On the Road #21: Guatemala Magic & Belize Paradise

As soon as I can, I’ll update you on my one year trip. I’ve decided to leave everything behind and spend real time with the people that matter the most in my life: my wife and three children. This is my story, I hope it will inspire you to create yours.

You can read my previous “On the Road” articles:

- On the road #1

- On the road #2

- On the road #3

- On the road #4

- On the road #5

- On the road #6

- On the road #7

- On the road #8

- On the road #9

- On the road #10

- On the road #11

- On the road #12

- On the road #13

- On the road #14

- On the road #15

- On the road #16

- On the road #17

- On the road #18

- On the road #19

- On the road #20

Date: from March 15th to March 28th

Countries/States/Province traveled through: Guatemala & Belize

Wow… time really flies! As I’m writing this On the Road, we are about to cross into Mexico and officially leaving Central America. I will keep awesome memories of this part of our trip. The simplicity, the relax attitude, the ultimate freedom and the joy of being alive. This passage has been a true introspection for me and I would have spent even more money in psychologist, yoga and meditation retreat to grow personally as I did in the past 7 months.

I still have one chapter of Central America to tell. It all starts at the border of Guatemala when El Salvador officials noticed my car registration number doesn’t match my temporary importation vehicle permit…

Nothing can put a Crossing Border Ninja Down

The official was quickly telling me about “penalizar” and other words meaning I would have to “compensate” them for their incompetence of keying the right information on their stupid permit. With a great combination of playing dumb and having my daughter smiling and laughing right besides me, the official starting to think that I couldn’t understand a word of what he said (hahaha!). A few minutes later, we were off to Guatemala with the correct number on my new importation permit!

Our first stop was in a hotel parking lot in Chequimula:

There is nothing better than a hotel with free wifi, complimentary coffee and free water refill for Freefall! We had the chance to meet the owner and his son during our stay. We gave them a few tips about what to visit in Canada as they were spending their summer vacation in British Columbia. During our trip, we have learned that making stops here and there to relax, work and homeschool our kids was a smart thing to do. This is why we decided to change our beat on our way back and include many moment like this. It helps me keeping the momentum I gained with my websites in Costa Rica and kids rather get over their school work within a few days and have the rest of the week off to do activities.

When we left Chiquimula, we headed toward Rio Dulce. This was supposed to be an easy day on the road and finishing it in a Marina. Well, there was an accident on the road and we spent 5 hours driving 17 km…

I never realized the importance of having space on each border of the road. I do now! In Guatemala, there isn’t any space to drive on the side road. Therefore, when 2 big trucks get into a collision, it takes forever to take them out! Fortunately, we had a great night at the Marina where kids played in a real boat while we were cooking.

In Guatemala, there are the famous Semuc Champey waterfalls. Because we have learned that Freefall can’t do too much off roads, we decided to go see Las Conchas, the second most impressive waterfalls of this country. This was a wise decision as we heard about another family taking a 4 hours bus ride to get to Semuc Champey! Unfortunately, there was lots of rain the day before our visit and the water was completely brown….

We had lunch there and decided to continue driving further until we arrived at Flores, a small village on an island. We took the next day walking around and explore this colonial village. I just can’t get enough of their architecture!

But the moment we were all waiting for was our visit at Tikal. We spent 2 days in this magical Mayan city. We haven’t had the chance to visit many Temples so far (they prefer you don’t call them ruins, but temples!), but Tikal was just amazing. It was fun to walk across the jungle, feeling like Indiana Jones about to discover riches from the past. We were allowed to climb pretty much everywhere and the site had only a few tourists. Kids were playing hide-and-seek while we were astonished by the natural beauty of the site. Even better, it was a clear blue sky and the sun was reflecting on all temples.

Belize Paradise

Leaving Tikal in the morning, we entered Belize not too long after. I was happily surprised to see Belizeans having more structure and being more serious about their borders. We crossed them easily (we are ninja, remember) and we made a stop at San Ignacio for a few days. Belize is completely different from all the other countries in Central Amercia. First, they speak English as their native language and a good part of the population is black and not Latino. There is a relax ambience with a touch of Bob Marley everywhere. Most convenience stores a held by Asians and we even saw an Amish community. I didn’t expect much of Belize and I was happily surprised by this wind of change!

The highlight of our trip in Belize was definitely the four days we spent on Tobacco Caye, a small island in the middle of the ocean. In each country, we identify something specific we want to experience. So far, we have lived with locals in Nicaragua, we surfed in El Salvador and we visited temples in Guatemala. For Belize, we decided to live on an island. This was just like lending into paradise. The concept is great: a small island with about 50 people max on it. We lived in small cabanas and food was served at 8am, noon and 6pm by a group of super happy Belizean. You could hear them having fun and laughing all day while hanging around the small properties. The view was incredible and we had access to snokerling gears (the island is right on a reef where you can swim with gigantic eagle rays and hundreds of kinds of fish), kayaks and Stand-up paddles (good I like this sport!). We chose to disconnect completely for 4 days. Therefore, we spent time with kids in the water and read a few good books in our hammock.

We realized there was a lot more to discover about Belize than we thought. They have a luxurious jungle, tons of temples to visit (98% of them are not excavated yet!) and cave you can swim and to tubes! Since we have decided to use our traveling budget for the island, we will have to come back to this beautiful country later on!

