How to Invest a Lumpsum Amount of Money in an All-Time High Stock Market

Between 2009 and 2017, the market went up on one of the most amazing streak:

Source: Ycharts

As you can see, for an investor waiting on the side lines, he had 2 very little opportunities (one in 2011 and one in 2015-2016) to enter the market during a plateau. Even then, the best timing to enter the market has always been today and the worst has always been tomorrow. This article will go in-depth to explain you why and how to invest an important amount of money in today’s stock market.

Still, the question of timing to invest your money is being recurrent among all investors. The reason is quite simple, nobody wants to invest in a stock market that will go bust the next morning:

Source: Ycharts

Are you willing to lose 35% of your money in 6 months just because the “right timing is now”? I totally understand you would not. We are all afraid to lose money when we are about to invest a big amount.

If you want to invest a massive amount of money and you are paralysed by the fact the market is too high, there is a solution. Just keep reading…

The market is a dangerous place

“Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.”

– Paul Samuelson

As I just mentioned, nobody wants to invest right before a bear market or worse, a market crash. This thought alone can paralyse your money for months, read years. When you get your eyes stuck on the screen, the market can become a dangerous place. However, one must first remember he doesn’t invest for the next 3 to 6 months. An investor should think about the next 30 to 60 years. This is why we should look at a graph with perspective, like this one:

Source: Ycharts

Lesson learned from this graph: the stock market always go back up. This graph covers pretty much all catastrophes an investor could live in his life. After the techno bubble and a credit crunch, the stock market is still averaging around 10% annualized returned over the past 30 years. I hope you have realized that I’m using total return in all my graph as dividend growth investing is the backbone of my investing strategy.

When you are in for the long haul, how the stock market will react in a few months should not worry you. The certainty you need is that the stock market always go back up. If you are not in for the long haul, then maybe investing in the stock market is not for you.

Unfortunately, being in for the long haul, is highly profitable, but incredibly boring…

The market is at its all-time high – how do I invest?

“The four most dangerous words in investing are: ‘this time it’s different.’”

– Sir John Templeton

Now that we have agreed that the stock market will reward its patient shareholders, investing when the market is at an all-time high is still not easy. Chances of making investment mistakes in 2017 are greater than making one in 2009 for example. This is mainly because we have been riding a 8 years long bull market. In fact, I could have given 100K to my 11 year old son in 2009 and he would have made money. I’m not too sure I would trust him to make investment decision in 2017.

The thing with a strong bull market is that it hides many bad companies. It like the ocean high tide; everything, good or bad, is being lift up to the top. Now, you have money to invest and you surely don’t want to pick-up someone else’s garbage.

On the other side, the only worse decision than picking bad stocks would be to not pick any at all. How’s your money market fund did between 2009 and 2017? What can save you is a strong investing process. With a well-defined stock picking methodology, you can start building a new portfolio today and invest a lot of money without being stressed even if you start in a all-time high market. The methodology presented above has been based on decades of academic studies and based on my own experience.

Don’t expect the market to be different this time. It will go down, and will bounce back. The only thing we don’t know is when. By using a stock selection process rigorously, you can start investing today, even if “today” the market is high. The following process will help you doing it the right companies and avoid picking bad ones.

#1 General metrics to filter down your research

“An investment in knowledge pays the best interest.”

– Benjamin Franklin

It is virtually impossible to screen the entire market and look at every single dividend paying stock for a single investor. This is why stock filters have been invented. But then again, with a complete access to all kind of data, the number of searches and theories on fundamentals are endless. How could you select efficiently a smaller bag of companies without losing all your time playing around with you filters? ‘Cause trust me, you can spend months playing around with fundamentals without picking a single stock.

I personally like to keep things simple. I don’t go too far with playing with stock filters as I believe numbers are only one part of the answer. In fact, no matter how great numbers a company could show, it only shows what it did previously, not what it will post in the future.

I have a few variations of filters, but it usually goes along the following lines:

- 50% < Dividend Yield (TTM) < 5.00%

- 01% < Dividend Per Share (5 Year Growth) <

- 01% < Dividend Per Share (3 Year Growth) <

- 01% < EPS Diluted (5 Year Growth) <

- 01% < Revenue (5 Year Growth) <

- 01% < Revenue (3 Year Growth) <

- 00% < Payout Ratio (TTM) < 100.0%

- 00% < Cash Dividend Payout Ratio (TTM) < 150.00%

I use the powerful stock screener provided by Ycharts. It helps me getting into details fairly quickly. Those filters are applied to both Canadian and US market. It will provide between 250 and 300 searches. While this makes a huge basket of stocks to pick from, I like to have variety!

Those metrics enables me to select companies with crucial trends for dividend growth investors; growing revenues and earnings. It all comes down to this: if a company doesn’t grow their revenues, it can’t grow their earnings. And if it can’t grow its earnings, well, what do you think will happen to the dividend payment?

