The stock market is definitely not a place for the faint of heart. At one point in time this February, the S&P 500 dropped by more than 10% (-10.51% on February 11th, 2016). On the Canadian market, the TSX dropped by more than 15% since its highest point in 2015. Now that we have been hearing more discussion about oil production stabilization from major oil countries, it seems both markets are on their way to recovering a good part of their drops. This is also a great opportunity to chase down bargains and make a few purchases. While the best timing might already be behind us, there are still good opportunities in this crazy market.

Recently, I reviewed 6 companies that raised their dividend within the first 2 months of the year. A reader of mine highlighted that only one company was Canadian (CNR.TO or CNI on the US market). This is why I decided to discuss a few great buy opportunities on the Canadian market in this article.

Royal Bank (RY.TO)

source: Ycharts

At the moment, Royal Bank is my favorite Canadian Banks. I even bought 29 shares to complete my children’s tuition fund in February. The reason why I bought RY.TO (RY for the US ticker) instead of buying another Canadian bank is linked to how RBC generates its revenues.

The company is a leader in capital markets and wealth management. Two sub-sectors poised for strong growth in the upcoming years. As Canada’s population is aging, fortunes are passing from the older generation and this new generation will face many challenges. This is why wealth management will become a priority for many families. The capital market sub-sector is more volatile than classic savings and loans activities. However, it is also a great source of growth for many banks. RBC has developed quite an expertise in this field.

At the same time, I tend to favor a bank that is less linked to classic savings and loans at the moment. Economic growth perspectives are inexistent for Canada in the upcoming two years mainly because of the oil industry. This will be a long period when consumers won’t borrow more than what they show on their balance sheet at the moment.

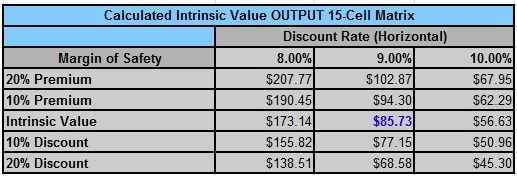

In order to be very sure of my purchase, I also use a double stage dividend discount model. After all, what really matters for me is the value of a company considering how much it will pay me back in dividends in the future. I didn’t go crazy with the dividend increase rate with a 6% growth rate for the first 10 years and I dropped it to 5% afterward. Here’s what my calculations look like:

| Input Descriptions for 15-Cell Matrix | INPUTS |

| Enter Recent Annual Dividend Payment: | $3.16 |

| Enter Expected Dividend Growth Rate Years 1-10: | 6.00% |

| Enter Expected Terminal Dividend Growth Rate: | 5.00% |

| Enter Discount Rate: | 9.00% |

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 8.00% | 9.00% | 10.00% |

| 20% Premium | $144.36 | $107.93 | $86.09 |

| 10% Premium | $132.33 | $98.93 | $78.91 |

| Intrinsic Value | $120.30 | $89.94 | $71.74 |

| 10% Discount | $108.27 | $80.95 | $64.57 |

| 20% Discount | $96.24 | $71.95 | $57.39 |

Source: Dividend Monk Calculation Spreadsheet

Finally, if I was looking at a smaller bank, I would probably go for Canadian Western Bank (CWB.TO). This bank is mainly based in Alberta and has benefitted from the oil boom. The bank has since then suffered from the oil bust and this may be the right time to enter in a position in a riskier play.

If you are interested in other banks, I’ve already covered the other members of the Big 5 at Seeking Alpha.

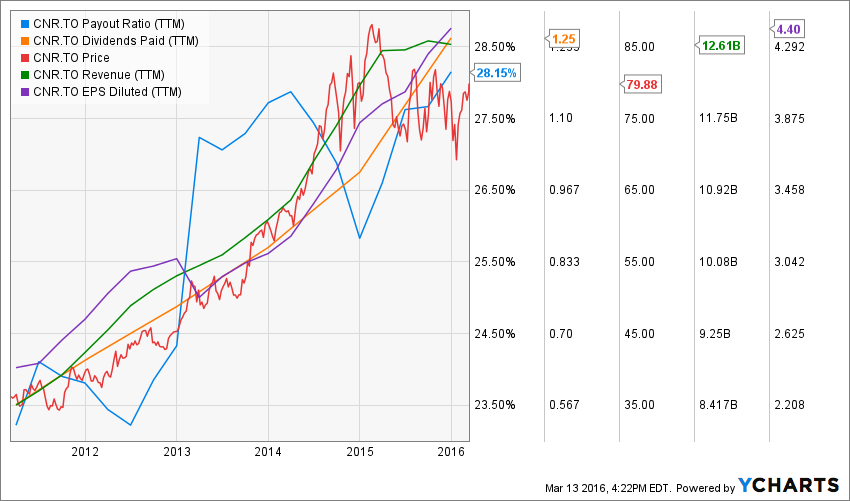

Canadian National Railway (CNR.TO)

source: Ycharts

It is no secret to anybody following this blog or being a member of Dividend Stocks Rock; I think Canadian National Railway (CNR.TO) offers a very good buying opportunity. I even purchased some shares myself towards the end of 2015.

