Since the Canadian interest rate environment will continue to be as exciting as a worm race across the garden, I thought of revisiting a two very popular Canadian REITs.

Boardwalk REIT (BEI.UN)

RioCan REIT (REI.UN)

Canadian REITs have been a strong source of steady income for investors for several years. While they don’t show spectacular stock price growth or even dividend payment growth, this asset class is still a must for all conservative and income seeking investors. For example, both BEI.UN and REI.UN have been issuing a monthly dividend payment for more than 10 years to their shareholders. Not a single time was the payment late or diminished, this is probably a better batting average than most landlords

Boardwalk Vs RioCan Business Model

In a few words, RioCan is 353 retail properties in Canada and USA with 7,600 tenants and 86% of their revenues are paid by important companies (national and anchor tenants). RioCan has well known tenants such as Canadian Tire (CTC.TO), Walmart (WMT), Loblaws (L), Metro (MRU), etc. The bulk of their properties are owned in Canada (305 out of 353) with a massive concentration in Ontario & Quebec they also have several locations in Alberta and BC. The REIT is less exposed to the Western Economy and should not suffered from Alberta’s “recession”.

They have a well-diversified tenant mix concentrated in the retail and grocery business:

Source: RioCan investor presentation

Source: RioCan investor presentation

Another example of how strong and diversified RioCan was the “Target Experience”. As at March 31st 2015, Target (TGT) represented 1.9% of annualized rental revenue. At the beginning of the year TGT announced they were dropping the ball in Canada and closing all their stores. RioCan was secured by their tenant agreement and the stock didn’t budge. Only one lease wasn’t part of an agreement with Target and it was guaranteed by… Walmart.

Each year, management ensures they have about 10% of their square feet up for renewal. Therefore, there isn’t a “crucial year of renewal” coming ahead. Each year is business as usual. The largest proportion to be renewed will come in 2015 on both sides of the border when 12.6% of Canadian square feet leased and 15.2% of US leased will reach maturity.

Finally, the overall occupancy rate is over 96% since 2003 and has never fallen under 96.7% since 2005. It’s retention rate for the first quarter of 2015 stands at 90%.

Conversely, Boardwalk REIT is a lot smaller than RioCan and is operates solely in Canada. 65% of their properties are in Alberta. At a quick glance, we can already put Boardwalk on the watch list considering what is happening in Alberta right now. However, as oil prices evolve rapidly, we might have another story to tell 6 months from now. This is why I’ll continue digging.

Source: Boardwalk investor presentation

Source: Boardwalk investor presentation

While RioCan operates in the retail sector, Boardwalk is a multi-family residential Real Estate company. BEI.UN owns over 225 properties with 35,277 residential units for about 30 million net rentable square feet. I like the fact management owns 25% of Boardwalk. That makes management team more accountable for their moves.

Boardwalk benefits greatly from the very low rate interest environment. The company is still renewing mortgages at lower rates than their previous contracts. This is why they have already renewed 42% of their 2015 mortgages due and will save $3.8 million in interest for the next 7 years compared to previous contracts.

The company focuses on vertical integration through bulk purchasing and warehousing parts and supplies. This is cost efficient and improves service to customers. It also takes care of most of their repairs and landscaping tasks in order to keep costs low.

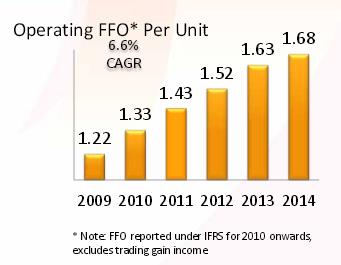

FFO per Unit & Payout Ratio

As you probably know already, REITs are totally different beasts than dividend paying companies. We can’t use the normal payout ratio as REITs are structured to pay a maximum of their profits to their unit holders. Therefore, the good way to look at REITs is to look at their funds from operations (FFO) per unit as well as their distribution. This is how you will calculate the equivalent to the payout ratio. RioCan was nice enough to provide its FFO graph in its latest investor’s presentation:

In 2015, the payout ratio was 88.1%.

In comparison, Boardwalk payout ratio stood at 60.70% in 2014 and will be around 55% in 2015 according to their latest FFO guidance.

While their apartment growth has stagnated since 2005, the FFO per unit has increased drastically. This is definitely linked to the interest rate environment along with tight cost control management.

If we compared both payout ratios, we will notice that RioCan is higher and has less room than Boardwalk for future increases. However, current low payout ratio is mostly due to very low mortgage rates and this situation might turn around quickly as most mortgages are held for no more than 7 years.