Payout ratios and cash payout ratios are used to determine if the company is about to suspend its dividend raise or if there is still room for management to keep being generous. After all, the power of compounding dividend lies within consecutive payment hikes.

A while back, I used to select companies paying over 2%, but I tend to give a quick look at lower yielders now. I’ve found gem such as Apple (AAPL), Disney (DIS) and Canadian National Railways (CNR.TO or CNI) by opening my search a little. I also rarely consider companies paying over 5% yield. They are usually in danger… especially when you are at a all-time high on the market. Why in the world a company would pay over 5% yield when interest are at their lowest and valuation is at the highest? There is only one answer to this question: because the company and its dividends are in great danger. Remember I told you that high tides bring everything up? Most 5%+ yielders are garbage.

Such filter will bring about 250 to 300 stocks on the table. This is too much for any kind of portfolio. Keep in minds that even professional portfolio manager with a complete team of analysts owns about 40 stock per portfolio. Once this first filter is done, you can start by looking at each component individually and consider the stronger dividend growth stocks or the higher yield, depending on what you are looking for.

I personally try to find a balance between revenue, earnings and dividend growth metrics. If the three metrics are growing accordingly, then, I know the management has similar objectives than mine: increasing my quarterly pay checks. I don’t give much importance to dividend yield for the reasons explained above. I rather focus on future growth instead.

To finalize my search, I usually filter those results and try to find companies showing good numbers in all metrics. This is how I usually narrow down “my stock universe” to about 100 companies. At Dividend Stocks Rock, this is about the number of companies we follow.

#2 Test the dividend sustainability

“How many millionaires do you know who have become wealthy by investing in savings accounts? I rest my case.”

– Robert G. Allen

The next step of selection is all about dividend growing payments. There is no point of investing in dividend stocks if there isn’t growth. Why? Because inflation will eat-up your dividend checks if they don’t grow accordingly!

To do so, I like combining the dividend payment with payout ratio and cash payout ratio on a 10 year history graph:

Source: Ycharts

This is 3M (MMM) graph from 2007 to 2017. As you can see, dividend payment has been consistently raising and so the cash payout and payout ratios. There are three observations to make from this graph;

- #1 The company is seriously committed to increase dividend payouts

- #2 Management benefit from lots of room for future increase (payout ratios around 50%)

- #3 It will be impossible for the company to maintain the aggressive dividend hike policy it has since 2014 as the payout ratios are rising just as fast as the dividend.

Testing dividend sustainability enables me to make sure that the company you are about to select for your portfolio will continue increasing its dividend in the future. If payouts ratios are around 90% or more, then, it’s time to ask yourself serious questions about the future dividend payment. If you can answer how the company can control this situation and increase their earnings in the future, there is no problem at selecting a higher payout ratio stock. However, if you are uncertain about how earnings could rise in the next 5 years, then you have little hope to see steady or significant dividend raise. You must remember that management will not throw away important cash flow to shareholders if this hurt the company’s balance sheet. If they do, this is just another reason to not pick up this stock!

#3 Define the business model and advantage

“The individual investor should act consistently as an investor and not as a speculator.”

– Ben Graham

Once you have played enough with fundamentals, it’s time to look forward into the future. This Jedi skill can be learn with a simple process: define the company business model and highly their main strengths.

In general, the company business model will tell you how numbers will go facing a recession or riding a strong economy. It is also very important to understand how the company makes money before you buy its shares. For example, I don’t know much about the mining industry and how they figure the future price of their commodity. For this reason, I’m staying away from such companies (plus, they are usually bad dividend payer anyway!).

On the other side, I completely understand how Disney (DIS) makes money. They sell entertainment and dream for all family members. Over the years, they have built a strong model where they can first make money from movies (Star Wars, Marvel’s, Frozen, etc) and then, create an incredible variety of money drivers (through their theme parks, toys, cruises, clothes, etc). Their main strength resides on their ability to create near to infinite cross selling opportunities with a single product. They have the marketing budget and the experience to establish efficient strategies making almost every movie a billion dollar industry by itself.

Once I clearly understood what Disney business model is about, I can understand how the company will evolve in all kind of economic situation. Can Disney exist in 50 years from now? Can it continue paying an increasing dividend? What possible catastrophe could affect Disney over a long period?

#4 Write down your investment thesis

“Know what you own, and know why you own it.”

– Peter Lynch

Writing down your investment thesis is the most important part of any investing process per my opinion. Funny enough, this is also the most overlooked part by many investors. I know, writing down stuff makes you work and takes additional time. But this is a crucial step that will make you a lot of money, and most importantly, will make you save lots of money as well. Why? Because defining the reason to buy a stock will, by default, determine the reason to sell it as well.

