Exactly 3 years ago, I was launching a dividend growth investing service called Dividend Stocks Rock. Instead of proving a classic investing newsletter, we have also included a variety of services such as stock card analysis, pre-screened stock lists, a monthly updated buy list along with 12 real-time portfolios. Those portfolios are actively manage and members receive buy and sell alerts. Most of our portfolios were created in October 2013 and now give us a 3 year return history. It is a good timing for us to review our performance and make some adjustments. I’m offering you the integral of our October Newsletter 2016:

Overall Portfolio Performances

Each month, we will publish our different portfolio returns along with transactions that occurred during the month. Portfolios were created on October 1st, 2013. We usually post our performance at the end of our newsletter. But for our portfolio review, we rather start with the good news.

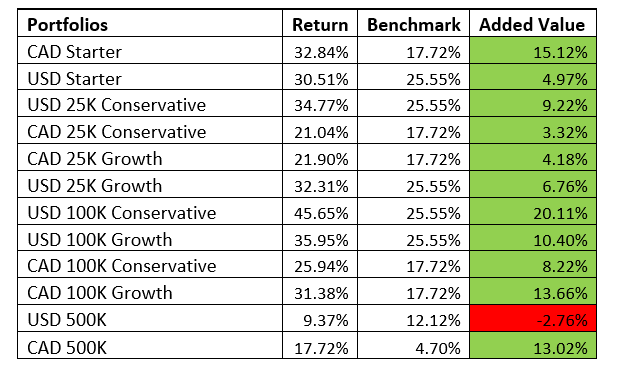

*Canadian portfolios added value is calculated based on 50% of VIG and 50% of XDV as half of portfolios are US stocks. Currency hasn’t been taken into consideration.

After 3 years in operation, we are proud to show strong and consistent added value throughout our portfolios. While we can say that the end of 2013 and the complete year of 2014 were “relatively” easy for investors to make money, it was a totally different ball game for 2015. This is exactly during negative years that you can appreciate the real potential of a strong portfolio.

On average our 4 conservative portfolios showed a better performance (avg of 10.22% over benchmark) than our growth portfolios (avg of 8.75% over our benchmark). As additional volatility gained the stock market, more stable companies have shown to be strong performer.

In the following pages, you will see our year-to-date, 1 year and since inception return for each portfolio. It will give you a better understanding of our performance over the past three years.

There is also an obvious appetite for yield from investors. As we continue to evolve in a very low interest rate environment, more investors resigned themselves to take additional volatility by moving their money away from bonds toward dividend paying stocks.

This situation has helped dividend investors to outperform the stock market and benefit from not only juicy dividends, but also considerable portfolio value appreciation. We don’t expect this trend to be so obvious in the upcoming years. Revenues and profits have stagnated or slightly went down for several companies over the past 2 years. American companies suffered from currency headwinds while international companies had a hard time keeping up with a slowing global demand. The oil industry along with other resources based businesses were hurt by ever dropping commodity prices. Finally, many industrials entered in a down cycle creating buying opportunities for us (such as MMM, UNP and CNR).

The economy has changed greatly since 2013 and it now time to look forward and see how companies will react to factors such as a persistent low commodity prices, slow interest hikes and struggling emerging markets.

At Dividend Stocks Rock (DSR), we do not favor a high trade volume among our portfolios. We rather benefit from the power of dividend growth compounding throughout years. However, this newsletter contains several trades. Our goal is to continue adjusting our strongly built portfolio but we are not chasing returns. DSR portfolios have been built following the 7 dividend investing principles:

- Principle #1: High Dividend Yield Doesn’t Equal High Returns

- Principle #2: Focus on Dividend Growth

- Principle #3: Find Sustainable Dividend Growth Stocks

- Principle #4: The Business Model Ensure Future Growth

- Principle #5: Buy When You Have Money in Hand – At The Right Valuation

- Principle #6: The Rationale Used to Buy is Also Used to Sell

- Principle #7: Think Core, Think Growth

We have made an exhaustive review of each position to ensure that all companies continue to meet our investing principles and are a good fit for our portfolios. In this effort, we hope you will gain a better understanding of how we have built and manage DSR portfolios.

