Brookfield stocks have reported robust performances for several years. Most of them trade on both the Canadian and U.S. markets and offer generous dividend payouts.

However, understanding the differences between Brookfield Infrastructure, Renewable, Properties or Asset Management could be a real puzzle to solve. It has become even worse after the company created new share classes last year for three of its “family members”. Which type of shares should you hold?

Brookfield Asset Management (BAM) (BAM.A.TO)

To keep things simple, we will refer to each company by their “simplest” ticker:

- BAM: Brookfield Asset Management

- BPY: Brookfield Property

- BIP: Brookfield Infrastructure

- BEP: Brookfield Renewable

- BBU: Brookfield Business

*Please note that all companies trade on both the Canadian and U.S. markets, but they all pay their dividends in USD.

BAM’s story traces back to 1899. The company was founded in 1899, as the São Paulo Tramway, Light and Power Company by William Mackenzie and Frederick Stark Pearson. It took the name Brookfield Asset Management in 2005.

Today, BAM is a world-class asset manager with nearly 2,000 employees managing almost $600B in assets. The firm specializes in “alternative assets” management. Alternative assets are those which cannot be categorized as stocks, bonds, or certificates. BAM has become a master in investing in complex projects that require sizeable amounts of money to be “parked” for a very long time. You can consider hydro-electricity plants, wind or solar farms, toll roads, bridges, pipelines, railroads, data centers, healthcare facilities, and large office buildings as examples of these alternative assets.

Such investments require unique expertise and, while they are operating in various industries, all share many characteristics:

- Large projects with several layers of complexity.

- Money must remain invested for decades to generate substantial cash flow.

- Most projects will perform well over time.

- They are not generally considered to be liquid assets that can be easily sold.

- Most projects won’t be greatly affected by economic cycles. They tend to be recession-resistant.

From a portfolio management perspective, investing in alternative assets is a great way to diversify your portfolio. Typically, the investment returns on such investments will not be determined by what is happening on the stock market. You can expect they will generate about 5-7% above inflation over long periods of time.

The problem for a retail investor is quite simple: it’s virtually impossible to buy a piece of a bridge or a railroad. This is where BAM comes into play as investing in BAM is like investing in your own “alternative asset fund”.

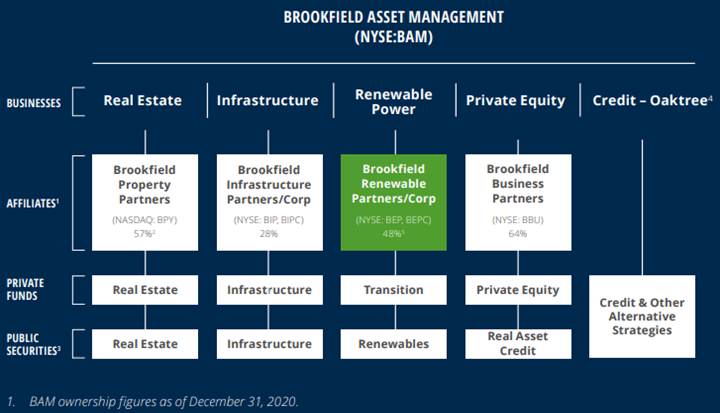

BAM’s structure is relatively complex as the company has stakes in all “Brookfield family members”:

Source: BEP Dec 31 2020 investor brochure.

If you have spare time, you can fill that time by following’s BAM’s multiple projects. According to their investors’ presentation (August 20th, 2020), the company raised over $48B, deployed (e.g. invested) $42B and realized (sold assets) $16B in the previous twelve months. These transactions include the acquisition of the India Telecom Tower Business for $7.6B, the refinancing of the One Manhattan West building ($1.8B), the privatization of TerraForm Power ($11B in assets were privatized). Speaking of privatization, BAM is currently in the process of buying back all outstanding shares of Brookfield Property Partners (BPY). This remains an open offer at $16.50 USD per share with no deadline.

The company currently has about $76B in liquidity to finance its projects. No doubt, they mean business. BAM will receive large amounts from institutional investors (banks, pension plans, etc.) to invest in alternative assets. They have their own funds and they also created several companies (BPY, BIP, BEP and BBU). Soon, BAM will also launch a reinsurance business (Brookfield Asset Management Reinsurance Partners) in 2021. All “Brookfield family members” are at least partially owned by BAM and pay a dividend. Therefore, BAM has created its own dividend fund across its multiple businesses.

In a situation where interest rates are close to zero, BAM is like a kid with $1,000 in a candy store. The company can easily use leverage to finance its capital-intensive projects and support its “children”.

Who should consider BAM?