For example, I used to own Wal-Mart (WMT) in my portfolio. My investment thesis at the time of the purchase was the following:

Wal-Mart is a leader in retail stores. The company manages stores across the world and benefits from geographic diversification. Management has built a strong brand name and WMT sizes enables substantial economic scales making it very hard for competitions. Since WMT sells “everyday stuff”, they are not at risk during a recession as their base of costumers will continue to make basic purchases. The company is now moving lots of capital to build a strong and reliable e-commerce site. I believe the future of WMT will go through internet sales. Their experience in brick-&-mortar stores and selling goods should be enough to conquer this new playground. The company shows steady revenue and earnings growth. Finally, WMT is a dividend aristocrat showing over 25 years of dividend increase.

Now, what has made me sell WMT? It does sound a buy-hold-forever stock right? The thing is that Wal-Mart failed at one key element of my investment thesis; after several years, they are still a minor player in the online commerce industry leaving Amazon (AMZN) setting the rules on this new playground. WMT didn’t cut or suspend its dividend growth, but I don’t see in 5-10 years from now how management will be able to increase their dividend. Since WMT doesn’t meet my investment thesis, I sold the stock in 2016. This is as easy and simple as that.

I am very well aware I might be wrong in my investment thesis. The purpose of writing it down it not to be flawless. The purpose is to know why you buy a stock so you can sell it and move along quicker if it fails you. This avoids having everlasting doubts paralyzing your money for months or years.

#5 Determine the right valuation

“The stock market is filled with individuals who know the price of everything, but the value of nothing.”

– Phillip Fisher

Ah! After many hours of research, you finally find the exceptional company you were looking for. But before you pull the trigger and buy 100 shares of it, the question that kills:

Is this stock overvalued?

The answer to this question is very hard to give, especially when the market is trading at a all-time high. However, my short answer to this question is quite simple. If you have found an exceptional company, today is the best timing to buy it and tomorrow is the worst one. I know you will probably won’t bite this as most investors prefer finding a complete process to assess the value of a share. The reason why I use a valuation process is mainly to determine what is the best buy among my short list of exceptional companies. I use a simple two step valuation process.

The first step is to look at the company’s PE ratio history of the past 10 years. Over a 10 years history, you usually get how a company’s valuation by the market evolves through a complete economic cycle (facing both recession and strong growth periods). Here’s 3M (MMM) PE historical graph:

Source: Ycharts

At first sight, we can see that MMM has rarely been trading at such high PE ratio. It seems that the company is overvalued right now. Probably that investors are willing to pay a premium for a strong dividend growth company in an uncertain environment.

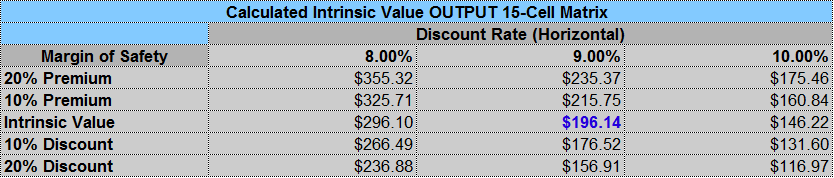

Then, I use a double step dividend discount model (DDM). The DDM gives me the fair value of a company considering solely its future dividend payment capacity. By using a two-step model, I’m able to use a dividend growth rate for the first 10 years, which would reflect the company current situation and near future and a terminal dividend growth rate usually reflecting a more conservative growth rate for the long haul. Here’s what it looks like:

As you can see, at the moment of writing this article, MMM seems slightly undervalued (current market price at the time of calculation was $189). I give more value to the DDM as I’m after the dividend payment when I invest my money. If the company met the rest of my investing process, this could be a strong candidate to my portfolio.

Here’s your next step

While this article is a good introduction on the topic, you may be left with questions such as:

- How do I build a whole portfolio?

- What about asset allocation?

- Are there safer dividend stocks than others?

- How do you find the dividend growth rate and the discount rate for the DDM?

Don’t worry, I’m not leaving you hanging there. I’ve wrote a complete book on building your dividend growth portfolio. The best thing is that it’s free!

This book went from 30 some pages to 135 master-class manuscript

You can now download 30 Days to Dividend Growth Investing, the second edition of my original book; Dividend Investing – How to Build a Money Making Machine. I’ve reviewed the entire book to create a unique resources that will help you building your portfolio step-by-step or improving your trading technique.

Finally, don’t forget this famous quote from Peter Lynch;

“You get recessions, you have stock market declines. If you don’t understand that’s going to happen, then you’re not ready, you won’t do well in the markets.”

– Peter Lynch

Disclaimer: I own shares of DIS, MMM, CNI.

On the Road #19 Deep Dished in Nicaragua

As soon as I can, I’ll update you on my one year trip. I’ve decided to leave everything behind and spend real time with the people that matter the most in my life: my wife and three children. This is my story, I hope it will inspire you to create yours.

