Retirement, Early Retirement, Financial Independence and Early Retirement (FIRE) are very popular topics among personal finance bloggers. I could even say that the concept of FIRE is particularly popular among dividend bloggers. Guys like Joe @ Retire by 40 and Jason at Mr. Free at 33 made it. Some others like Mark @ My Own Advisor & Bob @ Tawcan and Bert & Lanny @ Dividend Diplomats took a different path, but they are all savvy savers. They are budget aces. I’m not like that… definitely not. But that doesn’t mean I’m not interested in FIRE.

Not too long ago, I mentioned my retirement D and C plans on Seeking Alpha. In that article, I explain that I will reach the psychological mark of $1M at 65 (D plan)… or 50 (C plan). A lot of investors write that it is not enough. That aiming for $1M at retirement is like aiming at poverty level (I barely exaggerate). Are they right? Am I foolish? As it is often the case in finance, the right answer is “it depends…”. I’ll try to explain what I mean by telling you about my 4 retirement plans… Let’s start with the “boring plans” today, and I’ll follow-up next week with the 2 “interesting plans”.

The Boring D&C Plans; Having $1M between 59 & 65

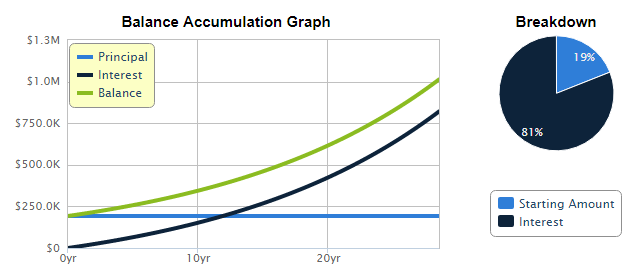

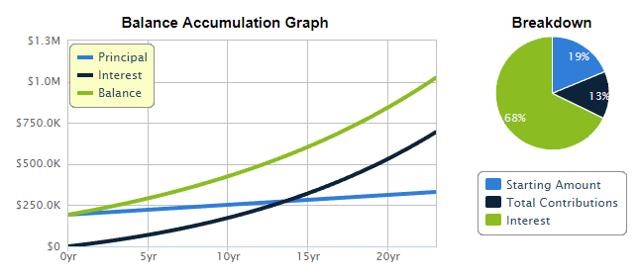

My “bad” retirement plans include having $1M between the age of 59 and 65. What’s the difference between both plans? Simply, that if I don’t save a penny in the next 29 years, I’ll have to wait until 65 to get my million dollars. If I save $500/month starting now, I can cut 6 years to my retirement. I’ve used a 6% investment return in both cases. Considering I’m 100% invested in equity and that I invest for 23 to 29 years, this makes plenty of sense. Statistically speaking, it totally makes sense. Even if you take the last 20 years of the S&P 500 total return, you get an annualized return of 6.48%. This includes the techno bubble and the world’s most important stock crash of 2008.

You can see my calculations results here:

Graph Source

Graph Source

Inflation is your enemy

Honestly, I was quite surprised to see how many people were saying that 1M$ was not enough to retire in 25-30 years from now. The main point was to consider inflation. I know it very well because I’m a former financial planner. Inflation is probably the most overlooked factor when calculating your retirement plan. First, we tend to forget this concept as the inflation over the past 10 years was almost nothing. But there is a problem with the stats we pull-out; its composition.

