In September 2017, I received slightly over $100K as a result of the commuted value of my pension plan. I decided to invest 100% of this money into dividend growth stocks. Each month, I publish my results. I don’t do this to brag, I do this to show you it’s possible to build a portfolio during an all-time high market. The market will crash… eventually. In the meantime, I would rather cash some juicy dividends!

Portfolio Comment – Valuation? Really?

Before I go one with my portfolio review, I wanted to come by for another round about valuation. I know I’ll shock some of you with this, but valuation doesn’t matter. When a DSR member asked me a few days ago what to do with stocks like MMM and UPS dropping like rocks and others like Starbucks (SBUX) being at their all-time high, here was my answer:

“I saw UPS and MMM getting hit yesterday but I barely skimmed their results. I’ll have something written on it next week. I think both (and seeing SBUX at their top) would be a great introduction for next Friday’s buy list, don’t you think?

In short (in case you are looking for a rapid answer to act today): the fundamentals of why I bought all three (I have them in my personal portfolio) are still there this morning. The market is getting overhyped or highly depressed for nothing most of the time (Hasbro jumped by 14% earlier this week… was it justified? I don’t think so). Therefore, I keep all of them because they all match my investing thesis.

The reason why MMM is in my portfolio is for the long haul. This business has been around for more than 100 years and will continue to thrive in the next 50 years.

SBUX isn’t done with growth in China, it will continue to thrive for several years through Asia (as they found a way to make them love coffee!)

UPS is a leader in an oligopoly. It has the scale, the network and it is first in class for efficiency. I don’t mind what the market is thinking, I get my increasing dividend each quarter :-)”

I know you will tell me, “but Mike, it doesn’t make sense if you buy a stock that is overvalued.”

I totally agree with you. Where we will disagree is how to determine the fair value of a stock, and more importantly, who determines this? Here’s the most recent example I’ve seen this week about valuation and supposed experts giving their opinion:

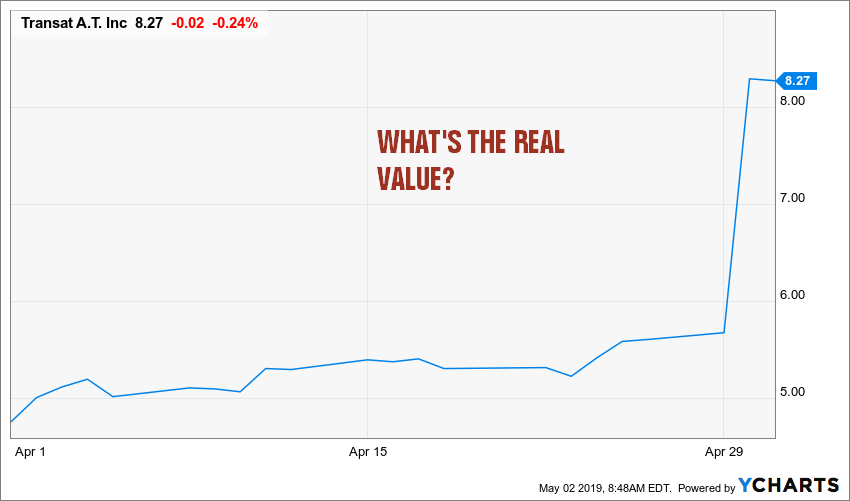

Air Transat and the valuation from $5 to $16

Air Transat (TRZ.TO) is a Canadian company which specializes in the organization, marketing and distribution of holiday travel in the tourism industry. It’s a big buzz right now in Canada because the CEO mentioned that the business could be sold. Shares jumped on the same day:

Source: Ycharts

There was a fascinating article done by La Presse (a French Canadian newspaper) trying to figure out what TRZ’s value was. The first analyst, from Desjardins Wealth Management, mentioned that considering TRZ’s cash alone ($335M) put the stock value at $8.92. Then, to that you must add lands in Mexico ($1.82/share) and the overall business ($1.68/share) and you get a “fair price” at $12. According to the same analyst, if there is an offer on the table, the stock could reach $16.

Regardless of the sale rumors, I was shocked to see that the company’s cash alone was worth more than the actual stock price. In this situation, you might as well just close the business, cash everything out and distribute wealth to shareholders!

Then the journalist asked another analyst. The guy from CIBC (CM.TO) says it’s worth $10 to $11 if it gets sold (so the offer should be around this number).

Finally, the guy from National Bank (NA.TO) concludes the article by saying the stock could go back down to $5 if there is no sale. Strangely enough, my online broker provided me with stock reports coming from the same firm listing the stock at $8.50 (upgraded from $6.00) as of April 30th.

