the trust between both the client and the company is quite important in this case. We are talking about military defense, you will not change your supplier in a heartbeat! Second, the switching cost for their clients would be incredibly high. Lockheed Martin benefits from several long-term contract guaranteeing a steady income flow. Those contracts are not easily broken. Plus, LMT owns a unique experience in military defense products and services.

Then again, looking at this graph doesn’t make any investors want to put its hard-earned money into a stock that has been skyrocketing for 5 years already. Remember the “gravity theory?”; it will go down sooner or later. Well, guess again:

Source: Ycharts

(stock capital gain since my purchase: 65.68%, dividend received: $18.41 per share for 11.82% of my purchase price ($155.76).

After almost 3 years, I’m already comfortably sitting on a 77.5% return for a CAGR of 21.08%.

But those two examples are not here to make me brag about my enlighten power of seeing through the future. I really can’t and I’m not smarter than most of you. However, I apply systematically the 7 principle of dividend growth investing to succeed in the stock market.

The dividend alone is a reason to buy now

The very first reason why you should not mind if a stock trading at its 52 weeks high or not is definitely the dividend payouts you leave behind. Even with a low dividend yield stock like DIS, I still earned a 2.11% CAGR investment return with its dividend payments (based on my cost of purchase). In the case of LMT, it’s even stronger with a CAGR of 3.79% over the past 3 years. Even if both stocks would have stagnated or go down, I would still earn money in the meantime.

If I had waiting on the sideline, I would not only have waited for ever because both stocks never went under their previous 52 weeks high (or barely), but I would have missed a significant amount of dividend paid. Money waiting in cash account doesn’t bring dividend.

What those 2 examples have in common; a strong investment thesis

Instead of spending hours trying to determine the value of a stock, I rather spend those hours on something a lot more productive: defining my investment thesis. A strong company will remain strong no matter what the market thinks about it momentarily. By spending more time on defining the reasons why a company should be part of your portfolio and what would be the worst-case scenario, you define the parameter of a successful trade. Even if you buy it “at a high price”, a long term holding approach will prove you right and will reward you with increasing dividend payments.

Disclaimer:

I’m long DIS & LMT

The opinions and the strategies of the author are not intended to ever be a recommendation to buy or sell a security. The strategy the author uses has worked for him and it is for you to decide if it could benefit your financial future. Please remember to do your own research and know your risk tolerance.

On The Road #16

As soon as I can, I’ll update you on my one year trip. I’ve decided to leave everything behind and spend real time with the people that matter the most in my life: my wife and three children. This is my story, I hope it will inspire you to create yours.

You can read my previous “On the road” articles:

- On the road #1

- On the road #2

- On the road #3

- On the road #4

- On the road #5

- On the road #6

- On the road #7

- On the road #8

- On the road #9

- On the road #10

- On the road #11

- On the road #12

- On the road #13

- On the road #14

- On the road #15

Date: from November 14th to December 1st

Countries/States/Province traveled through: Nicaragua

I’ve finally reached the “promised land”. After almost 6 months being on the road, we are now well established in a villa in Costa Rica for 3 months. Being here feels like being a millionaire. It’s great as I will have this feeling for the next 3 months!

But before, something very important happened in Nicaragua. Something I never suspected hit me. Nicaragua was a real game changer…

Nicaragua & their Volcano

Arriving in Nicaragua was a big relief. I wasn’t too keen on spending much time in El Salvador and crossing Honduras in a single day sounded like a very demanding challenge. Fortunately, we were now in Nicaragua, feeling safer than ever. Funny enough, fear is all in our head, nothing happened neither in El Salvador or Honduras.

We parked Freefall in a parking of a hotel called Playa Roca in Las Penitas. This was a really nice spot were we could have A/C (it was over 35 degrees everyday), access to wifi, a big rancho and a great beach right in front of us. There were also people from Quebec living in this village. They helped us doing our grocery (manoeuvring Freefall in the colonial city of Leon was a challenged as usual), washing our clothe and we visited 2 volcanoes with them (they had a small traveling agency).

The first volcano we visited was the Masaya. It was quite impressive as we were able to see lava inside the volcano. Being on top of this volcano staring at what would possibly kill us all if it erupts was quite impressive. The Lava was boiling and fuming.

While I enjoyed the Masaya, it was nothing compared to the Cerro Negro, one of the most active volcano in Nicaragua. This volcano doesn’t spit out lava, but only rocks. Over the years, it built a very nice slope where you can do… volcano boarding!

You climb up the volcano for about 45-60 minutes hike. The view was beautiful as you can see valleys and other volcanoes. Then, you dress-up like mechanics, take a piece of wood for a sleight and slide you way down the volcano at a very fast speed. Whoa! What a rush of adrenaline, this was crazy! The whole family did it (even Caleb who was registered as the youngest kid ever to climb up the Cerro Negro and slide it down with a sleigh!). I anticipated this moment for months and every second was worth it!