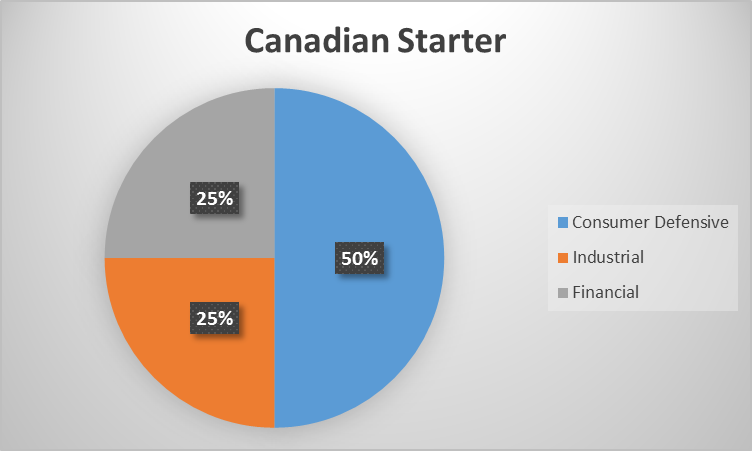

Canadian Starter

The Starter Portfolio shows 4 stocks that have been selected for their geographic diversification and financial stability. These four stocks could be part of the core investing strategy for many investors. These stocks may change faster than other buy & hold portfolios as we want to provide new investing ideas while you grow your portfolio.

Statistics:

Expected starting value for new investors: 1K-10K

YTD Return: 16.64%

1Yr Return: 21.73%

Since Inception: 35.51%

Number of holdings: 4

*Returns are as at October 6th, dividend included, total return

Asset Allocation:

It is difficult to have a diversified asset allocation with only 4 holdings. We have decided to include companies that are strong enough to go through any kind of recessions. While Finning International seemed to be a good pick considering its lower value, it didn’t turn out to be a good choice. For this reason, we will make a transaction in order to improve the portfolio. It’s easy to make mistakes with only four companies.

Comments on Current Holdings

Royal Bank has proven to be a very solid bank during the recent episode of concerns about the Canadian economy. Because RY has built a strong wealth management division and a highly performant capital market segment, RoyalBank was able to post growing revenues and profit. Procter & Gamble has been a steady dividend payer and offer a wide diversification for any starting portfolio. Holding PG in your portfolio is like holding a mutual fund. As for Coca-Cola, we think KO is currently undervalued. The company has made several efforts to improve their presence in the non-carbonated drink business with great success. KO will continue buying growing companies and introduce their products in their impressive distribution network.

Trades

SELL FTT

BUY CNR

We have decided to sell our positions in FTT with no loss after the stock price surged back this year with a +38%. We prefer investing in Canadian National Railway (CNR.TO) for the reasons mentioned in our previous newsletter. CNR evolves in a cyclical market and this is a unique chance of buying this railroad company at a cheap price. Its dividend yield is lower than FTT but it will increase faster in the upcoming years.