I will be in Mexico until April 20th and should enter Texas around April 21st. Let me know if you are on my way back, maybe we could meet!

AbbVie: Growth and Dividends All In One

This is a guest post written by Bob Ciura with Sure Dividend. Sure Dividend focuses on long-term dividend growth investing.

Stocks are typically grouped into one of two main categories, depending on their individual characteristics.

Some are called growth stocks, which are those companies that are in the growth phase of their corporate maturity.

These are usually companies that produce above-average revenue and earnings growth each year.

Then, there are value stocks, which are cheaply priced based on their price-to-earnings ratios. Value stocks also tend to pay dividends to shareholders.

Health care giant AbbVie (ABBV) might be one of the rare stocks that offers a mix of both qualities.

AbbVie has generated excellent growth since it was spun off by Abbott Laboratories (ABT) in 2012.

And, AbbVie is a Dividend Aristocrat, a group of companies in the S&P 500 that have raised dividends for 25+ years.

You can see the entire list of Dividend Aristocrats here.

This article will discuss how AbbVie stock can fulfill investors’ desire for growth and dividend income.

Business Overview

AbbVie is a global health care company, operating in the pharmaceutical industry.

It was spun off from Abbott, so that it could grow on its own without being held back by some of Abbott’s slower-growth segments.

This is a difficult environment for pharmaceutical companies like AbbVie, because of intensifying pressure on drug prices.

Not only that, but drug companies are always at risk of losing patents on major blockbusters, which opens the floodgates to generic competition.

AbbVie is not immune from these pressures.

However, the company has still generated excellent earnings growth over the past several years, even in a highly challenging climate.

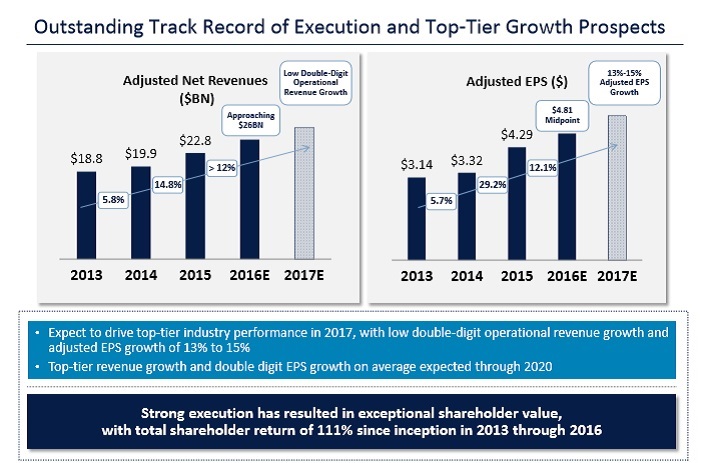

Source: 2017 JP Morgan Healthcare Conference, page 4

In 2015, earnings-per-share soared 29%. Last year, AbbVie managed 12% earnings growth, which is still quite impressive given the industry headwinds.

Its growth is largely due to the success of Humira, the company’s most important individual product.

Humira has been a major blockbuster for the company—its sales increased 16% last year.

But now that Humira has lost patent protection, AbbVie could be vulnerable to generic competition. Humira alone accounted for more than 60% of AbbVie’s total revenue in 2016.

The good news is AbbVie expects Humira to continue growing sales, even when new competition enters the market.

Growth Prospects

AbbVie has a two-fold growth strategy: continuing expansion of Humira, and growth from new products.

AbbVie’s future growth will still heavily involve Humira.

Even though Humira is off patent, AbbVie believes it can continue growing, because its high effectiveness has differentiated itself from rival drugs.

By 2020, AbbVie expects Humira will generate $18 billion in annual sales, which would represent 12% growth from 2016 revenue.

Source: 2017 JP Morgan Healthcare Conference, page 13

And, AbbVie continues to invest heavily in R&D, to pursue new drug development.

R&D expense was $4.4 billion in 2016, representing 17% of revenue.

This spending has paid off, as the company has a robust pipeline to fuel future growth. AbbVie often refers to its portfolio as “de-risked”, meaning it has many late-stage entities that are nearly ready to hit the market.

In all, AbbVie has eight late-stage therapies that the company believes can collectively generate $25 billion-$30 billion of annual revenue by 2020.

One of the biggest long-term growth opportunities for the company is in hematology, which is a large and relatively under-served market.

Source: 2017 JP Morgan Healthcare Conference, page 9

AbbVie envisions hematologic malignancies being a $50 billion market by 2020, compared with a $29 billion market in 2015.

This sets up a huge opportunity for AbbVie, since it has taken a leadership position in this category. Its major drugs designed to address this therapeutic area include Imbruvica and Venetoclax, which it launched in 2013 and 2016, respectively.

The early results are very encouraging: Imbruvica sales more than doubled last year, to $1.8 billion. Imbruvica is now AbbVie’s second-biggest drug by annual revenue, behind Humira.

Led by these two drugs, AbbVie’s hematological malignancy portfolio is equipped to serve two-thirds of the total addressable market.

Valuation & Expected Total Returns

AbbVie generated adjusted earnings-per-share of $4.82 in 2016. Based on its recent share price, the stock trades for a price-to-earnings ratio of just 13.5.

This is well below average.

For example, the S&P 500 Index trades for a price-to-earnings ratio of 26 on average.