Mind the Gap Nica, Otto & a Tsunami

After a week spent nearby Leon, we wanted to explore a little bit more of Nicaragua and decided to stop further down south at a small hostel called Mind The Gap Nica, a recommendation from many travelers.

As I was getting there, I stuck Freefall in the sand thinking it was safe to park. Rapidly, a family nearby came to help us out and they pushed Freefall out of trouble. People in Nicaragua are very kind and very helpful! They were quite happy I shared my Corona’s with them

This is when the magic started operating. We finally reached Mind The Gap Nica, a small hostel for backpackers & surfers. As we enter in what appears to be the restaurant (and the officina at the same time), heavy music from Tool is playing. I automatically though: “nice… that’s my style! It’s good to hear good old music!”. A bunch of backpackers with dreads and tattoos warmly welcomed us. They were super happy to see us here and showed us around.

We weren’t sure we would stay here for several days thought. We thought that a family of five (especially our children) might annoy young adults (they were mostly all mid 20’s). As it is the case when a decision needs to be made and we are tired, we decided to wait until the next morning before we do anything. In fact, we have a special rule about decision making during our trip. Prior to taking any important decision, we must do 3 things:

- Eat

- Sleep

- Have sex

Don’t laugh! This is the best way to make sure your brain is well rested and can take the right decisions. The next morning, we noticed that all backbackers were pretty much excited to talk with our children. They really like what we were doing with our family and we started sharing traveling stories. The best of all is that there were 3 Quebecois there! It felt good to speak our tongue with other travelers!

We then stayed at this place for the remaining time we had in Nicaragua. For 10 days, the time clock stopped and we stared at the sea to think most of the time. It was an amazing moment of inner reflection about what I want in life. Was it all that quiet? Yeah… besides the fact that we got hit by a Tsunami and a Hurricane the very same day…

Yup, you read that right: on the same day, we had to face a Tsunami and Hurricane Otto. It started right after we had our lunch at our RV. We knew about Hurricane Otto, the first Hurricane in 100 years to hit Costa Rica & Nicaragua this late in November. It was coming most likely tonight and we knew which kind of damage a tropical storm (the Hurricane was expected to hit the Atlantic coast and then switch to a tropical storm with strong wind) could do. On the other side, we felt safe here as we knew the owners (Diego, Sam and Morgan) and we knew they will help us if anything happen to the RV during the storm. But then, Diego comes to our RV to advise us about a earthquake that just happened in front of El Salvador and that there was a tsunami warning. We decide to pack-up everything we have around the RV and get ready to leave in the event of an alarm. And there it goes! A strong siren started to echo all along the coast. Several Nicas were in their pick-ups screaming to people to jump-in. Diego yelled at us to leave NOW.

I jumped in my RV and started driving my way out of the dirt road as fast as I can. During the whole time, I had my eye fixed at my mirror to make sure I don’t see the gigantic wave about to swallow us. I was ready to make Freefall fly it needs be. I drove like this for a few miles until we reach the “safe point”. When then stopped there and watch the ocean to see the wave. Fortunately, nothing happened. The tsunami wasn’t that big and hit the coast about 30km north of where we were. We could all happily go back to camping spot and wait for the tropical storm to hit.

But instead of freaking out, we wrapped Freefall and we decided to have pasta & wine by the rancho and listen to the waves. The night passed, a little bit of rain and we were blessed; the storm hit Nicaragua about 75km south of where we were. Definitely, Mind The Gap Nica was the place to be!

After going through this very demanding day, I realised more than ever that life was short and I rather enjoy it fully instead of waiting to retire someday. Doing this trip is the best decision I ever taken in my life, but I now realise that I should never be afraid of anything else. I mean, what is scarier than driving down a mountain when you think your car will crash and burn or to face both a Tsunami and a Hurricane the same day? Am I afraid of losing my job or having to sell my house because I’m not making enough money when I come back? Seriously? This is what you call a fear? I was once afraid of things like that, now I know that if it isn’t life threatening, this is not a fear I should have. This is the magic that happened in Nicaragua; I’ve became invincible.

Now in Costa Rica!

We arrived in Costa Rica on December 1st. At 8:40 am, we finished crossing the borders and we took a picture:

Yes, we are now officially crossing border ninjas!

By the end of the day, we reached our villa, an ultimate goal during our trip. We have earned our rights to relax and enjoy Costa Rica for 3 months.