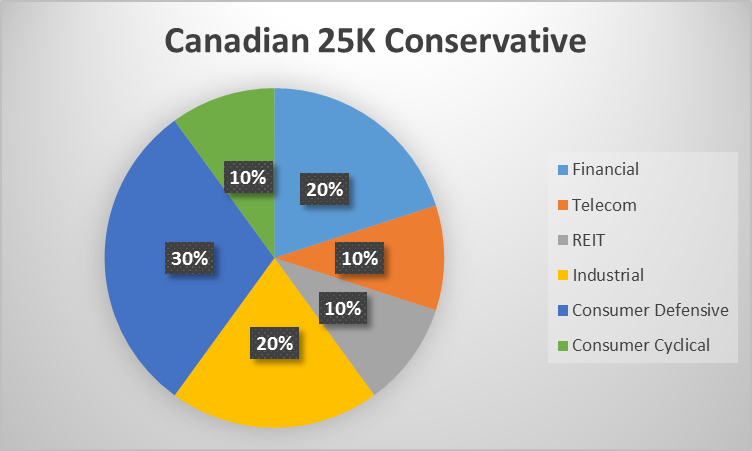

Canadian 25K Conservative

This is an entry-level size portfolio for conservative investors and / or retirees. The idea behind a conservative portfolio is to look for safer companies that will show great value and solid dividend payouts. We are looking for companies that will be less affected by a recession and will continue to offer a constant stream of income.

Statistics:

Expected starting value for new investors: 10K-100K

YTD Return: 14.47%

1Yr Return: 19.45%

Since Inception: 21.17%

Number of holdings: 10

*Returns are as at October 6th, dividend included, total return

Asset Allocation:

The idea when building a conservative portfolio is not really to beat our benchmark, but rather offer a smoother progression of capital through time. This is why there are 30% of the portfolio is invested in the consumer defensive sector and 20% in industrials. The idea is to provide a solid base that can go through all kind of situation. The 20% in the financial industry is also fairly stable and it is the same thing with the telecom (10%) and REIT (10%) allocation.

Comments on Current Holdings

As a leader in the REIT industry, RioCan provide not only a strong dividend yield (5.41%) but also offer investor with a great stability in the shares value. This is a similar situation with BCE that pays 4.55% yield and granted investors with a positive return of 12% this year. Both companies will continue to provide solid payouts to their shareholders. Many members wonder why we invest half of our Canadian portfolio in U.S. stocks. This is because the U.S. stock market offers a wider diversification. It is impossible to find companies that are as geographically diversified as PG and KO for example.

Trades

SELL AFN

BUY EMA

We decided to sell AFN mainly because the company is struggling to post profit and the short term situation will not likely improve. Instead of suffering from a potential dividend cut, we have decided to sell our shares and buy a more solid holding in Emera (EMA). Emera will not break any records, but it is set to continue increasing its payout for several years in a row.

SELL WMT

BUY CL

On the U.S. side, we have decided to get rid of Wal-Mart. This wasn’t an easy decision but the future of this company seems uncertain for us. The dividend payment is far from being threatened. However, we notice that growth vectors become rarer. The only option WMT has is to go more aggressively online and compete with Amazon (AMZN). WMT recently bought Jet.com for 3B$ and will continue to invest massively to gain market share in the future of shopping. This seems like quite a challenge to us.

On the other end, we decided to buy Colgate-Palmolive (CL) in this portfolio. CL has been around for so many years that it makes it very difficult for consumers to think of another brand when it comes to picking toothpaste. Management has done an incredible job in improving the company’s gross margin from 38% in 1984 to 59% in 2015. The decision of creating new local products to dominate each specific market gives another edge to the company. In other words, we think CL shows interesting growth vector for the future while remaining a solid consumer defensive pick.

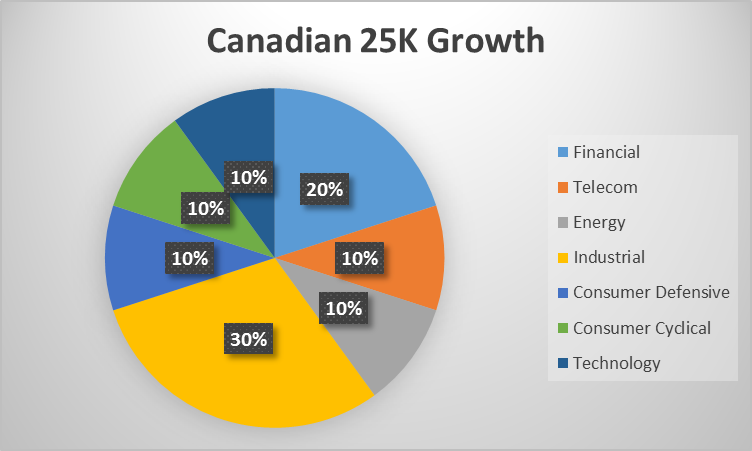

Canadian 25K Growth

This is an entry level size portfolio for investors looking for both dividend and growth stocks. We start with the idea that the most profitable companies and best investments are dividend payers. We also look at companies that have found a balance between above average growth in the business model while paying healthy distributions.

