A few weeks ago, a member of Dividend Stocks Rocks enquired about Enbridge and Transcanada. Since both companies are trading on the same symbol on both US and Canadian market and that they are at the center of the attention with the Keystone XL pipeline, I thought it worthwhile to take a look at them.

While small oil companies cut their dividends and oil exploration related companies saw their contracts cut, there is still a type of company related to oil that is providing immediate growth potential: pipelines!

The pipeline industry is quite simple; it’s costly and complicated to put it in place (just look at the Keystone XL pipeline saga), but once it is open; the owner charges a price per barrel going through it. The best part; the flow of oil moving through pipelines is very stable. Therefore, it’s like having a direct line with a never-ending ATM. After reading this paragraph, you are probably going to ask: Mike, if pipelines are such an amazing dividend payers, why is it that both ENB and TRP are NOT part of your DSR portfolios? This is a worthy question. Let’s take a look at both companies to see why we haven’t picked them.

Enbridge (ENB)

Enbridge Inc transports and distributes crude oil and natural gas. It is also engaged in natural gas gathering, transmission and midstream businesses and power transmission.

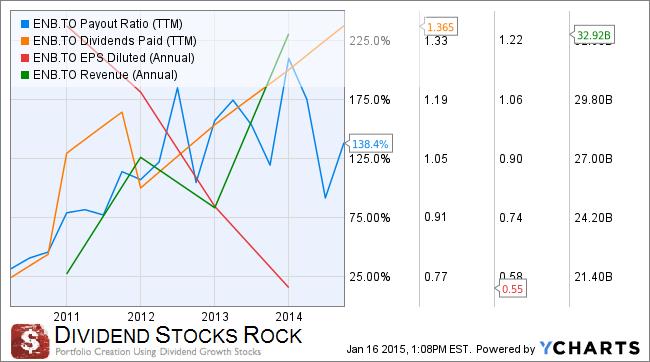

When I first looked at Enbridge’s DSR profile, I wasn’t impressed….

Very high payout ratio, ever dropping EPS and hectic revenues. This doesn’t sound much like a never-ending ATM to me! The company struggles to show consistent fundamentals while trading at a very high P/E ratio (around 62). While their business model definition inspires trust and conservative investment; their fundamentals do not speak the same language.

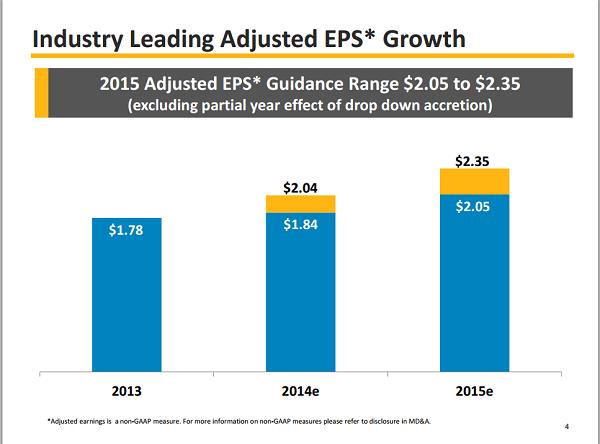

Then, we decided to dig further and look at ENB’s website and presentations. Here’s what we got from their 2015 Guidance Conference Call:

They use non-GAAP measures to adjust their earnings and show you they continue to make more money than before. Then, I looked at their statement of earnings to understand what is going on. I found that from 2012 to 2013, ENB operating income dropped by 14% due to higher expenses. I also looked at their cash flow to see if the pipeline was really growing the cash (keep in mind that EPS is based on accounting principles where the cash flow statement is king for any business). Well… due to a very high amount of investment, the cash flow statement is also lower in 2013 from 2012. There are good news related to this statement; #1 operating activities generate more cash flow than before and #2 if ENB invest massively, it also means they expect to make more money in the future.

I’ll be honest with you, I’m not a pipeline expert. Therefore I had to search throughout many documents to find why and how ENB was able to play some magic with their earnings and post growth while I see a big downtrend from Ycharts. Here’s their definition of adjusted EPS (source Yahoo Finance):

“The adjusted earnings discussed above exclude the impact of unusual, non-recurring or non-operating factors, the most significant of which are changes in unrealized derivative fair value gains and losses from the Company’s long-term hedging program and gains on the disposal of non-core assets and investments, as well as certain costs and related insurance recoveries arising from crude oil releases.”

Let me translate this for you: from my understanding, this means; the pipeline business continues to generate higher and higher profits but the hedging strategies around oil prices and the disposal of various assets/investments hurts their profit big time… year after year. There is one thing I’ve learned from EPS. Yes, it is based on accounting principles and you can trick them from time to time. However, you can’t trick them forever; if the business is making more and more money, at one point in time, the EPS will follow. This isn’t happening with ENB. After this analysis, you probably understand why ENB is not part of any DSR portfolios.

Transcanada (TRP)

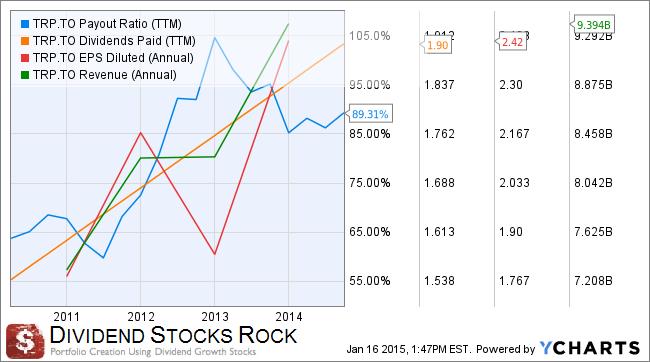

All right, now, let’s take a look at TRP DSR Profile:

At first glance, TRP’s fundamentals look a lot better than ENB. What really catches everybody’s attention right now is more if the Keystone XL project will happen or not. While the State Department looked at the project, it published a positive report saying it would have minimal impact on environment. However, they also mentioned that if the oil prices were to fall below $70, “price below this range would challenge the supply costs of many projects”. We all know Obama is not too eager to see this pipeline crossing the USA and, according to some, would result only as a benefit to Canadians. For now, the best move for any investor would be to look at TRP and exclude the pipeline perspective. If Keystone XL happens, than you can simply add this to your “best case scenario”. Since TRP can also look at its other project (Energy East) that goes across Canada instead of into the US, you can bet TRP will eventually get a pipeline… From the graph found on the next page, you can clearly see that TRP’s pipeline diversification doesn’t stop at Keystone XL or Energy East by any means (source TRP presentation):

In their most recent presentation, TRP expects to double its dividend growth rate from 2014 to 2018. For the past two years, it shows a 4% dividend growth and it should bump up to 8% annually. This wind of optimism is due to successful small to medium-sized projects (e.g. not major pipelines). If this would happen, the dividend growth might grow even stronger post 2018.

Overall, if I had to choose between Enbridge and Transcanada, I would definitely buy TRP. TRP’s fundamentals are stronger, P/E ratio is smaller (62 vs 21) and dividend yield is higher. On top of all this, TRP has a lot of upside potential in the event of one of the two major pipelines get approved.