Apple just released its fourth quarter with stronger results than expected:

-

$42.1 billion in revenue vs $37.5 in Q4 2013

-

$1.42 Earnings per share vs $1.18 in Q4 2013

-

16% sales jump for iPhones

-

20% EPS growth in 2014

-

$13.3 billion in cash flow

-

Declared dividend of $0.47/share

We will go through the main highlights of their reports, but first, we will analyze what Apple has been doing with its cash over the past few years. If you look at the following graph, you will notice how fast its growth was in 2011 but how revenues are now slowing and 2013’s earnings were less than those of 2012.

At the beginning of 2013, the stock started to disappoint the market as many investors were worried about how Apple would deliver its next big thing and the fact that competitors like Samsung were grabbing market share on Apple’s most profitable segment; the mobile industry.

But the company bounced back since the beginning of 2014 with surprising growth in terms of sales and earnings. It recently announced the new iPhone 6 and Apple Watch to be launched in early 2015. The stock has been trading around $97-$100 for a while – is Apple set to boom again? Following the first 4 Dividend Stocks Rock Investing Principles, I’ll take a look at Apple and present a full dividend analysis.

Principle #1 High Dividend Yield Doesn’t Equal High Returns

Did you know that the highest dividend yielding stocks underperform more “reasonable” yielding stocks? The Hartford Mutual Funds company wrote:

The study found that stocks offering the highest level of dividend payouts have not performed as well as those that pay high, but not the very highest, levels of dividends.”

Read more about this research here.

Apple’s dividend history is still in its infancy since management started this strategy to seduce investors in 2012. Was this related to the fact that 2013 produced slower growth and management wanted to keep more people on board? Or was pressure from activist shareholders like Icahn enough to convince Apple to distribute a few pennies from its treasure chest?

Apple’s dividend yield hasnnever been higher than 2.63% (and this was for a very short period). The yield is most likely to hover around 2% and this is why this stock will fly under the radar of many dividend investors. Keep reading and you will see why AAPL should be part of all dividend portfolios.

Principle #2: If There is One Metric; It’s Called Dividend Growth

If I had to go blindfolded to pick a stock and have only one metric to look at, I would pick dividend growth. This is the most important metric to me as it is a clear sign of the company’s financial health and ability to pay me for years to come. Here’s an interesting quote from Saturna Capital:

“Indeed, dividend growth has been a much larger determinant of equity returns in this new era of low benchmark rates and higher levels of uncertainty.”

You can get the full detail here.

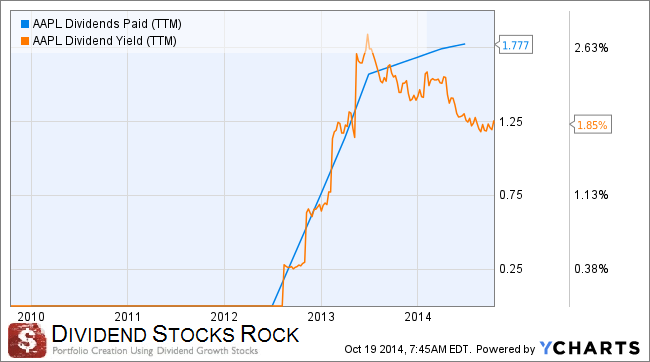

Did you know that Apple used to pay a dividend back in the 80s? in fact, from 1987 to 1995, Apple paid a quarterly dividend that went from $0.06/share to $0.12/share. The dividend recently came back from the dead in 2012 starting at $2.65/share and has risen to $3.05 in 2013 and $3.29 in 2014 (now $0.47/share after the 7-for-1 stock split). Considering the immense amount of liquidity this company has (XXXX in cash for its latest quarter), we can see this stock increasing its payout over the upcoming years.

Principle #3: A Dividend Payment Today is Good, A Dividend Guaranteed For the Next 10 Years is Better

What really makes me enthusiastic as a dividend investor is Apple’s ability not to simply maintain its dividend but to increase it systematically. You can easily analyse a company’s ability to sustain a dividend growth policy by looking at its dividend payout ratio combined with their dividends paid.