Beating the Market in 2016

Since 2012, I’ve initiated a tradition on this blog. Each year, I make a selection of 20 U.S. dividend growth companies and 10 Canadian ones. The goal is to build two portfolios of strong holdings that will beat the benchmarks. I’ve always used the same benchmark for the past four years:

VIG: Vanguard Dividend Appreciation ETF. VIG seeks to track the investment performance of the Dividend Achievers Select Index.

XDV: iShares Dow Jns Cnd Slct Dvdnd Indx Fnd. XDV seeks to provide long-term capital growth by replicating, to the extent possible, the performance of the Dow Jones Canada Select Dividend Index (the Index) through investments in the constituent issuers of such Index. The Index consists of 30 of the highest yielding, dividend-paying companies in the Dow Jones Canada Total Market Index.

I’ve selected both benchmarks because they are good and reliable examples of a dividend growth portfolio. If I wasn’t selecting my own stocks, I would probably buy thsse two ETFs to create a dividend portfolio.

Each year; I put myself to the test

Some people may think I put this list of stocks together the way you build your hockey pool for the season. Well it’s a little bit more complicated than that. I take about 2 months of research putting my information together and analyzing companies. Each company has to go through the 7 investing principles of dividend growth investing. These principles have been proven by several academic studies and tested through several years of investing. Then, I work on the selections to make a whole portfolio. It would be easy for me to aim at a specific industry and try to hit a home-run by selecting a sector as a whole. Instead, I’m doing my best to pick among various industries to make sure my selections as a whole could stand up as a portfolio. The idea is to show investors how they can successfully build a portfolio, anytime of the year.

By revealing and tracking my performance year after year, I put myself to the test. I think it’s important to be transparent and to show my readers how I’m doing. If not, what’s the point of reading my stuff right? For all that you know, I might be the worst investor in the world and you read about my theory… This is why I’m not afraid to share my findings with you and follow-up on my results.

I don’t expect to be right all the time. In fact, I’m quite surprised to see how often I’ve beaten the benchmarks since 2012. But what is important to me is to be transparent about how I select my picks and how they perform throughout the year. It’s a risk I’m willing to take ;-). My results are as at December 30th around 2pm (couldn’t wait for the market to close!).

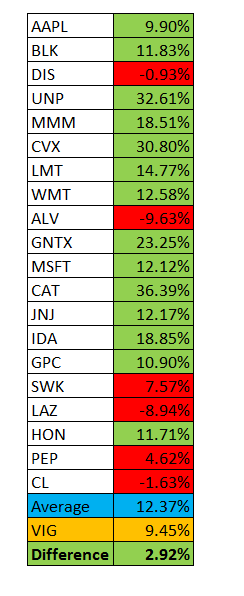

U.S. Best 2016 Dividend Stock Picks +12.37%

Source: Dividend Stocks Rock

As you can see, my portfolio shows a return of +12.37% which is 2.92% over the VIG performance and 2.92% over the S&P 500. 14 picks out of 20 beat the benchmark and only three companies show a negative return. We are not talking about one super flying stock improving the overall average, we are definitely talking about a solid portfolio, built to perform.

The key in this selection has probably been a few bold picks that severely unperformed in 2015. Companies such as Union Pacific (UNP), Chevron (CVX), Walmart (WMT), Caterpillar (CAT), Genuine Parts (GPC) all showed worse than -20% in 2015. I’ve looked at all of them and found that the market was overreacting for nothing. This is why they were part of my selections for 2016 and they have been doing quite well.

Disclaimer: We own 16 of these companies in our Dividend Stocks Rock portfolios. 9 out of 12 of our portfolios have beaten their benchmark since 2013. You can see our portfolio returns here.

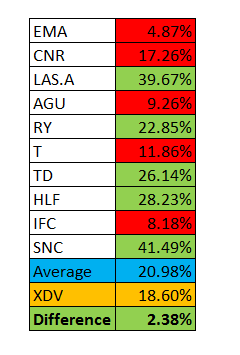

Canadian Best 2016 Dividend Stock Picks +20.98%

Source: Dividend Stocks Rock

I’m definitely proud of my performance on the Canadian market as I’m beating the XDV by 2.38% and even the S&P TSX by 3.26%. 5 out of 10 picks beat my benchmark and only one pick is showing a negative return. Here again, the great performance of this list is not solely due to a single pick. There are several great companies which performed well throughout 2016.

I must admit that selecting SNC Lavalin was a bit of a long shot, but I actually bought it for my personal portfolio for the same reason. I was convinced the engineering firm would do everything they could to avoid a trial and receive a 10 year ban penalty and it seems it will avoid it after all. Companies like Emera (EMA.TO), Telus (T.TO), Royal Bank (RY.TO) & TD Bank (TD.TO) continued to be solid as a rock. I also did a similar play as I did with UNP with Canadian National Railway (CNR.TO). I believe the beginning of 2016 was the right time to purchase railroads as they had suffered enough and they can only bounce back.