You can read my previous “On the road” articles:

- On the road #1

- On the road #2

- On the road #3

- On the road #4

- On the road #5

- On the road #6

- On the road #7

- On the road #8

- On the road #9

- On the road #10

- On the road #11

- On the road #12

- On the road #13

- On the road #14

- On the road #15

- On the road #16

- On the road #17

- On the road #18

Date: from February 26th to March 6th

Countries/States/Province traveled through: Nicaragua

Interesting enough, we’ve only been on the road for 8 days and I already have the feeling I need to share this with you. It is because we have experienced many incredible adventures in a very short time. Is it because we have become travel gurus? Or is luck? Or is it just destiny sending a bunch adventures towards our way because we deeply wanted to go back on the road? I don’t know what it is, but I can tell you one thing, this time, we got deep dished in Nicaragua. I always liked this expression coming from the famous crust pizza you can find in Chicago. We have reached the heart of this country!

But first, a few words about our departure

Leaving the house in Costa Rica wasn’t easy. A few days before we left, we were anxious to get back into Freefall for this last chapter of our trip. After 3 months, we had built a life in another country. We knew firsthand the farmer from whom we bought our fruit and vegetables, our cleaning lady, Vilma, was in love with Caleb, I made friends at Mono Congo, my office 3 days a week and we just felt at home back in the villa after each hike or day at the beach.

We were lucky enough to visit friends at their place near Tamarindo the day before we crossed the border. We didn’t know them very well (they were soccer friends), but it felt really good to enjoy a nice dinner with people we knew before going it alone for another 3 and a half months. Looking at Eric made me remember that I should do the same; this guy has 30 projects going on at the same time. He basically has dozens of money making projects… No wonder he is building 2 houses in Costa Rica at the moment! Hahaha!

After this nice encounter, we slept in a Finca very close to the border. I was darn nervous to get through the endless bureaucratic circuses… The day of our departure, at 5:15 I was up, at 5:30 we left the Finca and we finished crossing the border at 7:20. We haven’t loss our ninja touch for border crossings!

Deep Dished into Nicaragua

While we travelled, we made a lot of friends both on the road and on Facebook. Another traveller that we had never met before referred us to a family in the small village of San Juan de Oriente. They were friends for many years and the family was kind enough to welcome us to their little pueblo.

One thing to understand is that these guys grow up very close to each other. Therefore, we had met so many people during the next 3 days; I’m not sure who the brother of whom is and who are the cousin or aunts we met. Still, everybody in the whole family was incredibly welcoming.

We parked the car in front a school near a park with free Wi-Fi. A very clever idea the government had; they offer Wi-Fi in most children’s parks across the country! This is where we slept for 3 days.

We started our day by having a walking guided tour by one cousin (I think?!?) of the family. As we arrived early than expected, Raina and her husband Herby weren’t there yet. We then walked across this beautiful pueblo with sculptures of Mayan Gods everywhere. The village was situated close to the Lagon the Apoyo. Caleb called it the Lagon of Pollo the whole time ;-). We took a short walk to the mirador to admire a great view.

When we came back to the village, we followed Raina to her house. Very modest, she told us before we entered her house that her family wasn’t rich… in fact they were very poor. Third-world country poor. The house isn’t a house. It’s just a bloc of concrete with no windows and a metal roof. Don’t ask where the kitchen or the living room is; the kitchen is outside right beside a fire pit and the living room is simply the outside the house, covered by the same roof. We sat down on a wooden bench and started chatting. Spanish immersion big time! The even offered to share their lunch with us. Typical rice & beans meal. The kids didn’t say a word; I was quite impressed how they had reacted. They even went to watch TV with Raina’s little girl in their home.

We spent the rest of the afternoon with Raina and her family before going back to the park and let the kids play with other Nica’s. Our children were quite “popular”, it was fun to see how quickly they became integrated! Raina and her husband joined us for an evening tour of the village up to the mirador where we can see the city of Granada on the other side of the Lagun Apoyo. This Lagun is actually a volcano that has been sleeping for hundreds of years and now covered by the cleanest water in Nicaragua.

The next morning, we woke up early as Amy was sick at 5am. She hadn’t been feeling well for 2 days and we decided that I would go with the boys to explore the Lagun Apoyo while the girls would stay in the RV to rest. We hadn’t been sick during the trip so far, save for a few stomach bugs and vomit episodes that is just part of the game.

We were lucky enough that Herby joined us in our hikes. He showed us an ancient path taken by the Mayas. There were many sculptures along the way of different gods. Once we got to the Lagun, we went for a swim while Herby’s family came to join us and cooked a delicious meal on the beach. For once, we were one of the locals hanging out and not just tourists passing by J. Then, we had lots of fun riding in the box of an old pick-up truck until the car could no longer climb up the hill. Raina’s brother was playing with his motor. I was quite surprised to see how they manage any mechanic trouble with just a few tools! After 30 minutes of trial and error, we were back on the road again!