I’ve checked all three analysts and they are all CFAs. Therefore, they are no clowns. Nonetheless, their price ranges from $5 (no sale) to $16 where the assets of the company are worth more than its share price.

Your valuation model is as good as your assumptions

I’m not following Air Transat since it doesn’t pay a dividend. However, I found this example incredibly clear: your valuation model is only as good as your assumptions. Can you really put a price on your assumptions? Would you bet your spouse or children on your assumptions? Depending on which methodology you use, you will find TRZ worth 40% overvalued ($5 vs $8.27) up to being undervalued with a potential gain of 100% (at $16). If three professionals with incredible financial and human power resources can’t get it right (at least 2/3 of them will be wrong, right?), how can we pinpoint the stock price with accuracy?

If valuation doesn’t matter, what does? Your investment thesis.

Surprisingly, it’s a lot easier to establish your investment thesis than it is trying to calculate the fair value of Air Transat, UPS, 3M Co, Starbucks or Hasbro.

Air Transat is obviously a speculative play. Your stock return is completely dependant on a future (or the absence of) acquisition / merger.

The reason MMM is in my portfolio is for the long haul. This business has been around for more than 100 years and will continue to thrive over the next 50 years. It generates billions in cash flow which is used to keep their cutting-edge technology and innovation at an unmatched level. Plus, they acquire whatever can be integrated to their solutions.

SBUX isn’t done with growth in China, it will continue to thrive for several years throughout Asia (as they found a way to make them love coffee!). The company can definitely keep opening 600 stores per year for the next decade in China and will see their revenue, earnings and dividend grow at a very fast pace.

UPS is a leader in an oligopoly. It has the scale, the network and it is first in its class for efficiency. Transportation goods will always require their service and very few competitors can achieve this gigantic task and still be profitable. After all, even DHL left the U.S. market because it couldn’t compete with UPS and FedEx (FDX). I don’t care what the market is thinking; I get my increasing dividend each quarter :-).

In other words, take more time to analyze the company and write down your investment thesis. This will be a lot more useful than playing with your calculator and using various valuation models. Let’s set this newsletter aside and let’s come back to it next year to see what happened with TRZ, shall we?

Now, let’s take a look at how my “overvalued” stocks have performed ?

Numbers are as at May 2nd 2019 before the bell:

Canadian portfolio (CAD)

| Company Name | Ticker | Market Value |

| Alimentation Couche-Tard | ATD.B.TO | $6,780.24

|

| Andrew Peller | ADW.A.TO | $5,415.75 |

| National Bank | NA.TO | $5,107.20 |

| Royal Bank | RY.TO | $6,387.00 |

| CAE | CAE.TO | $6,246.00 |

| Enbridge | ENB.TO | $7,975.94 |

| Fortis | FTS.TO | $4,879.71 |

| Intertape Polymer | ITP.TO | $5,619.00 |

| Lassonde Industries | LAS.A.TO | $3,607.80 |

| Magna International | MG.TO | $5,159.70 |

| Cash | $982.54 | |

| Total | $57,178.34 |

My account shows a variation of +$533.96 (+0.94%) since the last income report.

The earnings season hasn’t start yet for my Canadian holdings as most of them are “dormant” and waiting for the next quarter to be published. I am contemplating my cash account growing and I start to think of two things:

#1 I should definitely take 5 minutes and call my online broker to start dripping most of my stocks

#2 I should definitely use the extra $1,000 sleeping to increase one of my positions

The best opportunity in my portfolio seems to be Lassonde. I’ll give it some more thought, but I’ll have to move this money ASAP. Right now, this $1,000 is sleeping while I’m working… it should be the other way around!