Disclaimer: We own 8 of these companies in our Dividend Stocks Rock portfolios. 9 out of 12 of our portfolios beat their benchmark since 2013. You can see our portfolio return here.

You Missed 2016 book? The 2017 is ready!

I’ve compiled a list of 20 dividend stocks to do well in the market for 2017. You just read about four of them, but there are still lots to discover in the book! The book includes the 20 dividend stock analysis plus 10 Canadian dividend stocks. That’s 82 pages worth of information for only $15.00 usd.

**BONUS** this year, you get the 2017 Best Stock Picks book + The Dividend Toolkit! **BONUS**

Click here to get your copy!

2017 Goals

This will be a crazy year…

2017 will not be like any other year, not for me anyway. As I’m writing my goals for 2017, I’m comfortably seated in a villa up in the mountain in the beautiful country of Costa Rica. A though crossed my mind the other day:

“For the next three month, I’ll be living in Costa Rica where I will wake up each morning on the top of the mountain, going to the beach whenever I want and explore this country like it’s my playground. For the next three month, I’ll be living like a millionaire”

Interesting enough, 8 years ago, when my partner and I founded our online incorporation, we called it M35. The meaning of this was to become millionaire by the age of 35. Today, I’m far from the iconic million-dollar net worth level. However, I’ve found a way to live like one for 12 months as I’m traveling the world and even more specifically for 3 months.

“If I can achieve such thing, I can achieve everything”

This was the second thing that crossed my mind that day. In fact, we all can achieve anything in life. The secret is to be dedicated to it. For this reason, my goals for 2017 will not be like the other years…

#1 Generate $20,000/month of online income

If you have been following me for a while, you know that my online income is already paying for my 1 year trip. Over the past 12 months, my online income jumped by 30% compared to 2015. My new goal now is to reach over 5 digits per month on a steady basis.

Don’t worry, this blog will not transform into a “make money online” blog. I intend to separate this venture with a completely different website while I continue to discuss investing on this blog.

Driven by my membership site, DividendStocksRock, I want to expand my horizon and fund more projects in order to create several money making machine.

#2 Start 2 Monthly Saving Plans

Once I reach my online income goal, I want to start saving $1,000 per month. This money will go in a TFSA account. It will be 100% invested in dividend stocks. My second savings plan will go for college. My oldest son will go to private school in 2017 and I need to start thinking about my three kids’ future. I already have closed to $13,000 invested for them, I’d like to be able to add a $500 per month plan by the end of the year.

#3 Pay $1,000/month worth of debt + clear my line of credit

In addition to my regular payment, I want to accelerate my debt repayment structure. Once I get back home in July, I want to start paying down my debts faster as I’m looking to reach financial freedom earlier. I want to setup the debt repayment plan + I want to clear a $19,000 line of credit by the end of 2017.

#4 Play Soccer in a league

Goal setting is not only about money. For 2017, I want to play in a soccer league. I’m not the best player around, but I truly enjoy this sport. I feel I can go beyond my capacities and improve myself. It also helps me getting out of my comfort zone.

#5 Weight 170 pounds

While traveling, I’ve reduced my eating habits. I LOVE eating and I definitely eat too much. However, as resources are not always easy to find, I’ve changed my eating habits already. I have no clue how much I weight right now, but I was around 185 lbs before I left. My goal is to go down to 170 pounds (I’m 5’9’’). I already have a good habit of running each morning, all I needed to do was to stop eating twice what I should ;-).

#6 Give $5,000 to charity

I would like to be able to give more to charity this year. I’m thinking jumping my contribution to $5,000 this year and increase it year after year. For this year, I will donate this money to kids related foundation, maybe 2-3 of them. Kids are our future, it’s important they all have equal chances to succeed.

Goal Setting is Fun, but there is more to it

I know you will be reading at least a dozen of bloggers telling you about their goals in 2017. This is the time of the year right? But what about the rest of the year? When I first wrote this article, I’ve setup “realistic” goals such as making a 30% jump in my online income (which I did last year), and starting savings plans around $250/month and $25 for my kids or paying down my debts by $500/month without clearing my line of credit.

Then, I looked back at my goals before hitting the “publish button” and I remembered something I read not so long ago in the 4 hour workweek by Tim Ferris (love this book, this is my second time reading it). Tim tells us that realistic goals are often no achieved as it doesn’t drive enough motivation. We don’t have to go the extra miles or think the unthinkable to achieve them. This is why we fail so many times.

This is why I’ve decided to erase my previous number and replace them by ridiculously large numbers. This way, I have no other choice but to commit to them and think how I can reach those “crazy” goals. Let’s crush 2017 instead of simply making it a good year.

© Copyright 2013 Adividend