I was relieved to find Amy looking a lot better upon our return. We went to play in the park again and our plans to see Granada the next day were still on. The next morning, we left early to explore the city. Granada is a nice colonial town. It is not my favorite, but I think I have become spoiled by traveling so much, hahaha! We walked around and took many pictures of the architecture. Then, we did the other thing we enjoy most when traveling in cities; eating at different restaurants! Hahaha!

We spent 3 great days with Raina’s family. We were touched by their generosity. Unfortunately, we had to leave them on a series of unfortunate events. During our last night, Amy started to feel sick again. She had fever and Advil couldn’t help to drop the temperature. Early in the morning, Raina knocks on our door to say goodbye as they had to leave for the hospital for her mother. At that time, Amy still had a fever and Caleb started not to feel well. This was total panic in the RV with two kids having a fever! At home, this wouldn’t have been a big deal. We would just wait 48 hours and go to the clinic if need be. But when your children are sick in a third-world country, we are facing a whole new different challenge. I left for the farmacia while my wife was searching for help among her Facebook friends. We were lucky enough to know a few doctors, nurses and pharmacists among our friends. They all told us to wait and keep them hydrated. We then decided to leave for Somoto anyway, thinking we would be close to Esteli, where there is an hospital if anything went south.

Then again, we were welcomed by Fausto, a guide for the Somoto Canyon and his family. They were very welcoming and even offered medicine for our children. The fever was under control and by the next morning, both kids were feeling better. We decided to stay one more day as we wanted to do the Canyon, but we couldn’t do it with weakened kids! During this day, we met with another family traveling with 3 kids (so cool!) in a pick-up truck with a tent (okay… they are far more adventurous than we are!). Drietz and Karoline are from Belgium. They have been travelling through North and Central America like us for a while. It was nice to chat with them while our children were recovering. That night, all the children were feeling well on our side and they got invited to celebrate the birthday of a little girl in Fausto’s family. They enjoyed the piñata, cake and even dancing! Once again, I felt blessed to live these previous moments with my family.

Exploring the canyon was something to remember! We did the big tour which is about 11km of walking and swimming through the canyon! It felt a little bit like the Narrows in Zion, but with the option of swimming for a good part of it. The kids loved it as we explored the canyon with the other family as well.

We spent the night chatting with Drietz and Karoline and other travellers that had just arrived there while we were hiking. In order to thank the Fausto family, we gave them 2 soccer balls. One kid even asked us to sign the ball as he was super happy. It’s a great thing we brought these balls to give away a little bit everywhere in Central America!

So here we are now, after a beautiful week in Nicaragua, we hit the road the next morning for what is expected to be the toughest day on the road: crossing Honduras in one day and finish our ride on the beach in El Salvador. I’ll tell you how it went in my next on the road!

14 New Canadian Dividend Aristocrats!

Life is good for Canadian dividend growth investors as 14 companies made the cut to be added to the Canadian dividend aristocrats.

To be considered an S&P Canadian Dividend Aristocrat, the company must have increased its dividend payout every year for five years but have a free pass and is still eligible if the company maintains the same dividend payout for a maximum of 2 years. Therefore, we are looking at stocks that have a good potential for raising its dividend but still pretty far away from 25 consecutive years as it is the minimum requirement for U.S. aristocrats.

Here’s a Complete List of Canadian Aristocrats Rules:

- The company’s security is a common stock or income trust listed on the Toronto Stock Exchange and a constituent of the S&P Canada BMI.

- The security has increased ordinary cash dividends every year for five years, but can maintain the same dividend for a maximum of two consecutive years within that five year period.

- The float-adjusted market capitalization of the security, at the time of the review, must be at least C$ 300 million.

- For index additions, the company must have increased dividend in the first year of the prior five years of review for dividend growth. This rule does not apply for current index constituents.

Here are the new additions:

Aecon Group (ARE.TO)

Aecon Group Inc. is Canada’s largest publicly traded construction company, providing a range of services to private and public sector clients (roughly 50/50) across its three core segments of Infrastructure, Energy, and Mining.

Aecon is a pure Canadian play if you are looking to invest in Canada’s infrastructure. As the Liberal government promise, we expect lots of billions to be spent in this industry in the upcoming 10 years.

Allied Properties REIT (AP.UN.TO)

You will see may REITs in this new aristocrats’ update. Allied Properties concentrate their effort in urban office environments across major Canadian Cities. The company currently owns 155 properties spread across downtowns of cities such as Toronto, Calgary, Vancouver and Montreal. Allied is growing through acquisition but remain attractive with a low 37.5% debt / total assets.