Statistics:

Expected starting value for new investors: $10K-100K

YTD Return: 6.25%

1Yr Return: 3.90%

Since Inception: 23.10%

Number of holdings: 10

*Returns are as at October 6th, dividend included, total return

Asset Allocation:

We have minimized our expositions to both consumers defensive and consumers’ cyclical sectors in order to leave more room for higher growth sectors. We have selected growing companies in the industrial sectors as long with more aggressive pick in the energy and technology industries. We believe there is a stronger growth potential on the U.S. stock market and this is why we have 50% of our portfolio invested in U.S. companies. Please note that U.S. dividend payments are not taxed in within RRSP accounts.

Comments on Current Holdings

We are quite satisfied with our picks in this portfolio. Once again, we have proved that picking low dividend yield can pay over the long haul. Lassonde Industries (LAS.A.TO) is up by 32% in 2016 and the company has increased its dividend by 24% in May. While the stock shows a shy 1% dividend yield, the payout went from $0.30/share quarterly to $0.51/share in 5 years only. With a payout ratio of 19% and a cash payout of 12%, you can expect additional dividend increase in the upcoming years.

We continue to follow closely the situation with Gluskin & Sheff (GS.TO). The company struggled to post growth this year and their special dividend has been greatly diminished compared to the past couple years. Nonetheless, the stock price is now very attractive for a merger or an acquisition. In the meantime, shareholders still enjoy a 6%+ dividend yield.

Another company we keep a close look at is WSP Global (WSP.TO). The company is doing well and we are confident it will continue its growth. However, the dividend payment has remained stagnant for the past couple years. If this situation doesn’t change soon, we will proceed with a sale as our main focus remains dividend growth.

Intact Financial continues to post solid results in 2016 and rewarded their shareholders with a dividend increase of 9%. IFC.TO shows a great mix of growth perspective and consistent income. Since the company didn’t suffer any major natural catastrophe this year, results for 2017 should even get better.

On the U.S. side, Apple (AAPL) is recuperating from a difficult 2015. Investors now see that AAPL could generate additional revenues from its side businesses such as Apple Pay, Apple Music, etc. The launch of the iPhone 7 should bring additional money in Apple’s already well-filled bank account.

Finally, Disney (DIS) seems to show a good buying opportunity at $91.50. The company is poised to publish strong revenues and profits in 2017 as their movies and theme parks divisions show impressive growth. ESPN continues to be the black swan of Disney business profile but there is a lot more to get from this company than its sports media division.

Trades

There will be no trade at the moment.

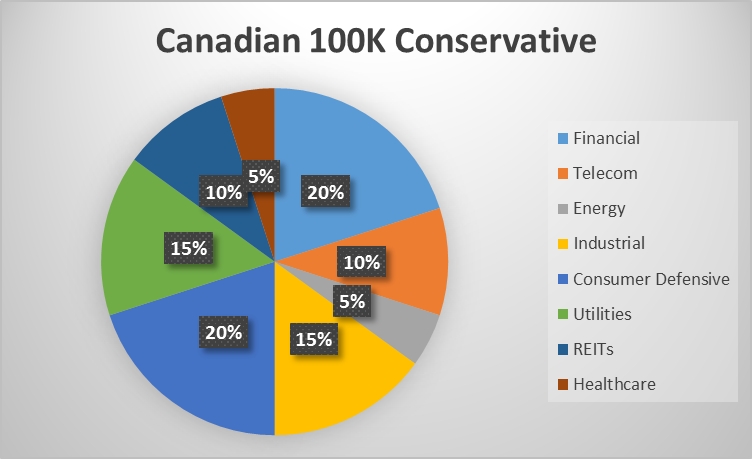

Canadian 100K Conservative

This is a complete portfolio for conservative investors or retirees. Since the portfolio includes 20 stocks, the minimum investment suggested in our opinion is 100K. Therefore, you could easily use this portfolio if you have 300K or 500K to invest. The idea behind a conservative portfolio is to look for safer companies that will produce great value and solid dividend payouts. We are looking for companies that will be less affected by a recession and will continue to offer a constant stream of income.