As a result, AbbVie stock could be very cheap. If the price-to-earnings ratio increased to 26, the stock would double from here, just from an expanding valuation multiple.

Aside from a higher valuation, AbbVie stock will generate future returns based on earnings growth and dividends.

A potential breakdown of AbbVie’s long-term returns could be as follows:

- 6%-8% revenue growth

- 1% growth from share repurchases

- 4% dividend yield

Going forward, the stock could provide 11%-13% total returns. And again, this does not include any expansion of the price-to-earnings multiple.

Therefore, AbbVie stock is very attractive on a valuation basis.

Dividend Analysis

As previously mentioned, AbbVie is a Dividend Aristocrat, going back to when it was a subsidiary of Abbott.

Since its spin-off and IPO, the company has accelerated its dividend growth, thanks to its high earnings growth over the past several years.

Source: 2017 JP Morgan Healthcare Conference, page 14

Such strong dividend growth has elevated AbbVie’s dividend yield to a hefty 4%.

Its dividend yield is double the 2% average dividend yield of the S&P 500 Index.

There should be little reason why AbbVie cannot continue to grow its dividend at double-digit rates going forward.

Based on adjusted earnings-per-share, AbbVie carried a dividend payout ratio of 53%. This means the company distributed just over half of its 2016 adjusted earnings-per-share as dividends to shareholders.

A payout ratio slightly above 50% is very comfortable.

And, the company is likely to continue growing earnings-per-share, meaning 10% annual dividend growth over the next several years is definitely possible.

Final Thoughts

AbbVie has all the qualities investors should look for. It has compelling revenue and earnings growth potential, and the stock has a cheap valuation.

Plus, AbbVie stock has a hefty 4% dividend yield, making it an attractive income opportunity as well.

Because of these qualities, AbbVie ranks highly using Sure Dividend’s 8 Rules of Dividend Investing.

AbbVie is among the top health care stock opportunities for 2017.

Its impressive financial performance, even in a tough environment, demonstrates the strength of its business model and future pipeline.

Top 4 Dividend Stocks to Hold Now

April 11, 2017

In my latest article, I’ve highlighted 4 popular dividend stocks to sell. As I wrote at the end of this article, I don’t appreciate when people criticize without bringing something on the table. For this reason, I’m offering you 4 interest stock picks for 2017 that could easily replace the other bad seeds.

Honeywell International (HON)

Business model:

Honeywell invents and manufactures technologies to address some of the world’s toughest challenges initiated by revolutionary macrotrends in science, technology and society. The company evolves in three different industries: Aerospace & Transportation, Automation & Control system, Materials & Chemicals. The company recently combined the aerospace and the transportation segment in order to improve scaling economy.

Main strengths:

The company has put additional focus on software engineering with nearly 11,000 engineers working on software instead of more classic industrial goods. The software business is better as it enables more combinations of services and drives higher margins. Honeywell certainly has some solid ground for future growth.

Potential risks:

While margins improvements were quite phenomenal, we can’t expect to see the company keeps increasing its margins. Therefore, further numbers shouldn’t be that impressive. Also, HON automation segment may suffer from the oil and gas industry slump.

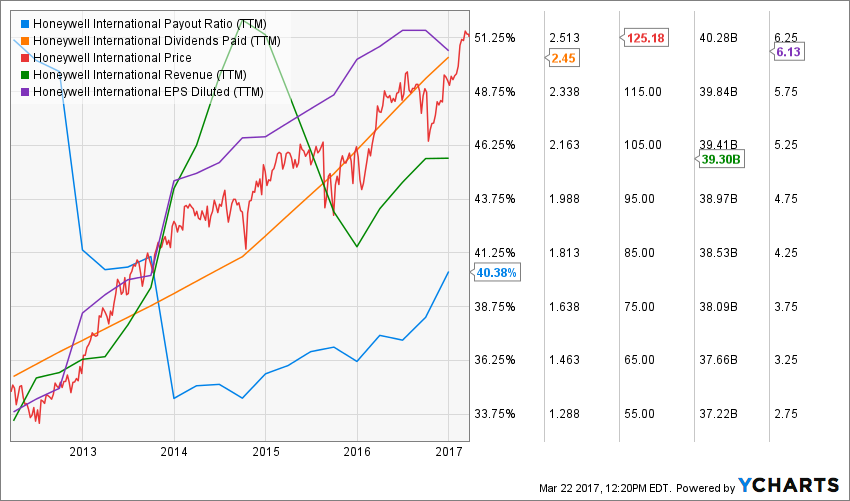

Dividend growth perspective:

management had announced last year that the dividend payout ratio will increase in the upcoming 4 years. In 2015, the dividend payment increase was of 15% and 11.76% in 2016. I’m not putting on my pink colored glasses and expecting a 12% dividend growth for the next 10 years, but I can appreciate the growth will be significant for several years to come.

Investment thesis:

Honeywell has made impressive efforts to improve their internal practices over the past 15 years after failing to merge with General Electrics (GE). Those efforts paid well as the company operating margins improved from 7.6% in 2004 to 15.2% in 2014. Those impressive margin increase lead HON EPS to increase by 10% in 2015 as the company is facing a challenging economy. The company was also able to increase its dividend by 10% CAGR over the past 5 years. HON is a leader in the aerospace control and safety systems and should benefit from its leadership position during the commercial aircraft upcycle.