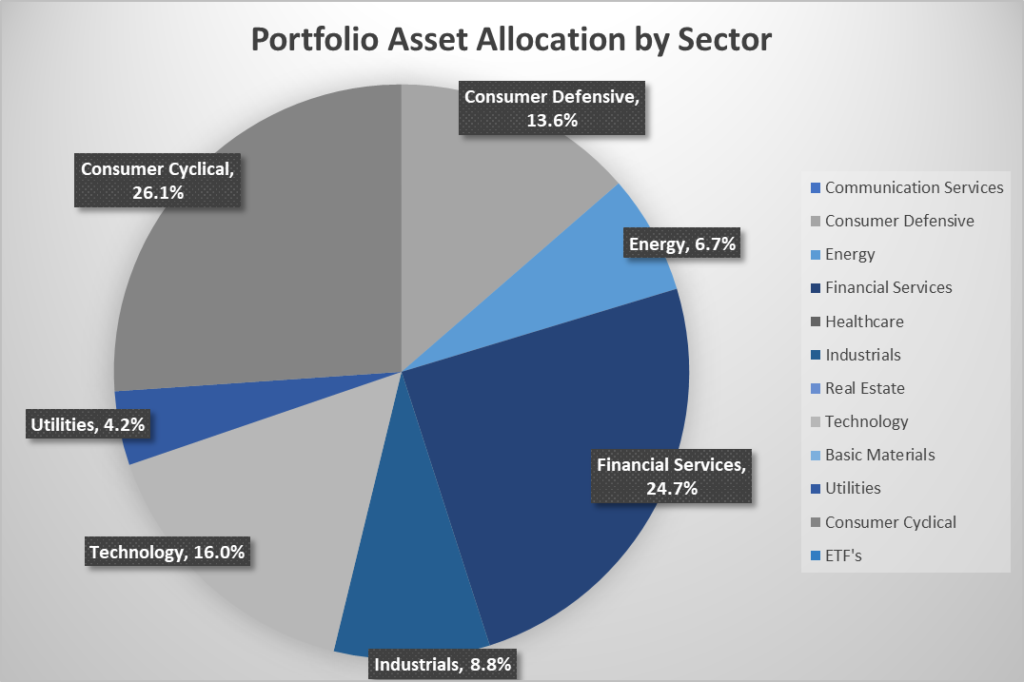

You can read about how I managed my portfolio as a Canadian (e.g. mixing both CDN and US investments): Investing the Canadian Way – Tricks I use to Boost My Returns. I discuss my sector allocation, how I manage currency fluctuations and my favorite sectors.

Numbers are as at May 2nd 2019 before the bell:

U.S. portfolio (USD)

| Company Name | Ticker | Market Value |

| Apple | AAPL | $6,526.12 |

| BlackRock | BLK | $6,707.82 |

| Disney | DIS | $6,137.10 |

| Garrett Motion | GTX | $54.00 |

| Gentex | GNTX | $5,376.80 |

| Hasbro | HAS | $4,696.14 |

| Lazard | LAZ | $3,937.20 |

| Microsoft | MSFT | $7,672.79 |

| Resideo Tech | REZI | $114.60 |

| Starbucks | SBUX | $6,589.20 |

| Texas Instruments | TXN | $5,814.50 |

| United Parcel Services | UPS | $3,870.94 |

| Visa | V | $8,139.50 |

| Cash | $413.59 | |

| Total | $66,050.30 |

The US total value account shows a variation of +$4,726.40 USD (+7.7%) since the last income report.

This was a marvelous month for me as most of my holdings posted strong results (besides UPS! Ha ha!)

Hasbro surprised the market and posted a profit while most analysts were expecting a loss due to weak sales and Toys’R’Us bankruptcy claw back. Franchise brands revenue was up 9% during the quarter and Hasbro gaming revenue rose 2%, led by Duel Masters, Connect 4 and Twister. The gross margin was 64.5% of sales vs. 63.8% consensus. During Q1, Transformers toys tied in to the BumbleBee movie appear to have stoked the strong revenue growth in a positive sign for the overall toy industry overall due to the strong movie slate coming up (Avengers, Star Wars, etc.). It looks like HAS will get past the Toys’R’Us saga faster than expected!

BLK navigated through a difficult quarter. While the company beat both EPS and revenue expectations, it did it with negative numbers. The 5% decrease in base fees Y/Y mostly reflects the impact of negative markets in Q4 and continued dollar appreciation. Investment advisory, administration fees, and securities lending revenue fell 4.8% to $2.81B from $2.95B a year ago. Technology services revenue in the quarter rose 11% to $204M on continued momentum in Aladdin. Management increased their dividend by 5% and as long as BLK trades under $500, it looks like a great deal for long-term investors.

Disney hasn’t published their earnings yet, but they add more meat to their streaming service, Disney +. While the market seems both surprised and happy with the new information, shares surged 20% in the last 30 days. This is clearly another market overreaction, but I’ll take it!

Apple also did relatively well (enough to push the stock almost 10% higher in the past 30 days). Although iPhone revenue lagged (as expected), the services business was up by 16%. The board announced a $75B share repurchase program along with another 5% dividend increase.

My entire portfolio quarterly update!