AltaGas (ALA.TO)

AltaGas Ltd.’s is a North American diversified energy infrastructure business with a focus on owning and operating assets to provide clean and affordable energy to its customers. Their purpose is to stock energy during excess period and offer it when the market requires additional power. AltaGas has grown its asset base to over $10 billion from just $3 billion at the end of 2010.

Bank of Montreal (BMO.TO)

After the 2008 crisis, there was a pause in paying dividend for all banks. Since then, they all have been back to their previous policy: double dividend hike each year. BMO is the latest bank to get back on the Aristocrat list.

Boardwalk REIT (BEI.UN.TO)

Boardwalk REIT is a multi-residential rental landlord that owns and operates apartment buildings in Canada. While BEI.UN is mainly concentrated in Alberta, it is the second largest REIT in term of units (200 properties for 33,000 units) and market capitalization. Edmonton and Calgary are showing over 50% of all unites managed. No wonder their revenue fell in the past couple of years. Still, the company seems to manage well through this challenging environment. This could be a nice addition with a dividend yield close to 5%.

Brookfield Asset Management (BAM.A.TO)

Brookfield is an alternative asset manager with over 100 years of operation. They manage $250 billions across more than 30 countries. What are alternative assets? BAM manages 4 divisions: Real Estate, Infrastructure, Renewable Energy and Private Equity. Those are interesting sectors if you are looking to diversify your portfolio in other types of industries.

CAN Apartment Prop REIT (CAR.UN.TO)

Canadian Apartment Properties REIT owns apartments, townhouses, and land-lease communities in or near major urban centres in Canada. It now has around 48,000 units across the country. Interesting fact 50% of its properties are in Ontario and only 6% in Alberta. In other words, this company will not suffer from the gas price shock. The company shows a strong profile and a solid dividend yield near 4%.

First Capital Realty (FCR.TO)

First Capital manages shopping center in Canada. They own 160 properties representing a $23.8 million gross leasable area. The company focuses on growth with over 14M square feet in development worth over $1 billion over the next several years. The business is well spread across the country with 34% of its portfolio in Western Canada, 42% in Central and 24% in Eastern Canada.

Intertape Polymer Group (ITP.TO)

Intertape Polymer makes one of my favorite product for RVing…. Duct Tape! But the company is more than making this famous product, it also manufactures all other kinds of packaging tapes and materials. The company is celebrating 100 years of history and is poised for a long life if we look at how revenues are growing for the past 5 years!

Loblaw (L.TO)

Loblaw is the largest food retail in Canada with over 2,400 stores and 70,000 million square feet of store space to feed Canadians. One of the major strength is Loblaw ability to create #1 and #2 private labelled brand in Canada with President’s Choice and No Name. Private Label brands are more profitable for stores and drive margins up. Loblaw also owns Shoppers Drugs giving them opportunities in the drug market.

North West Co (NWC.TO)

While most companies focused on urban area, North West is doing the opposite. It specializes in opening retail stores in underserved rural communities. While they are present in Canada, they also have stores in Alaska, South Pacific islands and the Caribbean. They basically operate small stores in small places leaving the competition to none. Interesting business model, and obviously successful when you look at how earnings and growth went up over the past 5 years.

Pembina Pipeline (PPL.TO)

Pembina is one of western Canada’s largest transporters of liquids, carrying approximately 50% of Alberta’s conventional crude oil and 30% of western Canada’s natural gas liquids production. As many plants continue their production, PBA benefits from a steady cash flow to support its dividend during the crisis.

Stantec (STN.TO)

While we often hear about SNC Lavalin (SNC.TO) and WSP Global (WSP.TO), Stantec is another very important engineer firm with over 22,000 employees working in 400 locations across the world. Stantec is expected to benefit from major investment in infrastructure from both Canadian and U.S. Government in the upcoming years.

Weston (WN.TO)

Weston is selling more than bread. In fact, it remains in control of Loblaw (L) and Shoppers Drug Mart. Weston Foods is the largest Canadian baker. As it wasn’t enough, Weston also controls one of the Canada’s largest REITs; Choice properties REITs (guess which stores is their biggest renter?). One way or another, if you are Canadian, you do buy something from Weston each week!

My Favorite New Aristocrats?

If I had to put a dollar in a new aristocrat this year, I think it would be in Brookfield Asset Management. This investment would mainly to profit from alternative assets which are not always easy accessible for investors. I also appreciate Loblaw and Weston but their dividend yield is not incredibly high for income seeking investors.

What about you? What is your favorite new aristocrats?

Disclaimer: We own BMO and BEI.UN.TO in our Dividend Stocks Rock Portfolio.