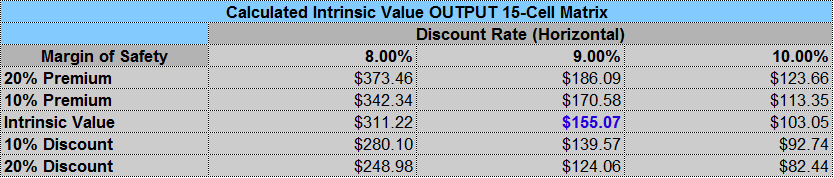

Valuation:

Source: Dividend Monk Toolkit Excel Calculation Spreadsheet

Lowe’s (LOW)

Business model:

Lowe’s is the second-largest home-improvement retailer in the world with over $59 billion in annual revenues. Strong from its position in the U.S., Lowe’s benefits from the recent rebound of the world’s largest economy. LOW is also expanding through acquisitions as management recently closed the purchase of Rona in Canada. Lowe’s doesn’t only focus on selling you home renovation and improvement products, it also uses their experienced salesforce to provide you with additional advice. The company has also successfully built a solution-based segment within its stores. By offering a complete solution from start to finish, Lowe’s make sure to “capture” the customer for its entire project purchases.

Main strengths:

Mainly due to its size and high tech product management platform, Lowe’s is able to generate substantial economies scale. The firm has created an integrated supply chain that efficiently routes nearly 75% of all Lowe’s merchandise through one of 15 regional distribution centers. Its omnipresence in North America enables Lowe’s to benefit from strong construction business in Canada and the United States. This alone should be enough to bring consistent growth for years to come.

Potential risks:

As we see it, the biggest risk for LOW is definitely another economic slowdown. There are still several uncertainties in the air and a contraction of the US economy would definitely put a halt to LOW’s strong growth perspectives. The company margin will be under pressure in the upcoming years as competition with Home Depot intensifies and Rona’s lower margins are included in Lowe’s numbers.

Dividend growth perspective:

LOW shows a very strong business model generating a consistent cash flow stream. While the company will benefit from additional cash flow during a strong economic cycle, its distribution network efficiency will continue to provide management additional room for dividend increases in the future. The secret of LOW’s long dividend increase history is found in a very low payout ratio (35%) and a very low yield too (less than 1.50%). Management’s conservative approach makes the company’s dividend growth sustainable for several years to come.

Investment thesis:

Focus on a recovering U.S. economy and additional growth from acquisitions should continue to push LOW’s stock price higher. Its strong brand and the way it helps its customers to go through bigger projects by offering a “one-stop-shop-&-advice” service will secure LOW’s market share and improve margins over the long haul. Lowe’s has been able to transform a simple home product store into a great service offering for home projects. There is definitely more room for growth in the upcoming years.

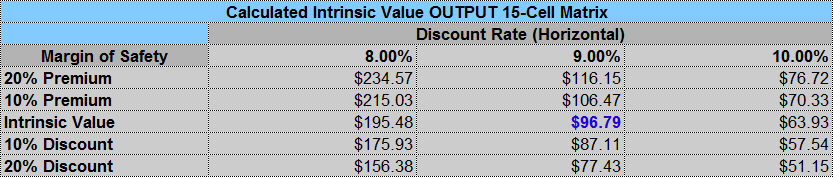

Valuation:

Source: Dividend Monk Toolkit Excel Calculation Spreadsheet

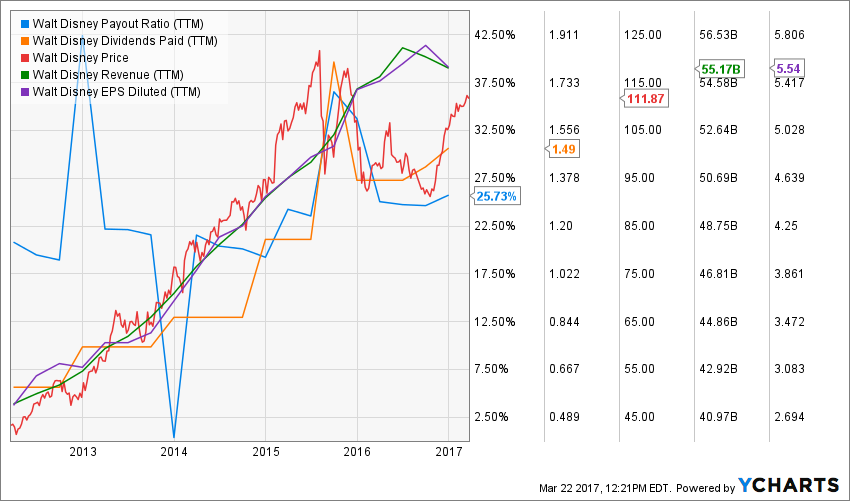

Disney (DIS)

Business model:

DIS has become more than entertainment parks and Mickey. It is now the largest entertainment business in the world. Walt Disney is divided into five different segments: Media Networks, Parks and Resorts, Studio Entertainments, Consumer Products and Interactive. The Media division (ABC, The Disney Channel and ESPN) leads DIS revenue shares with 44% of the company total sales.

Main strengths:

Disney has built one of the most respectable brand in the world. Its attention to details makes their theme parks and movies almost perfect each time. They also show a strong synergy between all their divisions. Therefore, whenever Disney makes a good move, it is able to duplicate its returns through derivative products across its other divisions. The recent Start Wars success is a great example of how a blockbuster movie engaged more enthusiasm for theme parks and figurines.