Statistics:

Expected starting value for new investors: 100K-500K

YTD Return: 12.20%

1Yr Return: 20.62%

Since Inception: 24.84%

Number of holdings: 20

*Returns are as at October 6th, dividend included, total return

Asset Allocation:

With 20 holdings in this portfolio, it becomes easier to have a great asset allocation among various sectors. We have 15% in utilities and 10% in REITs to add steady income with relatively higher yield. The financial sector shows 20% as we included 3 Canadians banks and Black Rock, the world largest asset manager.

Comments on Current Holdings

We decided to own 3 Canadian banks and 2 Telecoms as it is the core of the Canadian stock market. By selecting the two biggest banks (TD and Royal), we ensure to cover a large portion of the financial sector. Both banks are doing well in 2016 and will continue to offer a great stability. As for ScotiaBank, the company offers a great diversification away from the Canadian economy. It is true BNS.TO struggled with their Latin America division lately, but the storm seems to be behind us.

BCE and Rogers offer another great dividend pillar in this portfolio. As they evolve in the same oligopoly, their performances are somewhat related. Both BCE and Rogers made efforts in the past couple of years to diversify their telecom services with additional TV services. Their dividend payment will continue to increase and will reward investors with 4.50% (BCE) and 3.50% (RCI.B) dividend yield.

Finning International (FTT.TO) has been the best performing Canadian holding in 2016 with +34%. The company struggled in 2015 (-25%) due to a difficult year for the Canadian resources sector. While the oil industry is going through a challenging period, the mining sector isn’t going great either. However, it seems that the worst has been put between us with this year results. However, we will continue to follow the situation closely as FTT didn’t increase their dividend by much (?0.50).

Boardwalk (BEI.UN) has a good run on the stock market, but their results haven’t been that strong. The company posted decreasing occupied rent by -5.1% mainly due to their property in Alberta. We can expect a similar scenario in 2017. The dividend payment remains under control with a AFFO payout ratio of 78%. We don’t expect much growth from this REIT, but we will continue to benefit from a stable dividend payment.

Trades

SELL WMT

BUY CL

See comments in the Canadian 25K Conservative portfolio.

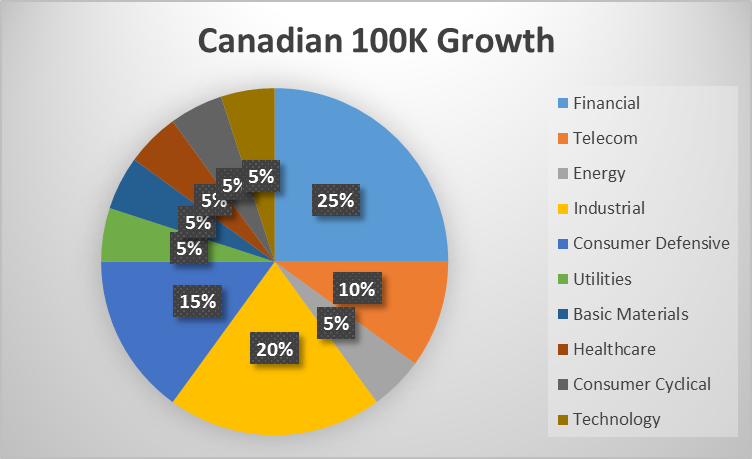

Canadian 100K Growth

The ultimate dividend growth machine portfolio. With a maximum of diversification, this portfolio is made for those who are looking to make some real money with dividend stocks. The portfolio currently shows 20 positions in different sectors. Since the portfolio includes 20 stocks, the minimum investment suggested in our opinion is 100K. Therefore, you could easily use this portfolio if you have 300K or 500K to invest.