Each quarter, we run an exclusive report for Dividend Stocks Rock (DSR) members called DSR PRO. The PRO report includes a summary of each company’s earnings report for the period. We have been doing this for an entire year now and I wanted to share my own DSR PRO report for this portfolio. You can download the full PDF that gives all the information about all my holdings.

Download my portfolio Q1 2019 report

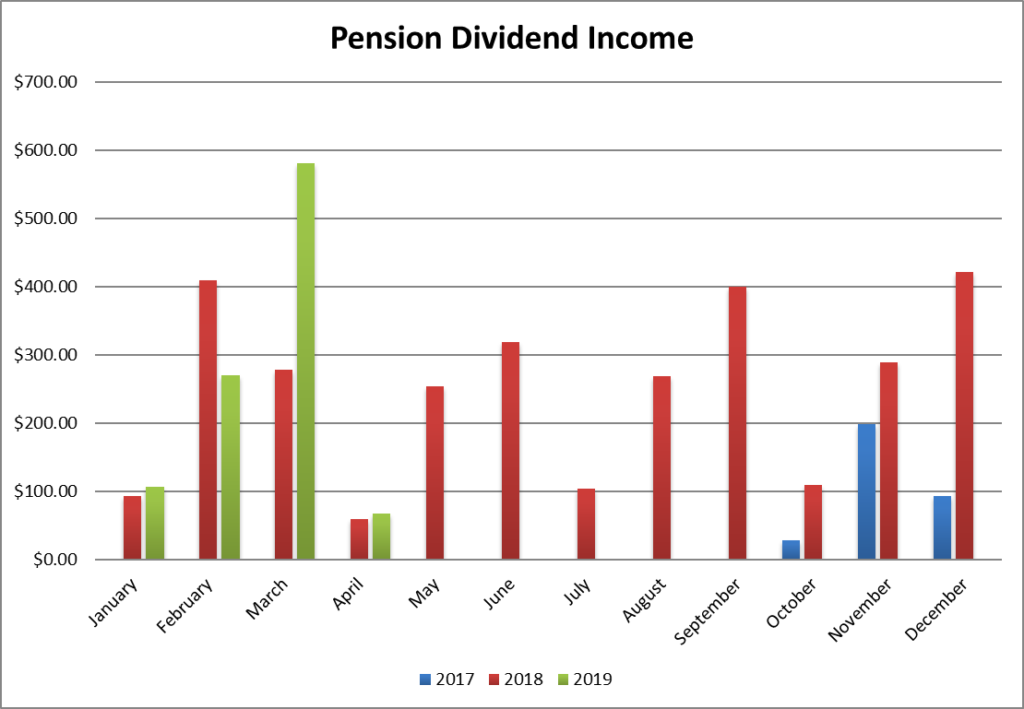

Dividend income: $68.32 CAD (+14%)

April is my smallest dividend income month of the year. This is mostly because I have very few stocks paying me during those 30 days and they are low yielding stocks. However, look at the dividend growth here! The growth is compared to April 2018 (not a necessarily a recent dividend increase):

- Alimentation Couche-Tard: +39%

- Andrew Peller: +14%

- Gentex: +4.5%

- Currency: 4% gain on GNTX dividend

When you combine both dividend growth and capital growth in this portfolio, you get great results! I’ve never looked for only high yielding stocks. I think the balance between dividend growth and capital growth is important in one’s portfolio.

Canadian Holdings payouts: $32.04 CAD

- Alimentation Couche-Tard: $10.75

- Andrew Peller: $21.29

U.S. Holding payouts: $27.03 USD

- Gentex: $27.03

Total payouts: $68.32 CAD

*I used a USD/CAD conversion rate of 1.3421

This is not only my largest dividend month, but also my largest quarter so far. It is quite exciting to see dividends increasing at such rapid pace.

Since I started this portfolio in September 2017, I have received a total of $4,352.17 CAD in dividends. Keep in mind that this is a “pure dividend growth portfolio” as no capital can be added into this account (it’s a LIRA). Therefore, all dividend growth comes from stocks and not from additional capital.

Final thoughts

My portfolio has had a great ride so far in 2019. This recovery is so strong that I could now take a 25% hit on my portfolio and I would still have a few hundred over my original amount. This shows you how it’s impossible to know when and by how much the market will crash.

If you are worried it will happen, I suggest you read “Sell Now – It’s About Time Someone Tell You This”. This article will tell you what you should toss in your portfolio and what you should keep.

The post April Dividend Income Report – Beating Records, Holding Steady appeared first on The Dividend Guy Blog.