Potential risks:

Over the past 18th months, many financial analysts have spit in the soup. The main reason being the inevitable death of the cable industry. This will not happen in 2017, but analysts are concerned about the highly profitable ESPN network slowly losing their customers for streaming options. This could hurt the stock price over a short period of time again in 2017, but we remain strongly bullish for DIS over the long haul.

Dividend growth perspective:

Disney is not known for its dividend payments. It is usually paying a shy 1% yield even with a strong dividend growth policy. The good news is that the yield is now closer to 1.50% as the stock price stagnated while the dividend continued to grow. 5 years ago, DIS dividend payment was at $0.60 per share for the year and it will be paying $1.49 in 2016. The payout ratio is still very low at 24.63%. This shows you how strong the dividend growth potential is.

Investment thesis:

DIS has become more than entertainment parks and Mickey. It is now the largest entertainment business in the world. Walt Disney is divided into five different segments: Media Networks, Parks and Resorts, Studio Entertainments, Consumer Products and Interactive. The Media division (ABC, The Disney Channel and ESPN) leads DIS revenue shares with 44% of the company total sales.

Disney divisions will benefit from the US consumers spending more, especially with the coming of the new Star Wars trilogy. Finally, Disney is the strongest brand for family entertainment and this competitive advantage is nearly impossible to replicate.

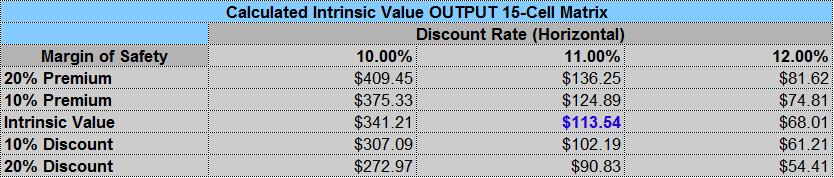

Valuation:

Source: Dividend Monk Toolkit Excel Calculation Spreadsheet

BlackRock (BLK)

Business model:

BlackRock is the world largest asset manager, period. The company offers a variety of products for all asset classes (from fixed income to equity and alternative investments). Over the past decade, BLK grew a lot faster due to the popularity of its ETFs product line; iShares (there is something with this “i” thing, huh?).

Main strengths:

BlackRock benefits from a core business model where 61% of AUM is coming from institutional clients. Due to shifting costs and BLK solid reputation, this is a very sticky business. BLK also benefits from Govt regulation modifications pushing brokers and advisors to use more cost-efficient investing products. Since BLK is the largest ETF manufacturer, it will automatically drive its sales up.

Potential risks:

Investing firms are always one crash away from a bad year. In the event of a bubble burst as we had in 2008, BLK shares will definitely plummet. However, I see this outcome as very unlikely at the moment. The economy is growing, employment in the U.S. is strong and the stock market continues to move forward.

Dividend growth perspective:

BLK has increased its dividend payment for 7 consecutive years now. With a payout ratio around 50%, management has lots of room to continue its dividend growth policy for several years to come. Since BLK benefits from a strong growth vector through its ETFs products, you can expect this company to show on many dividend investor radars in the years to come.

Investment thesis:

BlackRock is a leader in its industry and has built a solid relationship with its clients. They operate a sticky business with institutional client and they are a leader in a growing investing trend. As BLK offers a wide variety of products, it will manage making money regardless if investors are bullish or bearish.

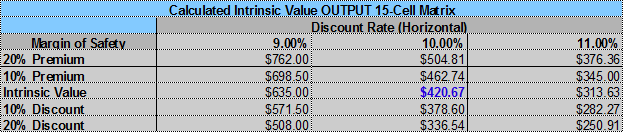

Valuation:

Source: Dividend Monk Toolkit Excel Calculation Spreadsheet

How I selected those 4 companies

Before I select any companies to be part of my portfolio, I go through an exhaustive investment process. Each company must meet the 7 dividend investing principles. Those principles have been established based on several academic studies and over a decade of my financial experience in the stock market. I not only think those stocks will do well in 2017, but I believe they will do well in the long run too. In my opinion, those are keepers for a dividend growth portfolio.

Top 4 Popular Dividend Stocks to NOT Hold

April 06, 2017

Warning: be ready to be shocked by reading this article

And I’m ready to take your tomatoes… even though I’m right

Instead of making another list of great stock picks, I decided to do the opposite today. I actually wrote about these companies over the past 12 months telling investors to sell them now before it’s too late. What makes them special is that they have tons of fans as they are very popular dividend paying companies. They often ace the first filtering processes due to their competitive advantage and good fundamentals. Their “brand” as a dividend paying stock is strong among investors but I feel that they offer more smoke than anything else. Many investors are blinded by the story told by these companies and tend to ignore the story that will happen in the years to come.

Those companies are on my black list and I don’t see them returning to my watch list any time soon. In fact, I think each of them is a BIG SELL at the moment.

General Electric (GE)

General Electric is a 100-year-old company offering various digital industrial products. The company counts 8 divisions within its “GE Store”:

- Power: combustion science and services, installed base.

- Energy connections: electrification, controls and power conversion technology.

- Renewable energy: sustainable power systems and storage.

- Oil & Gas: services & technology.

- Transportation: engine technology and localization in growth regions.