We tend to benefit from the timing of performing sectors to improve the overall portfolio return. The dividend growth portfolio series will include more regular updates as we want to make sure to pick all the best buying opportunities. The idea is to keep a core portfolio as a “buy & hold” strategy and benefit from the dividend growth compounding effect while buying and selling stocks timely according to what is happening on the market.

Statistics:

Expected starting value for new investors: 100K-500K

YTD Return: 11.44%

1Yr Return: 12.47%

Since Inception: 30.61%

Number of holdings: 20

*Returns are as at October 6th, dividend included, total return

Asset Allocation:

We took the opportunity to hit various sectors with the energy, utilities, basic materials, healthcare, consumer cyclical and technology for 5% each of the portfolio. This gives us a great diversification while position the portfolio to benefit from various market segments. While we have 15% in the consumer defensive sector, we believe those 3 companies (Lassonde, Pepsi and Cal-Main) show great growth potential.

Comments on Current Holdings

Emera (EMA.TO) has been a solid pick since the very beginning. The company shows a great combination of sustainable cash flow and growth perspective (through their U.S. acquisitions. The company pays a 4.50% dividend yield while trading under a 15 PE ratio.

We will follow the imminent merger between Agrium (AGU.TO) and Potash (POT.TO) in the upcoming years. We believe it will be beneficial for our holding and that Agrium should gain in value after the merger occurs. Nonetheless, our focus will remain on their dividend policy (keep in mind Potash cut theirs not so long ago).

National Bank stock has been doing great this year with a +12% ytd. Both capital market and wealth management continue to perform well while we saw steady revenue growth form the personal & commercial banking (more classic business) division. The bank already increased their dividend by $0.01 this year and should perform another dividend raise after publishing their year-end results.

Calian Group (CGY.TO) stock has been skyrocketing in 2016 (+45%). This is mainly due to very strong results and record quarters. The company posted increase of 14% in revenue for the first 9 months of 2016 and 36% for EBIDTA during the same period. The company also announced the renewal of various contracts ensuring consistent cash flow in the upcoming years.

On the U.S. side, Cal-Main (CALM) has recently announced it will not pay any dividend for its recent quarter. Some may wonder why it is still part of our portfolio. The reason is simple; CALM dividend policy is different from most classic dividend payers. Management doesn’t issue dividends if the company doesn’t generate profit. Since the company already paid more money with its first 3 quarters this year than in 2015, we don’t mind this pause. In fact, it sounds more conservative to approach dividend payments this way.

Trades

No trade at the moment.

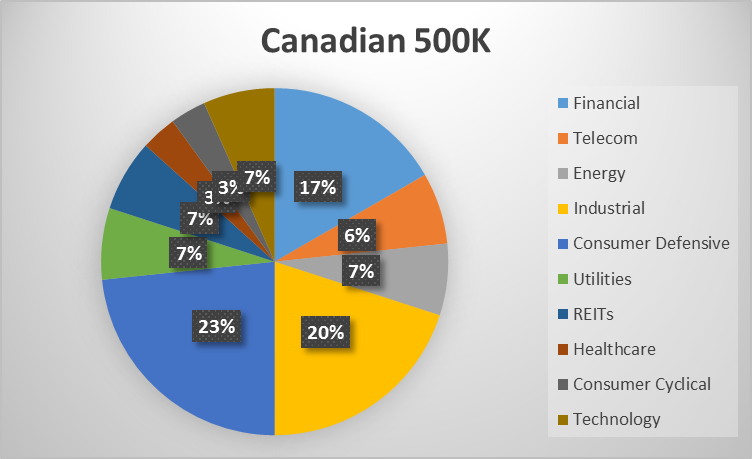

Canadian 500K

This is our biggest portfolio. It can be used for all portfolios over 500K. We decided not to create a growth or conservative but rather a complete 500K portfolio. In order to make sure we cover both growth and revenue part of a portfolio of that size, we added a few ETFs generating revenues. You can then increase the portion in ETFs if you wish a more conservative portfolio or simply ignore the last few lines and concentrate on the stocks if you seek more growth than revenues.