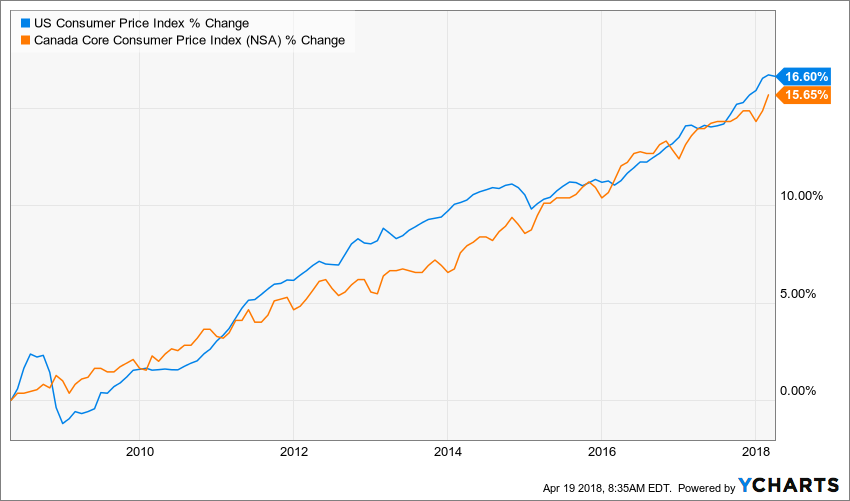

When you look at the Consumer Price Index (CPI) to know if inflation went up or not, you are looking at the wrong direction as a consumer. This indicator is good for a country or a central bank, but not so much for a citizen.

Both countries show inflation rate of roughly 1.5% annually; source Ycharts

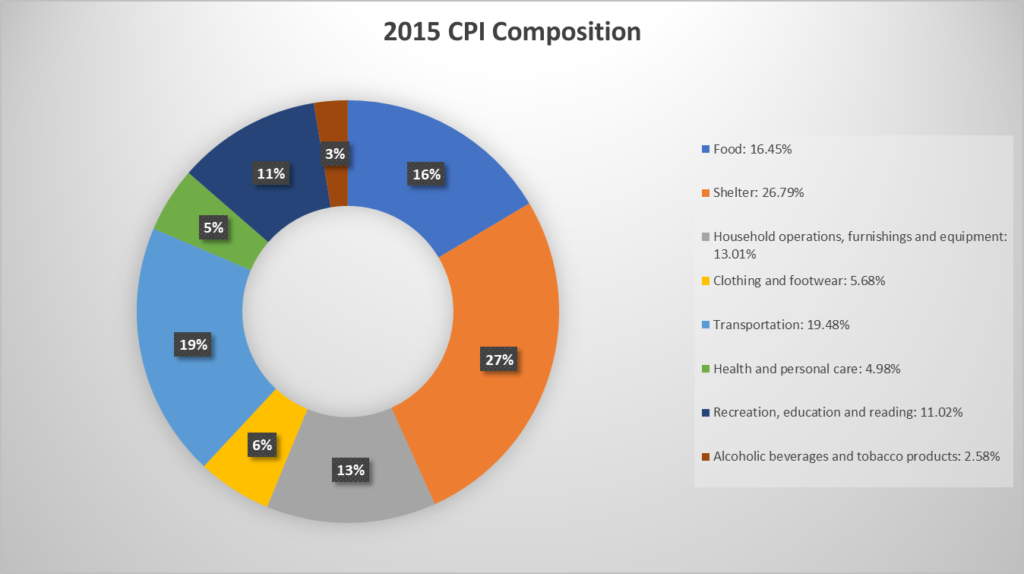

If you have some time, I’d suggest you read the CPI definition of your country to understand. Mine (Canada), can be found here. Here’s how the basket of good was composed in 2015:

- Food: 16.45%

- Shelter: 26.79%

- Household operations, furnishings and equipment: 13.01%

- Clothing and footwear: 5.68%

- Transportation: 19.48%

- Health and personal care: 4.98%

- Recreation, education and reading: 11.02%

- Alcoholic beverages and tobacco products: 2.58%

I know very well that food (family of 5 with 2 teenagers doing lots of sports!) is taking a lot more than 16% of my budget, and transportation is a lot smaller as we only have 1 car. But if car prices have been low (my monthly car payment is roughly the same for the past 12 years with 3 different cars), then the country will say inflation is low. If food price has increased significantly during that time, then “my inflation” is a lot larger than my country’s. For that reason, I calculate an inflation of 2% for my retirement.

How can you retire with so “little money”?

Once you factor inflation in my “million dollars”, I get a present value of $563K (retiring at 65) to 634K (retiring at 59). The present value refers to how much your future value is worth today, or how much it will be worth at retirement, in today’s dollar (factoring the inflation).