- Lighting: LED bulbs.

- Healthcare: diagnostics technology.

- Aviation: advanced materials, manufacturing and engineering products.

All right, what could possibly go wrong with this all-star player? I mean, even Warren Buffett holds shares of GE in his portfolio. Now that the company is getting rid of its financial division (GE Financial), management is claiming to focus on what they do best; manufacturing a wide variety of products. Fine.

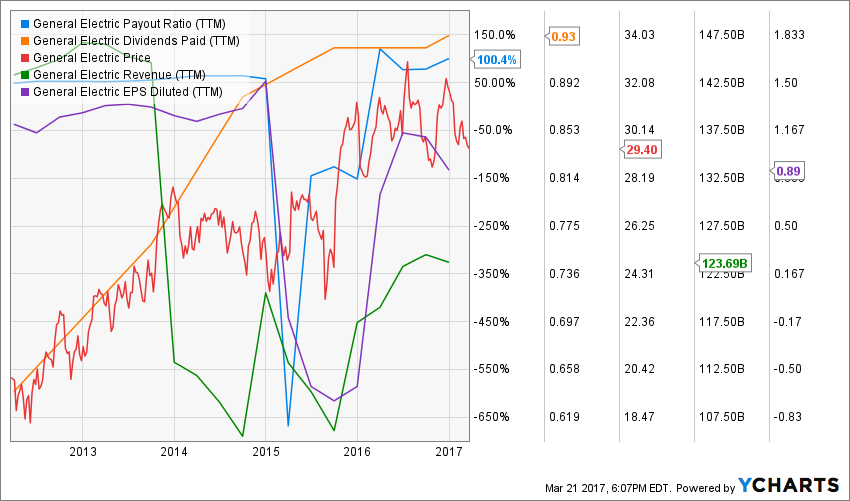

But what this great story doesn’t tell you is that it’s not looking well for future dividend payments. First, the company cut its dividend severely back in 2008 and shareholders haven’t gotten back to their previous distribution level yet:

Source: Ycharts

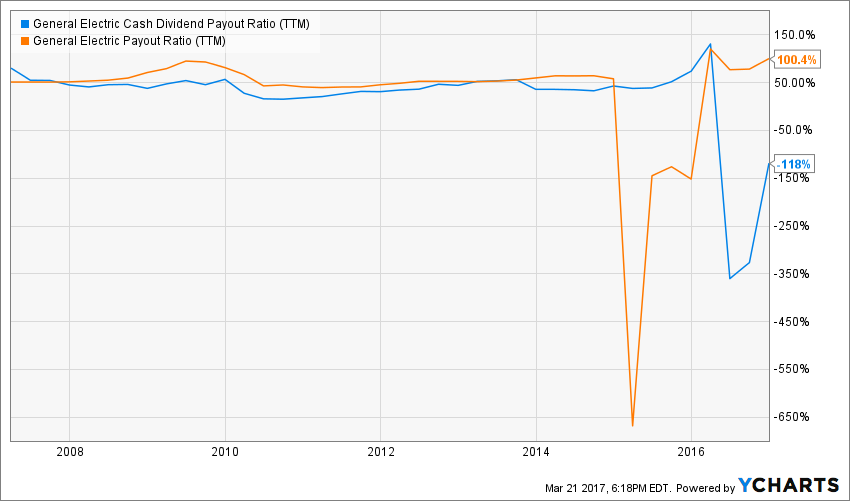

But you are going to tell me the dividend payment is climbing slowly but surely again. However, tell me how they will continue to do this with such payout ratios:

Source: Ycharts

If you take the accounting approach, the company is fully saturated with a 100% payout ratio. It is not surprising to see a meager dividend increase since 2014. Then, if you take the cash flow approach, it’s even worse. The company is bleeding cash seriously.

The main argument I hear from current shareholders is that they picked up GE at $9 during the crisis. Well done, great move! However, now that you have made a solid profit on your investment, tell me where GE stocks will be going in the next 10 years? We already see that the dividend growth rate won’t be astonishing… and the stock price will not go anywhere. In fact, GE’s stock has been severely underperforming the stock market for the past… 20 years!

Source: Ycharts

Wal-Mart (WMT)

Source: Ycharts

While GE has good fan base, my guess is that Wal-Mart is even more popular. For one fact, WMT is part of the elite group of dividend aristocrats with 42 consecutive years with a dividend increase. In fact, it is now closer to gaining the ultimate title of Dividend King. Which kind of heretic would be crazy enough to spit on such a stellar company. After all, WMT’s dividend growth and payout ratios numbers are far from disgusting:

Source: Ycharts

In fact, when you look at these numbers, you would probably do well to throw me under the bus for my declarations. Wal-Mart is in no position to go wrong tomorrow morning and fail their shareholders. However, the vision of the future is definitely not as flourishing as the WMT of past days. Towards the end of 2016, I decided to sell Wal-Mart from my portfolio. The problem is that I don’t see how the company will be able to grow in the future.