This means the company has adopted a sustainable model for raising its dividend and won’t jeopardize the company’s future since there is more than enough money to pay investors. Apple has tons of cash and a very low payout ratio. This looks good for the future.

Principle #4: The Foundation of Dividend Growth Stocks Lies in its Business Model

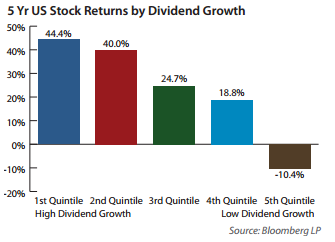

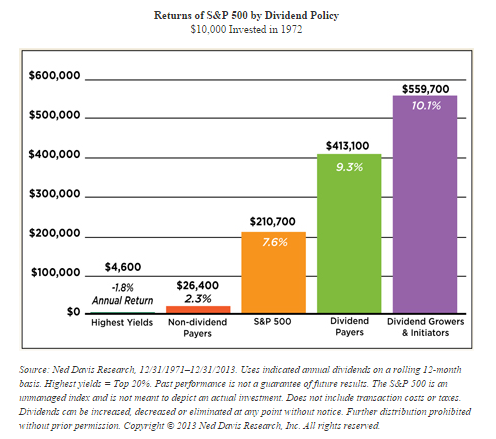

A company that doesn’t have a sound business model won’t be able to sustain consecutive dividend increases over the long haul. On the other hand, businesses which pay dividends and increase them will outperform other stocks:

Source: Edward D. Jones – Dividend Stocks Rock

Now how can you find these marvels? This is why you need other financial metrics to identify companies that will be able to sustain and increase their dividends for the next 10 years. At DSR, we look at the 3 and 5 year metrics for Sales and Earnings per Share (EPS) growth. We only select companies with positive growth over both the 3 and 5 year periods. Since an economic cycle lasts between 5 and 8 years, a strong company should be able to post increasing sales and earnings over these time frames. I’m using both EPS and Revenue TTM (total return, not annualized) from Ycharts:

DSR STOCK METRICS

3 year revenues = 39.35% Pass

5 year revenues = 281.4% Pass

3 year EPS growth = 23.45% Pass

5 year EPS growth = 323.30% Pass

Apple passes the four tests easily. The beauty of Apple’s business model is its ecosystem. They don’t launch products just for the sake of it. They study and research long enough to launch an innovation that is backed with a solid plan and a perfect fit with the current product ecosystem. This is how the Mac, the iPhone, iPod and iPad and soon the Apple Watch can “talk” together.

A Look at the Most Recent Results

Apple’s last quarter is not only very strong but leads to an optimistic forecast for the Holiday season and the rest of 2015. The company projected stronger than expected revenue of $63.5 – $66.5 billion for the next quarter. Tim Cook had great reasons to smile:

“Our fiscal 2014 was one for the record books, including the biggest iPhone launch ever with iPhone 6 and iPhone 6 Plus,” said Tim Cook, Apple’s CEO. “With amazing innovations in our new iPhones, iPads and Macs, as well as iOS 8 and OS X Yosemite, we are heading into the holidays with Apple’s strongest product lineup ever. We are also incredibly excited about Apple Watch and other great products and services in the pipeline for 2015.”

Source: Apple

Digging down the financials, we notice iPhone sales are strong (with iPhone 6 being the biggest launch ever in the iPhone series) but iPad sales struggles down by 13%. This is about the only bad news for this result as even the Mac has well performed with sales up by 21%. We compare Samsung a lot with Apple since both companies drive most of their revenues from smartphones. While Apple keeps piling cash, Samsung expects its benefits to drop by 60% du to high margin pressure on its smartphones.

Considering Apple Pay and Apple Watch as new innovation to have an impact on 2015 results, Apple is in the right direction to go through a strong 2015.

Disclaimer: I hold APPL shares at the moment of writing this article and it is part of our Dividend Stock Rocks Portfolios.