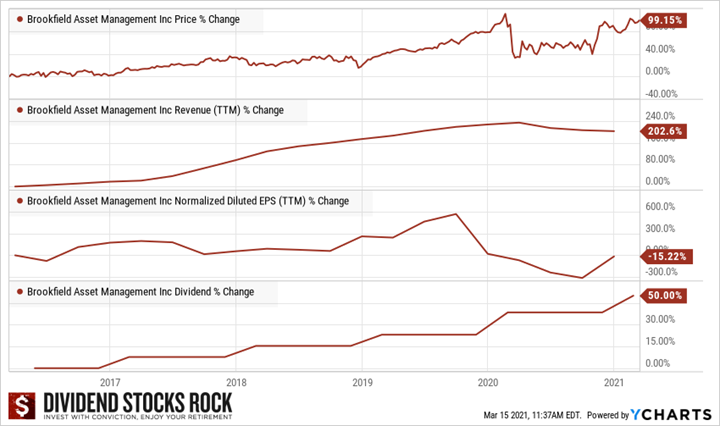

BAM trades on both the Canadian and US markets (BAM.A.TO or BAM) and offers a 1.2% dividend yield. The dividend is paid in USD and has been increased yearly since 2012. Investing in BAM will provide you access to alternative assets, an asset class that is virtually impossible to acquire if you don’t go through packaged investment vehicles (such as ETFs or mutual funds). You will not get much from its yield alone, but the total return (dividends plus capital gains) on such a play is interesting. Among Canadian-based asset managers, BAM is somewhere between Berkshire Hathaway and BlackRock. BAM is an excellent fit for growth investors, but also offers robust long-term stability.

When analyzing BAM, one should ignore their earnings per share. The company is operating too many different transactions affecting their earnings in a single year. Tracking funds from operations (a non-GAAP measure) will give you a better perspective. This number can be found in each company’s quarterly earnings report (highlighted at the top of their press release).

Partnets, Trusts, and Corporate Shares?

In 2020, Brookfield decided to create a new type of shares for BPY, BIP and BEP. Historically, all companies were trading on both the Canadian and U.S. markets under a Trust (Canadian) or a Limited Partnerships (LP) (U.S.). I’m not going into the tax details here because a) I hate taxes (and you should too) and b) I leave this field of knowledge to accountants and tax experts (and, again, you should too).

Long story short, Trusts and LP’s distributions are taxed differently in a taxable account. For this reason, this type of asset is usually less popular among retail investors, ETFs, and mutual funds due to their tax complexity. To ensure more flexibility and liquidity, Brookfield decided to create corporate shares (C shares). The idea was to increase its appeal to U.S. retail investors because of more favorable tax characteristics.

Therefore, all the family members received their corporation share tickers for both the Canadian and U.S. markets. This created much confusion at first as we now have 3-4 different tickers per company:

| COMPANY NAME / TYPE | LIMITED PARTNERSHIP (LP) | CORP. (U.S.) | TRUST (CDN) | CORP. (CDN) |

| Brookfield Property | BPY | BPYU | BPY.UN.TO | * |

| Brookfield Infrastructure | BIP | BIPC | BIP.UN.TO | BIPC.TO |

| Brookfield Renewable | BEP | BEPC | BEP.UN.TO | BEPC.TO |

*Brookfield Property kept the trust units in Canada as it is already treated as any other REIT.

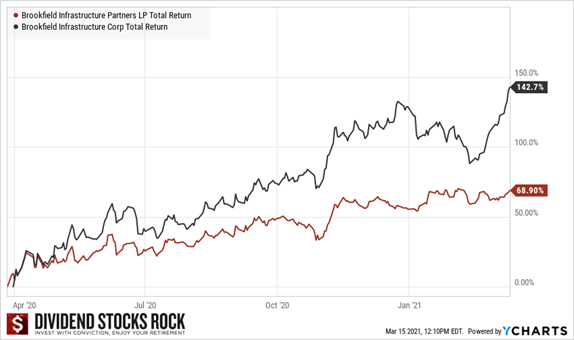

All entities are economically equivalent. However, we noticed an important difference between the performance of the new “C” shares vs the “old” tickers since their inception.

The difference in price is explained by the unexpected level of interest for the corporation shares. As demand increased for the corporate shares, all Brookfield C shares appreciated in price faster than the trust and LP units.

Are corporation shares better then?

Many investors asked me if they should shift their money into the corporation shares. I can’t tell you what to do with your investments (remember, I’m not your broker or your personal advisor). However, I can tell you this: it seems that if you are more interested in total returns and you don’t mind receiving a smaller dividend yield, the corporation shares may be the better option over the long haul. Going forward, demand is likely to remain stronger for the corporation shares because they are easier to trade and deal with the tax implications than the LP or Trust units.

Units will likely pay a higher yield as is the case now. Right now, the difference is important for BIP and BEP:

- BPY: 7.47% vs 7.33% for BPYU

- BIP: 3.83% vs 2.68% for BIPC

- BEP: 3.03% vs 1.94% for BEPC

**Please note that there are also tax implications. I strongly suggest you revise this aspect with a tax expert or accountant. There are tax implications for having LPs in retirement accounts for investors**.