In the retail industry, we all know the future is online. Brick & Mortar stores will continue to see their sales slow and eat up money in operating costs (more storage, more employees, etc). I was confident WMT would pick-up on the ecommerce trend at one point, but they have literarily failed to build an efficient online store over the past three years. The proof? They now had to spend $3 billion on Jet to get a sales platform that should perform… all the previous money was wasted on their website and now, more money will bleed out of their bank account to integrate this new platform. In the meantime, Amazon (AMZN) is growing their revenues like there is no tomorrow:

Source: Ycharts

If I project Wal-Mart in 50 years from now, what do I see? Probably an old success story that aged very badly with outdated stores and poor clientele still going to their stores. They will probably restructure, cut some employees and close some stores in the hopes of preserving their cash flow and dividend payment. This is called putting your company on an artificial respirator.

Being a Canadian, Wal-Mart’s future looks like a lot like the 130 year old Eaton company failure (which declared bankruptcy in 1999). We also had other retail stores that didn’t survive such as Zeller’s and Woolco’s. The three companies have something in common with Wal-Mart: they all underestimated their competitors coming to serve the retail industry but from a different angle. I’m telling you, Amazon will kill retail stores as we know them.

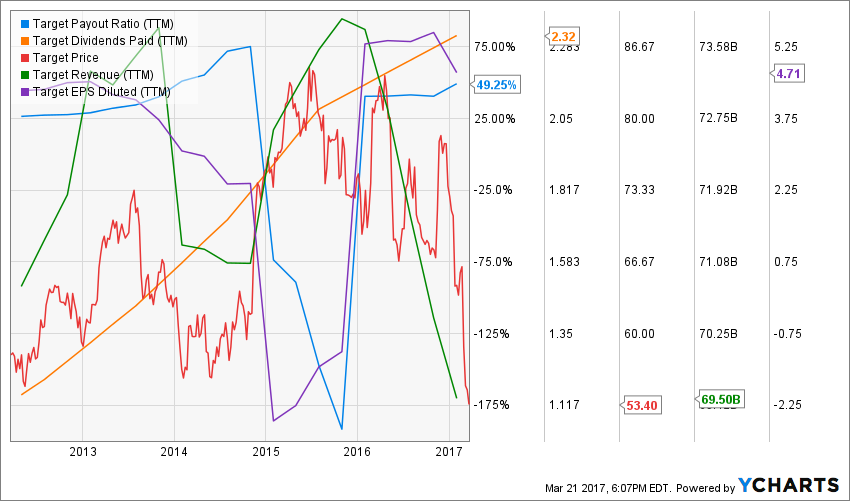

Target (TGT)

Source: Ycharts

Target’s story follows along the same lines as Wal-Mart. However, before proving their inefficiency online, Target had already disappointed me. This happened a couple of years ago when they tried to waste as much money as possible entering the Canadian market thinking they could sell us lower-quality stuff and compete against Wal-Mart that way. To be honest, I wasn’t insulted by Target coming to Canada. However, I was shocked to see how management misread the Canadian market.

Growth opportunities are getting rarer in the retail store business. You are not allowed to waste an opportunity like this. This makes me question Target’s ability to create growth vectors for the future. I mean, if they can’t read potential new markets and they can’t impose themselves as leaders online, where could they find growth?

I can appreciate Target’s solid core business. GE and WMT both have solid core businesses like TGT. However, having a core business is not enough to ensure future dividend growth. Even if a company evolves in a more mature and stable industry, it needs to find growth possibilities somewhere. Hoping consumers will spend more in your store is not a strategy.

Unfortunately, TGT’s fate seems in line with WMT… they will be both be eaten alive by the Amazon’s of this world…

Chevron (CVX)

Source: Ycharts

The last, but not least, stock you should sell in a hurry is Chevron. The CVX situation is a little bit different. You should not sell it because it has no future, you should sell it because there are absolutely no upside potential at the current price. After the oil bust in 2014, the CVX price dropped all the way down from its peak price of $133 in 2014 to $75 in 2015. I had advised my DSR members to buy the stock shortly after this drop (price was around $80 something). However, CVX stock price went rapidly back up and recovered most of its loss to $122 in December 2016. This was the time to sell the stock and this is what we did in our DSR buy list towards the end of 2016.

The thing right now with CVX is that its stock price is solely supported by rumors and hopes oil prices will go back up. As we all know, hopes don’t make money and don’t pay the bills. The proof is that CVX went from $120 to $108 in the span of the past 3 months as oil prices are struggling again. Buying or holding CVX right now is as good as putting your money in a coffee can in your refrigerator. You will not lose your money, but it will do sweet nothing for a while.

Chevron is going through a very challenging period. The company is selling assets to pay their dividend and is surfing on previously developed projects to generate cash flow. However, this long “pause” due to weak oil prices will affect the company for several years to come. There is no short-term future when CVX will generate an interesting return for its shareholders. It’s not worth it, even at a 4% yield.

Consider This List Instead

I’ve always considered those who only bash and complain to be unproductive. It’s a good thing to tell the world something sucks, it’s another to tell you what doesn’t, right? I thought it was important to highlight these 4 companies as they appear to me like big investment mistakes at the moment. I’d like to offer 4 replacements if you are about to sell these companies. I will provide a detailed analysis in my upcoming article but I didn’t want to you hanging in the dark in the meantime. Here are my 4 choices:

- Honeywell International (HON)

- Lowe’s (LOW)

- Disney (DIS)

- BlackRock (BLK)

On the Road #20: El Salvador Surprise

As soon as I can, I’ll update you on my one year trip. I’ve decided to leave everything behind and spend real time with the people that matter the most in my life: my wife and three children. This is my story, I hope it will inspire you to create yours.