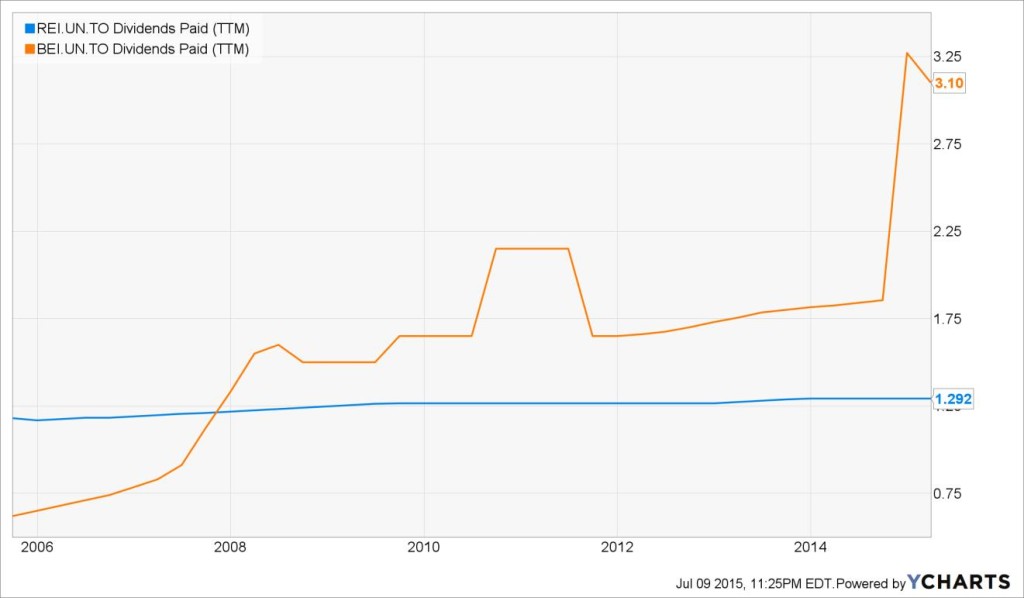

Dividend Yield & Growth

RioCan has barely increased its dividend over the past 5 years with an annualized growth rate of 0.43% while Boardwalk (through special dividends) was able to maintain a 2.43% 5 year annualized growth:

There is probably a small advantage for Boardwalk for paying a special dividend once in a while as compared to RioCan that sticks to a more conventional payment distribution. However, the RioCan yield is over 5% right now while Boardwalk shows a lower yield at 3.40%.

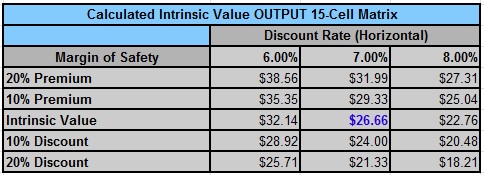

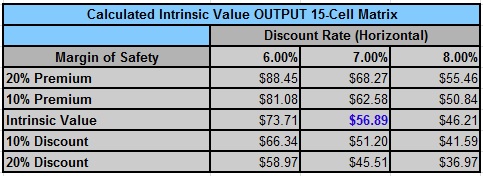

Stock Valuation

When it comes down to stock valuation, I usually use the Dividend Discount Model. What better way to analyze a company than to use the main reason why an investor would pick this stock? But using the Dividend Discount Model is harder in both cases as dividend growth is low to nothing in both cases.

Since the overall risk is very low with such companies, we can’t use the same discount rate as we use for a regular company. The Real Estate business is relatively stable at their size and will not likely fluctuate from one year to another. This is why I’m using a discount rate of 7%, which is definitely lower than my normal range (from 9% to 11%).

For RioCan, I’ve considered a dividend growth of 2.50% for the next 10 years with a drop to 1% afterwards. For Boardwalk, I was a bit more generous as I think the company will be able to raise its dividend (or pay a special dividend) as long as mortgage rates are so low. This is why I use a growth rate of 5% for the first 10 years and decreased it to 2.50% thereafter. In both cases, the stocks seem slightly overvalued.

Riocan:

Source dividend toolkit excel spreadsheet

Source dividend toolkit excel spreadsheet

Boardwalk:

Source dividend toolkit excel spreadsheet

Source dividend toolkit excel spreadsheet

Final Thoughts

After reviewing both companies, I can highlight the main strengths of each of them. Let’s start with RioCan:

#1 High sustainable dividend yield makes it very attractive for income seeking investors

#2 The business model is based on both geographic & tenant diversification

#3 The company has very high quality tenants (many publicly traded companies)

And for Boardwalk:

#1 Cheap interest mortgage renewals improve the company balance sheet year after year

#2 97.8% occupancy level gives them some room for a storm

#3 Even if Alberta enters into a recession, people will have to live somewhere; they are more likely to rent than anything else.

While Boardwalk presents better dividend growth perspective, I think I would pick RioCan if I had to buy one of them today. The reason would lie in a higher dividend yield coupled with a more diversified properties portfolio.

What do you think? Which one is the best REIT in your opinion?