The Price You Pay Doesn’t Matter

Not too long ago, I wrote an article on Seeking Alpha about selling General Electric (GE) before it fails investors again. I knew there are lots of GE shareholders and I expected to get thrown my fair share of tomatoes. After all, we have all our reasons to hold share of one company instead of another and someone telling you it’s a bad idea may hit the wrong button.

There was something very surprising in the comments thought. Especially coming from supposedly educated investors. Several shareholders commented they would keep GE because they bought it at $6-$9 during the 2008 market meltdown. I don’t really understand why the price they paid 9 years ago, means something today. In fact, the price you pay for a stock doesn’t really matter and I’ll tell you why.

Paper profit is only good… on paper

Ok… so you bought GE at $6 and it’s now trading at $30. The first thing I want to tell you is congratulation. It was a risky guess, but you were right, that’s great! But now, do you still think GE is the best buying opportunity now? Would you buy more GE shares at $30? If the answer is yes, then it’s okay. This means your investment thesis is still good and you believe GE is a strong company that will continue growing.

But if you tell me you bought GE on a momentary and exceptional drop, maybe it’s time to revise your position. Because over the past 5 years and over the past 10 years, GE is underperforming the S&P 500. GE appeared to have become a great investment only for those who bought it during the first 6 months of 2009 while it was trading at its lowest point.

Upon my analysis, my guess is that GE stock will stagnate in the upcoming years as the company isn’t showing strong growth vector and is struggling to increase its dividend every year. Therefore, GE shareholders could sell their shares and cash their profit!

Yeah, but I’m already making 250% profit on this trade since 2009, I can keep it for another 10 years and reap the dividend. True, but imagine if you take your profit and buy another strong company now that will not only pay a strong dividend but will also bring you stock appreciation?

Between you and me, I think MMM and HON will outperform GE in the next 10 years.

Yield on cost is interesting, but there is more

Another point made by GE shareholders was their yield on cost. Let’s say you bought GE at $8. The company now pays a quarterly dividend of $0.24 or $0.96 per share. Based on your cost of purchase, the stock yields 12%. This is quite impressive. Once again, those investors have made a great move back then. But what is happening now?

Now, an investor that had used $10,000 to buy GE at $8, receives $1,200 in dividend per year (12%). His shares also worth $37,500 as the stock price is around $30 these days. With $37,500, all you need to find is a company paying 3.2% yield to receive the same amount of money in dividend.

This changes the whole perspective. If you go out on the market and look for a 12% yielding stock, you will find nothing but risky picks. However, if you look for a company yielding between 3% and 3.5%, you can find plenty of interesting companies. Companies that show better growth potential in the next 10 years than GE. Because unless you have picked GE during its sweet spot at the beginning of 2009, this stock has underperformed the market since the techno bubble in the 2000’s.

A good investment makes your portfolio bigger

I expect two things from my portfolio going forward: #1 increasing its dividend payment each year and #2 increasing its value each year. Because this is what good company do. Therefore, it’s only normal if you keep any stock for a while that your price paid would become ridiculously low.

This is where we all tend to become more lenient. For example, I’m holding on to my Coca-Cola (KO) shares right now as I bought them a few years ago, and they show a nice profit on paper. However, can KO really continue to contribute to my portfolio now? The price has been stagnating for a good 2 years now (if it’s not more!). Let’s not go crazy here and sell any stocks that has underperformed over the last 2 years. My point is to always review your holding and confirm if your investment thesis is valid. While reviewing Coca-Cola, I must find more reason than simply “I keep it because I make X% of profit on paper”. This is not a good reason to keep any company.

So, tell me, why to keep a stock just because you bought it low?

I might have missed the point, but after this post, I really wonder why one would keep an investment simply based on their paper profit or their yield on cost. I think there could be strong opportunities out there, don’t you?

Which other investing strategy do you follow?

I still remember the first year of my investing journey. I started investing at the age of 24. This was back in 2003 – one of the most perfect times to invest and make a lot of money. It was after the techno bubble, when I could barely keep up in my university classes because was too busy playing Tetrinet!, and before the catastrophic 2008 market collapse.

With a strong financial background which was acquired through my bachelor’s degree and two summers working in an office of a derivatives & futures department, I was convinced I had everything I needed in order to succeed. At the time, I was working in a department which offered credit to investing clients. We were doing mostly investment loans – a leverage technique involving the lump sum of an investment in the market taken as collateral to guarantee an interest-only loan. I decided to use this technique for my own good and withdrew $19,500 from my personal line of credit and started picking some stocks.

Back then a monkey could have done it and a smarter monkey could have built a $70,000 portfolio within three years. I was part of the smarter monkey. I sold my portfolio, paid down my line of credit and used the remaining $50,000 to purchase my first house with a solid cash down.

I had no investing strategy

Since the market was good I decided to simply chase returns from one stock to another without really having a set of metrics to follow or an investment process in place. I was buying and selling as I saw fit and as I saw my portfolio growing stronger. Honestly, I thought I was a genius… but I was just a smart monkey!