You can read my previous “on the road” articles:

- On the road #1

- On the road #2

- On the road #3

- On the road #4

- On the road #5

- On the road #6

- On the road #7

- On the road #8

- On the road #9

- On the road #10

- On the road #11

- On the road #12

- On the road #13

- On the road #14

- On the road #15

- On the road #16

- On the road #17

- On the road #18

- On the road #19

Date: from March 7th to March 14th

Countries/States/Province traveled through: El Salvador

I don’t know if this is because we are gaining experience travelling, but everything seems easier this time around. I anticipated the “2 border crossings” day with a bit of nervousness. I don’t appreciate Honduras much due to its poor reputation. And this is not exaggerated. The last traveler we know who spent some time in Honduras got their car door damaged as thieves tried to break in. At 5:15am, we woke up and put our ninja border crossing gear on. After entering Honduras in less than an hour and 20 minutes, we drove in stealth mode until we were snared in a police control point. Obviously, driving in stealth mode with a 25ft white RV isn’t that easy! The police officer asked me for my vehicule titulo and mi passaporte. I show him my title with a “no a la ma?o”, which means “you can’t take it dude!”. He saw I wasn’t joking behind my ninja mask and dropped the ball, we were free to go without even showing our passports! We got to the El Salvador border right before lunch… 11:50 very bad timing! I had to wait an hour until everybody got back from lunch at 1pm and finally entered El Salvador around 1:20pm. A few more miles on the road and we hit the playa and I had a beer in my hand before Happy Hour started!

El Salvador Surprise

The first time we crossed this country, I had the feeling there was a gun pointed at my back the whole time. I didn’t like the ambience and seriously wanted to get through it as soon as possible. But this time, I wanted to stay at La Tortuga Verde, a cool place near Playa El Cuco that I had found right before leaving this country the first time. The plan? Stay here for a week and learn to surf!

The week started like a dream. Each morning, we woke up, enjoyed a nice coffee and then hit the waves with William and Amy. In the afternoon, I was working under a palapas, facing the ocean and feeling the nice breeze on my face. Seriously, this couldn’t get any better.

The three of us took a surf lesson the first day with Rory, a surfer from Montana. After about 10-15 minutes, we all took on our first white water wave. Before the hour ends, Rory let us go practice alone as we were jumping on waves quite easily. The rush of feeling the board in perfect balance and riding the wave is addictive! However, I must tell you; I’m not going to become surfer Mike tomorrow morning. While we took several white water waves (once the wave breaks, it’s easier to stand up on your board), I failed to take on waves before they break. Still, I had so much fun surfing every day of the week, it was a blessing! I clearly remember my last day surfing while I was looking at the sun shining a million flickers on the ocean, holding my board to face the wave and think: thank you life… I’m living this!

But we did a lot more than simply surf on that day. In fact, El Salvador had more surprises for us. Let’s start by the unexpected welcoming attitude from the people of the village. One of the benefit of staying more than a couple of days in the same place is that you get more smiles from locals as they recognize you as the week goes by. We even attended the 15th birthday party of a young girl where we were camping. In Central America, the 15th birthday is like the 18th in Canada, it’s a big event. In fact, it looked more like a wedding reception than anything! They were kind enough to share their meal with us during the celebration!

Then, we woke up early one day to go deep sea fishing! This was a lot of fun! We took a boat ride for about 3 hours. While we were trolling with 3 different lines, we could admire the beauty of the El Salvador coast. You can see mountains, volcanoes and a beautiful natural beach without any resorts higher than a two-storey house. I almost caught my first fish, it was darn heavy! Unfortunately, he broke the lure and got away. Then, it was William’s turn to “almost” catch one. As he was pulling it out of the water, the fish swung one last time and returned into the sea. My wife was sea sick and we had to return to land… so much for nothing… no fish for tonight, but a great adventure in our memories! We also had the opportunity to release baby turtles into the sea. Definitely, La Tortuga Verde is a great place to hang out!

Then, towards the end of the week, we met another traveling family; Jeremy and Lucie with their kids Jeanne and Gabriela. They were French, doing about the same trip as we are. They were heading toward Nicaragua, but decided to stay one more day so we can chit-chat a bit. It was another great moment with can exchanges to inspire and be inspired. I truly enjoyed their company and it was fun to discuss our adventures. At the same time, we also met Mariano & Monica, an Argentinian couple heading North. We might encounter them again during our trip and we also invited them to Quebec as they will be there next September. It will be a great chance to practice my Spanish again!

The downside of having great encounters is that you have to let your new friends go. The French family left the night before we did. They stayed an extra half hour to have a beer with us and then, it turned out to be 2 more hours, until there was no time left and the Goodbyes had to happen. At least, we can stay in contact and we might see each other again. They are already planning another trip to Asia for next year. Who knows… we may meet them in another country. The world is such a small place!

We left La Tortuga Verde with big smiles on our faces and spent the last day in El Salvador in a very cool place… Agua Termales! What about a bunch of hot springs where you can relax after crossing this country in one day? We even had the opportunity of climbing a short hike and exploring the valley. Definitely, El Salvador was a lot more than we expected!

This was only a week, but enough for us to create memories for life, plus I now have another sport to practice!

In my next on the road, I’ll tell you what happen when you cross a border and the Aduana makes a mistake with your car registration number…. Ouch!

© Copyright 2013 Adividend