Have you taken a look at the recent earnings?

It is without any surprise that many US companies posted slow revenue growth due to either a “challenging” environment or (an even more common excuse: due to a strong US dollar. I follow primarily dividend stock results and many of them are international businesses. No need to explain that a strong US dollar is hurting many dividend stocks in particular. The market didn’t overreact as it was more a mild earnings season without many surprises.

What you Need to Know about the Latest Earnings

71% companies beat analysts’ estimates in earnings

45% companies beat analysts’ estimates in revenue

Blended earnings growth was a scant 0.01%

It’s the lowest growth since Q3 2012 (-1.0%)

57 companies issued negative EPS guidance compared to 25 companies issuing positive EPS guidance

The market expected the energy industry to be hit harder than expected

Healthcare sector performed well with 10.5% companies surprising to the upside on earnings and 10.8% with better than expected revenue

Overall, analysts were quite pessimistic for the first quarter of 2015 and this is why there are so many earnings beats. This is not really because companies went out of their way to perform a strong quarter. This is why there wasn’t much movement in portfolios lately.

Healthcare (22.3%) and Financial sectors (13.4%) show the biggest earnings growth while Materials (-1.2%) and Energy (-56.6%) are lagging behind. For revenue, the winning sectors are Healthcare (10.5%) and Technology (5.6%) while Materials (-9.4%) and Energy (-34.5%) are, again, the biggest losers.

Finding the Right Stock in the Current Market

I believe the market is fairly priced, not overpriced. I don’t see any bubbles ready to burst yet, but it doesn’t mean you should keep investing your money in the first dividend stock that comes to mind. In order to help you in the search of relatively low priced stocks, I pulled out the following screener:

- P/E ratio under 16.8 (which is the current 12 month forward market average)

- Dividend yield between 2.50% and 10%

- Payout ratio under 85%

- 5 Year revenue growth positive

- 5 Year EPS growth positive

- 5 year dividend growth positive

The list includes 171 stocks with a few stocks trading on both Canadian and US market (mostly Canadian banks with US tickers). Sorry for Canadian folks but only 31 companies passed the test. This leaves 140 for the US market (I keep telling you that the US market is more diversified ![]() ).

).

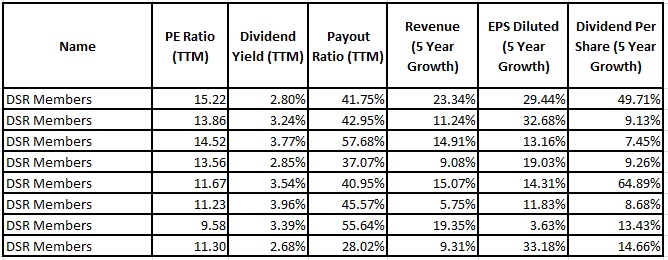

Some of My Selections

I just sent an email earlier this week to my Dividend Stocks Rocks (DSR) members with the Excel spreadsheet including the 171 stocks with stats. In this month’s newsletter, I also reviewed 5 US and 5 Canadian dividend stocks featured in this spreadsheet. It’s not too late to download the list if you register with DSR, you have access to our previous newsletters!

In the meantime, I’ll share with you 1 US and 1 CDN stock pick ideas coming from this list.

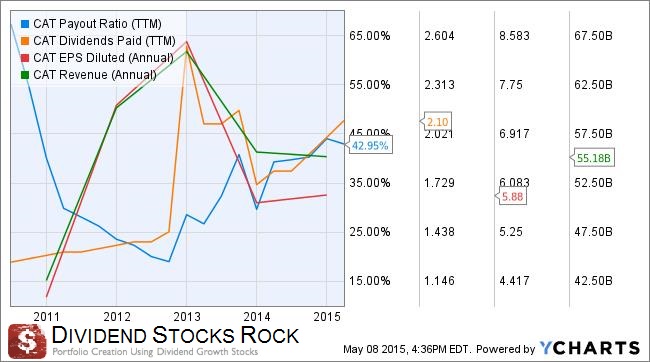

Caterpillar (CAT)

This is another company which is suffering in the resources sector. While the construction sector in the USA helps Caterpillar, the mining industry and low oil prices are dragging down sales expectations. Emerging markets are not what they used to and they won’t need as many Tonkas since those countries are not looking at double digit growth anymore. Caterpillar also sells lots of equipment to drilling companies for oil exploration. You can guess that this sector is also slowing down.

However, the world will always need world class equipment sold by CAT and it’s only a matter of time until the company hits another uptrend cycle and sees its sales on the rise again. When you look at cyclical companies such as CAT, you must identify the right time to enter in a position. We are currently in one of these moments.

The company currently pays a 3.16% yield with a payout ratio around 43%. The stock traded around 17-18 P/E ratio not so long ago and it is now down to 14.

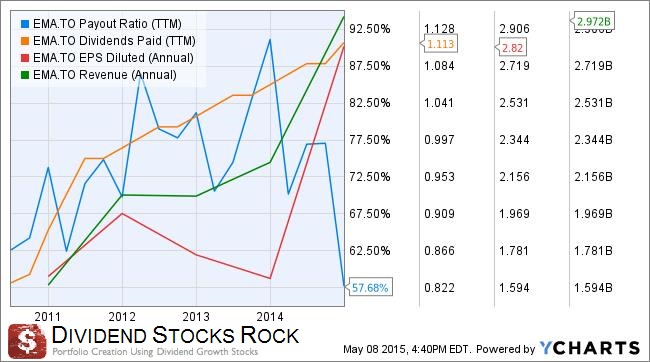

Emera (EMA.TO)

Emera has been on a nice run of +22% over the past 12 months compared to the S&P TSX at +3% for the same period. Still, the company is trading at a low PE ratio of 16.62 and offers great growth perspectives.

EPS and revenues rose due to increase in demand for energy in the US and a weak Canadian dollar. Similar to ADN‘s situation; this is a good time for Emera. The company is in line with its budget for its maritime link and should start producing additional revenues in 2017.

At first considered as a defensive play since we are talking about a utility company; EMA surprised with last quarter double digit earnings growth. Great dividend, great payout ratio and not overvalued. Enough said.

What The List Looks Like

If you are interested in taking a peak at the stats of the rest of the list, here’s what it looks like:

What about you, have you find any interesting companies to buy lately?