We have been walking in the dark for several weeks. While the market tried to guess where the pandemic would lead the economy, we barely received any data to confirm or deny our hypothesis. We knew jobless claims would skyrocket but that doesn’t tell us how many real jobs will be lost.

As we move forward with the second earnings season of the year, CEO’s comments on their businesses will be crucial in our decision-making process. Remember: power is knowledge.

Let’s look at two Canadian companies that have seen their stock prices plummet since the beginning of the year. Those are obviously riskier plays, but those risks could come with great rewards down the road.

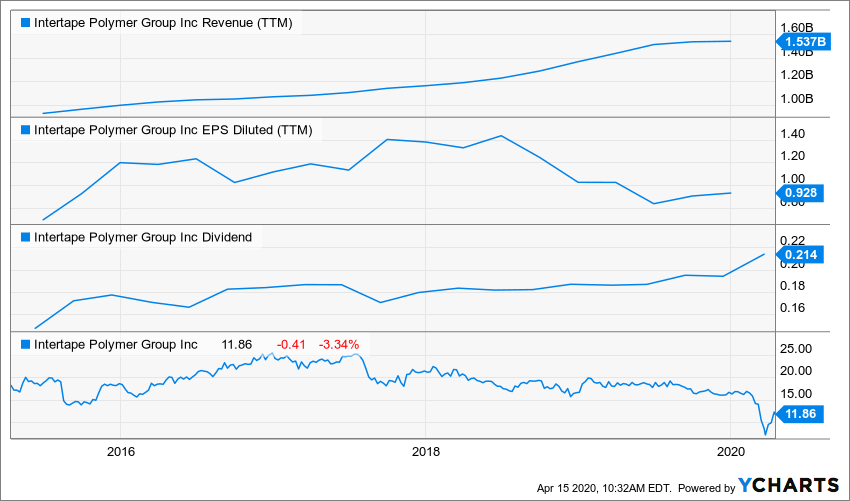

INTERTAPE POLYMER (ITP.TO) -22%

The Company in a Nutshell

- ITP is known for its growth by acquisition strategy.

- ITP is a leader in the tape industry: 67% of its revenue, generated by top #1 or #2 brands in North America.

- Intertape Polymer makes one of my favorite products for RVing… Duct Tape! But ITP has a lot more than this famous product to offer to investors.

Business Model

Intertape Polymer Group Inc manufactures and sells a variety of packaging products. The firm’s primary product categories include tapes, films, and woven coated fabrics. The company’s tapes include pressure-sensitive and water-activated carton sealing tapes, and flatback, duct, double coated, foil, electrical, and filament tapes. Intertape’s film products include stretch wrap, shrink film, air pillows used for protective packaging, and packaging machines. The woven coated fabrics include building and construction products and specialty fabrics. Most of the revenue comes from the United States.

What could go wrong?

For a company that has just contracted for substantial debt in 2019 to make several acquisitions, you can expect that the arrival of a global recession isn’t the best timing. ITP’s plan is all about acquisitions to reach its 2022 target. At this point, the market is worried management won’t be able to reach their targets and may not generate the expected synergies from its previous business moves. ITP expects to use cross-selling among its businesses to boost their revenue. Their customers may not jump on the buy button right away to increase their orders considering the current economic situation.

What could go right?

ITP’s CEO went public recently to calm down investors. This is a perfect example of how clear information can change our perceptions. After confirming that half of its business was thriving (ecommerce and food packaging), the CEO confirmed he sees no point in changing their 2020 guidance. It was “business as usual” since some business segments compensated for others. The stock jumped by more than 20% since those pronouncements by the CEO.

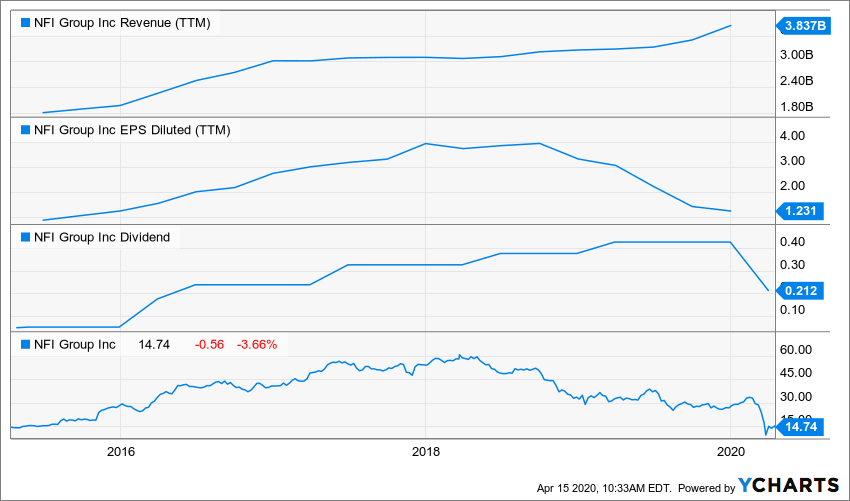

NFI GROUP (NFI.TO) -48%

The Company in a Nutshell

- NFI shows a major strength in manufacturing zero-emission buses (ZEBs).

- As the cost of transportation keeps rising, ZEBs are definitely a market with growth perspectives.

- NFI is a true leader in its market with a 45% market share in heavy-duty transit buses and 39% in motor coaches.

Business Model

NFI Group Inc is a Canadian automobile manufacturer. The company organises itself into two segments: manufacturing operations and aftermarket operations. Manufacturing operations, which represents more than half of the company’s revenue, includes the manufacture of transit buses for public transportation, and motor coaches. Aftermarket operations includes spare parts and servicing related to transit buses and motor coaches. The company’s fabrication, manufacturing, distribution, and service centers are located both domestically and in the United States, with the majority of its revenue derived from operations in the U.S.

What could go wrong?

I recently covered NFI Group for my DSR members since the company announced a dividend cut of 50% as production idled across all segments. The business continues to provide minimum support and deliver parts, but the bulk of its activities are closed. As NFI has plants in Europe, UK and North America, the company must face various limitations according to each country. Overall, they announced they would pause their production until May. NFI recently made a major acquisition (Alexander Denis) and in retrospect that acquisition was possibly ill timed.

What could go right?

Most NFI’s revenue (70%) is driven by public transit agencies. The company has a strong backlog of 4,000+ buses and most of them will be delivered since cities continue to need transportation. Since government supports such purchases, you can expect more money to be spent there as a stimulus to restart the economy. NFI’s April COVID-19 update mentions that the company had enough liquidity to work through this crisis and currently is exploring more options through their bank and the Government.

Conviction for the Long Run

There are two strategies you can use to determine your next move. One is based on the current stock price and how it lost value. The other is based on the fundamental reason why you might add (or not add) this company to your portfolio. While the first strategy is widely used among investors, I prefer the latter. A strategy based on an investment thesis will always provide you with great confidence in your picks and will reduce some of the emotions attached to trading. Therefore, it’s always the time to invest according to DSR’s principle.

Since those stocks haven’t recovered their losses, this is a great opportunity to combine both the price and investment strategies together. Keep in mind these are long-term plays. Don’t expect short term gains.

The post Canadian Biggest Losers: Is it Time to Capture These? appeared first on The Dividend Guy Blog.