Is it the end of the world if I keep my investment as is?

While these modifications could raise eyebrows for investors, keep in mind that all tickers have been created to reflect the value of the same company. Therefore, it’s not a major mistake to hold one ticker and not the other (or maybe you kept both since you received new shares in the stock split process).

At DSR, we have shifted toward corporation shares for our “regular portfolios” (25K, 100K or 500K), but we focused on units (LPs or Trust) for our retirement portfolios. The rationale is quite simple: corporation shares should bring a higher capital gain (e.g. more demand) and lower yield (higher stock price) while units will bring more income and price stability. This is what we want inside of a retirement portfolio, right? (Then again, beware of tax implications).

We have reviewed each of the Brookfield businesses for our DSR members. Here’s an example of what we shared in the newsletter.

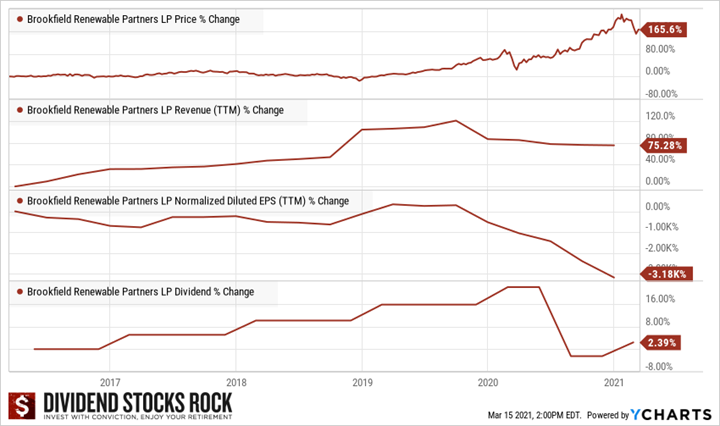

Brookfield Renewable (BEP) (BEPC) (BEP.UN.TO) (BEPC.TO)

BAM ownership-48%

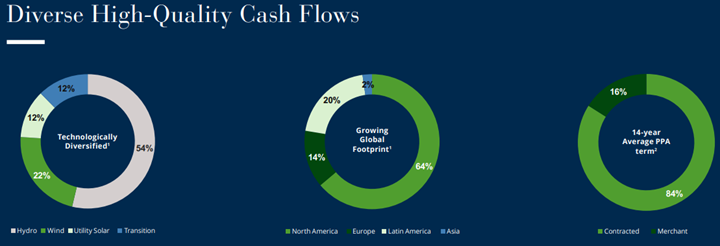

BEP operates one of the world’s largest publicly traded renewable power platforms. Its portfolio consists of approximately 20,000 MW of capacity and over 5,300 generating facilities in North America, South America, Europe, and Asia. Its investment objective is to deliver long-term annualized total returns of 12%–15%, including annual distribution increases of 5–9% from organic cash flow growth and project development. The company is a global leader in hydroelectric power, which comprises approximately 66% of its portfolio. It is also an experienced global owner and operator of wind, solar, distributed generation, and storage facilities. (BEP investor website)

Like BIP’s business model, BEP is also operating across multiple business segments:

| HYDRO | WIND | SOLAR | STORAGE | DISTRIBUTED GENERATION |

| 7,900 megawatts | 5,500 megawatts | 2,100 megawatts | 2,700 megawatts | 1,200 megawatts |

Source: Investor brochure

Moving forward, BEP will improve its diversification with major investments in wind and solar energy. The company currently shows a project pipeline of 23,000 megawatts with more than 75% in wind and solar energy. As is the case with other Brookfield members, you are better off tracking its funds from operations than its earnings per share.

BEP investing narrative

Like BIP, BEP offers a great diversification for investors when it’s time to select a renewable energy producer. BEP shows about 55% of its activities in North America, opening the door for good geographic diversification. The company is on its way to more than double its energy generation capacity once it completes its development pipeline.

After an impressive stock price surge, the stock appears to be taking a break. While the stock is cooling down, there is nothing to worry about. The rise of interest rates on bonds combined with the incredible ride BEP has had over the past 12 months are responsible for this small correction. You can’t expect stocks to always go up.

I’ve also covered BAM’s offer to buy all the remaining unit of Brookfield Property Partners (BPY, BPY.UN.TO, BPYU) in the video below.

Final Thought

After looking across all Brookfield businesses, we think the most interesting investments today are BAM, BIP and BEP. The fact that there is a close link between the three of them may create a break to buy the whole package. If anything major happens to BAM, it will likely have an impact on BIP and BEP.

Also, you may prefer to own utilities that are specialized in a specific activity or in a specific region. While there is a great advantage to diversification, we have seen many cases where management spreads itself too thin and loses control of its operations

I expected this newsletter to shed some incremental light on the Brookfield family of companies.

The post Brookfield Stocks: Which Type of Shares Should You Hold? appeared first on The Dividend Guy Blog.