I was fortunate enough not to lose much money during the 2008 crisis as my portfolio was relatively small. However, this was a good lesson. I learned that I needed an investment process to go forward and avoid bad results in my portfolio. This is how I started my quest to a solid investing strategy.

Penny Stocks – Technical Analysis Buzz

During my “smart monkey period” I was using a little bit of penny stocks and technical analysis. I thought that by simply looking at graphs that I could predict the future. Surprisingly, there are tons of investors claiming they can but rarely do they show me what is going to happen. They are far better at explaining the reasons why something happened yesterday. After a few successes, eventually I got burnt and began to understand that this was more about shamanic luck than anything else. Sadly, I didn’t have any totem on my desk to build my strategy.

Growth – Value – Whatever

The first two approaches you read when you open books about financial theories at school are the growth and the value approaches. Honestly, I liked both but, they didn’t seem like a complete investing strategy to me. After reading many portfolio managers describing their investment process, including famous methods with “bottom up” and “bottom down”, I understood they were all pretty much selling the same “Kool-aid”. They all look for undervalued solid companies with future growth perspectives. The difference is that growths require taking additional risks while waiting for future money to come whereas values aim for sure shots that will gradually rise over time. However, some successful growth stocks become values and vice versa … some value stocks give strong growth.

Dividend Growth Investing as My Motto

As you know already, dividend growth investing has been my motto for several years now. I have built a solid investment process which guides me through my journey toward financial freedom. I favor DGI over any other strategies because it enables me to post solid and consistent return without having to trade every week. It is easier to find solid companies and keep them for years while cashing their growing dividend versus trying to find the next Apple (AAPL) and sell it at the right time.

I feel I have all the time in the world as I’m in my mid-30’s. Therefore, I can let the power of compounding interest grow my payouts for the next 50 years. Having said that, I also like to keep my mind open to other investing strategies.

Using ETFs as a Complement?

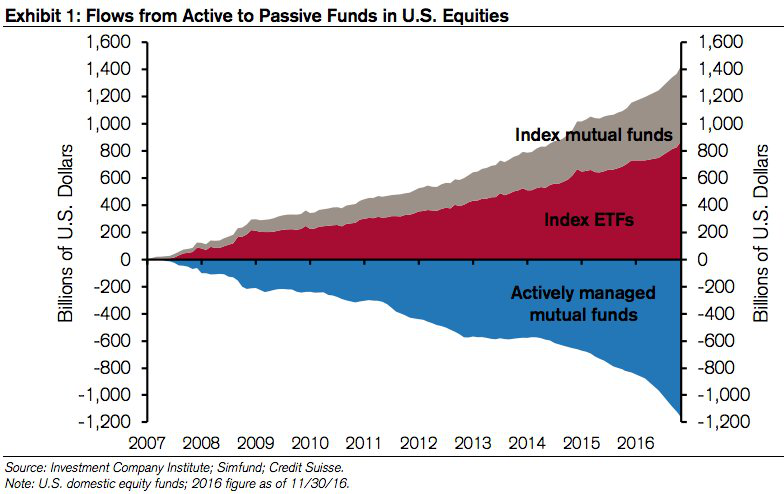

At the beginning of 2016, I also made the decision to manage my kids’ tuition money with my DGI approach. It was easy to build a portfolio as I had little over $12,000. This year, it is part of my 2017 financial goals to save additional money in this account. However, I will not be adding big lump sums but, rather, a monthly amount. For that reason, buying individual stocks might not be the perfect solution. Based on this thought I started looking into ETFs investing. One graph caught my attention while I was doing my research about what an ETF is:

As you can see, there are tons of money going out of actively managed mutual funds and moving toward index investing. The lion’s share goes to index ETFs as they are more flexible and cheaper than most mutual funds.

I could easily use one or two well diversified ETFs such as VIG (Vanguard Dividend Appreciation ETF ) and XDV.TO (iShares Dow Jns Cnd Slct Dvdnd Indx Fnd) or go even wider and purchase SPY or XIU.TO to follow the S&P 500 or the TSX. With a simple series of clicks I would be building a core portfolio with a minimal investment. After all, following the market’s performance isn’t that bad!

I’ve decided to invest in individual stocks primarily because I like it. I like reading financial statements, I like understanding business models and trying to figure out if they will succeed over time or not. Picking a bunch of ETFs and letting them work their magic doesn’t sound very attractive at first sight. However, this strategy does work very well and could be a good complement to my core strategy when I have smaller amounts of money to invest.

Which strategies do you use?

Currently, I’m still doing additional research about ETFs investing. I’m not convinced yet, but the whole concept is very tempting. I’d like to know if you use or consider other types of investment?

© Copyright 2013 Adividend