Statistics:

Expected starting value for new investors: 500K+

YTD Return: 12.32%

1Yr Return: 15.70%

Since Inception: 17.68%

Number of holdings: 30

*Returns are as at October 6th, dividend included, total return

Asset Allocation:

The 500K achieves a great balance between growth and conservative holdings. With a solid core dividend among Canadian financial market, U.S. consumer defensive and strong industrials from both borders, The Canadian 500K portfolio shows a strong potential for both growth and dividend growth in the upcoming years. While we hold 6 companies in the industrial sector, only 2 of them evolves in the very same sector (railroads).

Comments on Current Holdings

When you hold 30 different companies, you can afford having some with very low dividend yield such as Alimentation Couche-Tard (ATD.B.TO). We have selected this company mainly for the fact that it evolves in a consumer defensive market, but the company shows a very strong appetite for growth. The stock surged over 500% over the past 5 years and we believe Couche-Tard will be able continue its growth by acquiring more convenience store and merging them into its lucrative business model.

Canadian National Railways (CNR.TO) has been added to several of our portfolios this year. This is because we believed it was the right timing to do so. Railroads evolve in a cyclical segment of the market. When they are down (as they were in 2015), it was the right time to pull the trigger.

Parkland Fuel (PKI.TO) is an independent fuel distributor in Canada. The stock jumped this year (+32%) after entering in an agreement with Alimentation Couche-Tard to buy all Canadian asset based from CST (as Couche-Tard is buying the U.S. assets). With this transaction, PKI Becomes Canada’s largest fuel retailer, with more than 1,555 sites in communities across Canada. It will also expand its retail geographic coverage and presence in Québec and Atlantic Canada, two regions that are less affected by the oil industry.

On the U.S. side, Helmerich & Payne (HP) is finally coming back from the dead. It was a long 2 years of stock dropping and bad news, but HP is now up +28% in 2016 mainly to the oil rebound. Management even kept its 43-year streak with a consecutive dividend increase by giving an extra $0.01 to its shareholders.

Trades

SELL WMT

BUY CL

See comments in the Canadian 25K Conservative portfolio.

DSR 2 Year Promotion

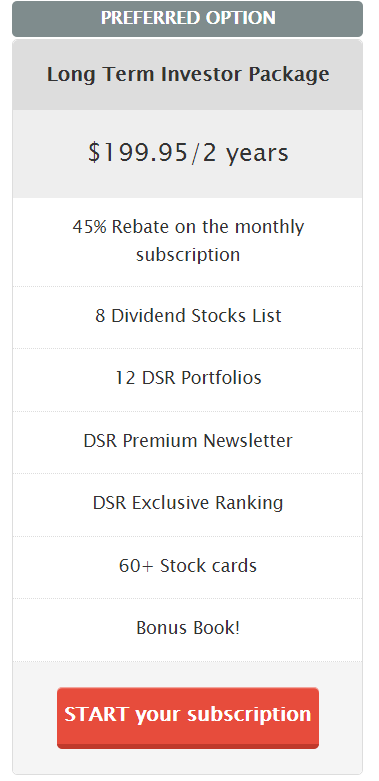

As you can imagine, this article is long enough, I couldn’t post my U.S. portfolio commentary. However, if you go back up to the first chart of this article, you will see that 11 of our 12 portfolios beat our benchmark over the past 3 years. If you want to look what’s inside DSR hood and have real access to our portfolios (not just the commentary), you can register for a special rate of $199.95 for 2 years. The best part is that you can try it without any worries; I will refund you within the first 60 days of your purchase if you are not satisfied.

Join thousands of investors performing: