Many investors are obsessed with the timing of their investments. They think they can predict what will happen with the stock market and will find the magic loophole that will make their investment profitable. I find this premise interesting because if there is one thing we don’t control as investors, it’s how the market reacts. Sometimes, there is great news that doesn’t affect the market at all and other times, missing analysts expectations could kill your stock even if the numbers were good. Between you and me, the market is going to do what the market is going to do. There is no rationale explaining why Microsoft (MSFT) went from $75 to $110 in less than a year. Once you have picked a company that you like and have written down your investment thesis, you can only wait and watch your portfolio. While you can’t control the market, there are things that are fully under your control. This is where you should put all your attention.

Your saving rate

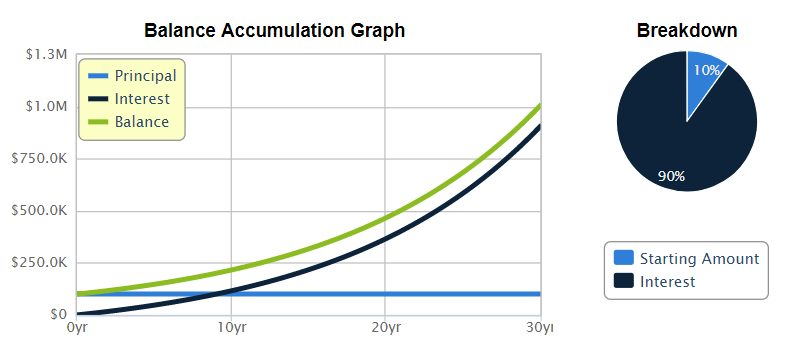

The amount of money you save to invest in the stock market is probably the most powerful tool you possess to reach your investment goal (or FIRE!). The internet is filled with great example of bloggers who saved 40, 50, even 60% of their income to invest in the market and retired early. Want to reach $1M in your account? If you have 100K to invest today you will need to average an 8% return over 30 years to reach it:

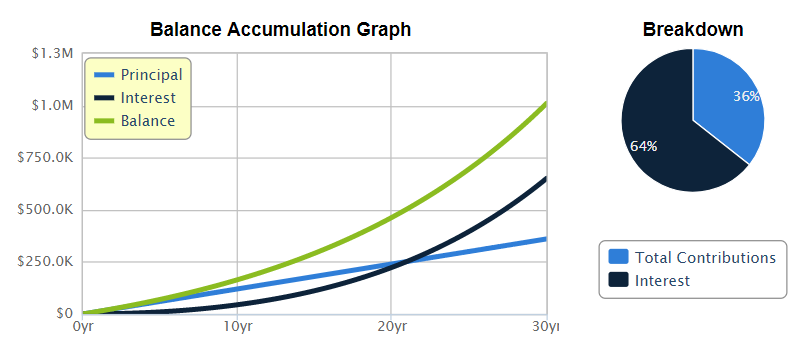

Or you can start with $0 today and save $1,000 a month at 6.2% return (a lot more realistic) and get to the same amount in 30 years:

Source: Calculator.net

Now, imagine that you have the 100K and you save $1K per month today… yup, you’ll end-up a multimillionaire in 30 years.

Your asset allocation

During my financial planning career, I’ve met with many investors with sour investing stories to tell. Many of them got “fooled” and “lost almost everything” on the market. Stats on DIY investors tend to corroborate those horror stories where most investors are not able to match the stock market returns. But when you dig a little deeper you understand why:

- They invested massively in tech stocks in 1999

- They sold everything in January 2009 to put their money into gold (ah!)

- They thought the energy sector was the greatest place to invest 50% of their portfolio

Do you see the point? The market has gone through various crashes and follows a cyclical trend. Each crash hurt a specific sector. If you are wise enough to control your emotions (stay invested) and diversify your portfolio across many sectors, you don’t have to fear anything. In 2008, my portfolio went as low as -27% while the S&P 500 was losing 50%. Then, in 2015 and 2016, we had quick dips of about 10-15% but I didn’t even feel it. Am I a genius or a market guru? Far from it. I just make sure that I pick companies I love in many different sectors. Therefore, there is always something going up while another industry is going down in my portfolio. Are you curious about my current asset allocation? You can check my pension account here.

Your investing strategy

Along with your asset allocation, another thing that is fully under your control is your investing strategy. I’m always surprised to see how many investors don’t have one written down. I have mine all written down and based on decades of experience investing along with numerous academic studies.

The most important point is to write it down and know why and when you invest. Once you have done that, the hardest part is to follow your plan no matter what is going on the market. There is no point in having an investing plan if you don’t follow it, right? Believe it or not, many investors forget about their own strategy when the market gets shaky.

Taxes you are going to pay

It is almost impossible to predict which kind of return your portfolio will show in 20 years. However, you know to the penny how much you will pay in taxes for each dollar withdrawn from your portfolio. This is why it is so important to have a withdrawing strategy once you retire. You can control when you will pay your taxes on your investment.

Governments give you plenty of various investing account types coming with different tax rules. Make sure you understand them all and know how to optimize them. If you are bored by numbers, investing 1K to 2K in a fee-based financial planner will be worth it. He will write down a withdrawing plan and help you save thousands of dollars in taxes.

Fees you are going to pay

On top of taxes, there is something else you have control of; management fees! If you are still in mutual funds, chances are you can save several thousand dollars simply by replicating your asset allocation with 5 ETFs. This is called the couch potato strategy. You simply move your money away from mutual funds charging 2%+ in MERs (management fees) and you pick ETFs doing exactly the same thing, but for 0.20% (or less!).

If you are like me and you enjoy managing your money more actively, going DIY with an online broker account like Questrade for Canadians will let you save money too! At $5 per trade, you can definitely save lots of money on transaction fees!

Final Thought

You may want to play the market or think you can outsmart other investors, that’s your right. On my side, I make sure I control those six factors first. Each of them is actively contributing to my success through my investing journey.

The post As an Investor, You Control These Six Factors – Nothing Else appeared first on The Dividend Guy Blog.