Therefore, it’s like pressing fast forward and waking up tomorrow at 59 with $634K in my bank account. Do I have enough to retire? Imagine I keep the same numbers: inflation rate of 2% and investment return rate of 6%. That makes a net investment return of 4%. If I apply the “4% withdrawing rules”, I could indefinitely (or almost) withdraw 25K from my portfolio. Then, I’ve calculated how much I can afford to withdraw each year and burn my nest egg to the ground by the time I pass away (let’s say 30 years). I found that I could live on $35K (indexed with an inflation at 2%):

| Year | Starting amount | Withdrawal | End Amount |

| 1 | $ 634,000.00 | -$ 35,000.00 | $ 634,940.00 |

| 2 | $ 634,940.00 | -$ 35,700.00 | $ 635,194.40 |

| 3 | $ 635,194.40 | -$ 36,414.00 | $ 634,707.22 |

| 4 | $ 634,707.22 | -$ 37,142.28 | $ 633,418.84 |

| 5 | $ 633,418.84 | -$ 37,885.13 | $ 631,265.74 |

| 6 | $ 631,265.74 | -$ 38,642.83 | $ 628,180.28 |

| 7 | $ 628,180.28 | -$ 39,415.68 | $ 624,090.48 |

| 8 | $ 624,090.48 | -$ 40,204.00 | $ 618,919.67 |

| 9 | $ 618,919.67 | -$ 41,008.08 | $ 612,586.28 |

| 10 | $ 612,586.28 | -$ 41,828.24 | $ 605,003.53 |

| 11 | $ 605,003.53 | -$ 42,664.80 | $ 596,079.04 |

| 12 | $ 596,079.04 | -$ 43,518.10 | $ 585,714.60 |

| 13 | $ 585,714.60 | -$ 44,388.46 | $ 573,805.71 |

| 14 | $ 573,805.71 | -$ 45,276.23 | $ 560,241.24 |

| 15 | $ 560,241.24 | -$ 46,181.76 | $ 544,903.05 |

| 16 | $ 544,903.05 | -$ 47,105.39 | $ 527,665.52 |

| 17 | $ 527,665.52 | -$ 48,047.50 | $ 508,395.10 |

| 18 | $ 508,395.10 | -$ 49,008.45 | $ 486,949.85 |

| 19 | $ 486,949.85 | -$ 49,988.62 | $ 463,178.91 |

| 20 | $ 463,178.91 | -$ 50,988.39 | $ 436,921.95 |

| 21 | $ 436,921.95 | -$ 52,008.16 | $ 408,008.62 |

| 22 | $ 408,008.62 | -$ 53,048.32 | $ 376,257.91 |

| 23 | $ 376,257.91 | -$ 54,109.29 | $ 341,477.54 |

| 24 | $ 341,477.54 | -$ 55,191.47 | $ 303,463.23 |

| 25 | $ 303,463.23 | -$ 56,295.30 | $ 261,998.00 |

| 26 | $ 261,998.00 | -$ 57,421.21 | $ 216,851.40 |

| 27 | $ 216,851.40 | -$ 58,569.63 | $ 167,778.67 |

| 28 | $ 167,778.67 | -$ 59,741.03 | $ 114,519.91 |

| 29 | $ 114,519.91 | -$ 60,935.85 | $ 56,799.10 |

| 30 | $ 56,799.10 | -$ 62,154.56 | -$ 5,676.79 |

Considering that my wife and I will also get Canadian’s Old Age Security pension, I can count on an additional $1,000 per month at the age of 70 (let’s figure they push it back to that age in the meantime). This pension would cover any shortfall my portfolio could have (just in case my 6% investment return over the next 50 years isn’t accurate). In other words; I count the OAS as a safety net, not to be part of my budget.

Now, can we live with $3,000 per month? Absolutely!

Considering my house will be paid in full at retirement, I will have more than enough with 3K per month. At the moment, my family budget is about 6K per month, and this includes feeding 3 children (2 teenagers), paying for their tuitions (private school for the oldest one), activities and my mortgage payment. Once my children leave the house, I’ll be rich! Hahaha!

Jokes aside, my monthly budget will fall under $2K per month. Therefore, I will even be able to afford a nice trip to Europe each year! On top of that, I will still be sitting on a 500K+ safety net as my house will be paid in full and is already worth near $400K today.

So…. Is $1 million is enough?

My short answer is yes… and you just read my long answer, hahaha!

But that’s the boring plan. That’s the “if everything goes wrong” plan. Honestly, I already consider myself retired. I’ll explain to you why next week!

The post A Million Dollar at 59 Isn’t Enough appeared first on The Dividend Guy Blog.