If there is only one reason to buy CNR.TO (CNI if you look for the US ticker), it is probably the fact that there are no other railway operators in North America with such low operating margins. We all know how costly it is to build, manage and maintain railways each year while truckers don’t have to pay a penny to construct highways. This is where Canadian National Railway has become the top of the line railway operator with an operating margin of 54% last quarter. In comparison CP.TO is at 59.8%, CXV at 71.6% and UNP at 63.2%.

But if you need more reasons, here are plenty:

- 5 year revenue growth of 11.22% CAGR 5 year EPS growth of 14.64% CAGR 5 years dividend growth of 15.40% CAGR

Very low payout ratio of 27.39%

Since CNR evolves in a fairly stable and predictable market, I will use a discount rate of 9%. As for dividend growth, I use a 10% rate for the first 10 years and reduce it to 7% to be more conservative. The 10% dividend growth for the first 10 years seems aggressive at first, but considering the company increased it by 15% CAGR over the past 5 years, I think that using 10% for the first 10 years is a fair assessment:

Source: Dividend Monk Calculation Spreadsheet

Source: Dividend Monk Calculation Spreadsheet

Agrium (AGU.TO)

source: Ycharts

Agrium is another of my recent buys for my retirement portfolio. This stock is also part of my Canadian Growth Dividend Portfolio beating my benchmark by over 10% since its creation (you can see my performance here).

AGU.TO (AGU for US investors) is another stock taking a serious beating being -15% over the past 12 months or so. The price of potash dropping, global economic slowdown and less demand coming from emerging markets contributed to making AGU a great buy opportunity at the moment.

The company isn’t without risk as I just highlighted them. However, its retail business (it also sells many products to farmers on top of fertilizer) enables the company to support rougher period. Compared to Potash (POT.TO or POT) which recently cut its dividend by 34% early in 2016, AGU increased its payout from $0.99 to $1.21 within 2015 through a dividend increase each quarter of the year. Now we are talking about a confident management team! The best of all is that AGU’s payout ratio remains in control around 50%.

With the Chinese Government announcing various plans to boost up its economy, we can expect a potash price rising in the upcoming years and AGU will head to the top again.

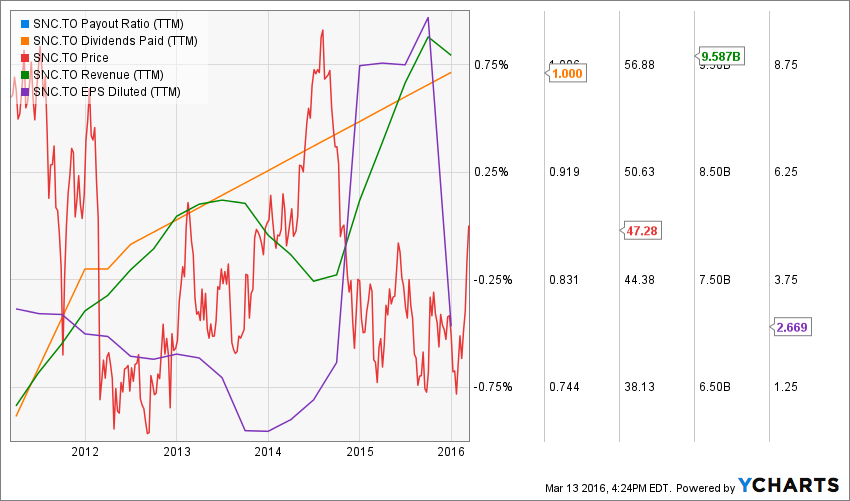

SNC Lavallin (SNC.TO)

source: Ycharts

Do you remember me selling my shares of Scotia Bank (BNS.TO) to buy SNC Lavallin last year? Let’s go back in time and read this article again. I was somewhat challenged by readers (and that’s what I like to be honest) but I was rather called out for profanity on Seeking Alpha (they picked up my article and republished it on their site). I like making bold moves when they make sense. SNC.TO isn’t a big part of my portfolio, but I found (and still find!) more value into SNC right now than BNS. It’s been almost a year and I have proven to be right so far:

SNC is up 19.96% since I wrote my article and BNS is down 6.26%. This excludes dividend payments, but still, it would come down to the same result; SNC is seriously doing better than BNS.

The company published better than expected results in their most recent quarters leading analysts to increase their target for the engineering firm. This is the main reason why the stock is up so high recently. Not to mention the future looks brighter than before: At the end of 2015 SNC had a $12 billion backlog, and in the first 60 days of 2016 added $1.3 billion contract at the Darlington Nuclear Generating Station and an $800 million contract in the Middle East for its oil and gas division.

Gluskin & Scheff (GS.TO)

source: Ycharts

Gluskin & Scheff has taken a serious beating over the past 12 months. The stock is currently down by over 25% since January 2015. At least, the company paid $1.59 per share in dividends in 2015. This translates to a 7.81% yield based on the current stock price. You know that I’m far from being a fan of high dividend yield. However, Gluskin & Scheff high dividend yield is linked to its semi-annual special dividend based on performance fees. While it makes the dividend yield fluctuate, it doesn’t impact its payout ratio that much as the special dividend is paid according to how good management was.

While some analysts were expecting a special dividend as high as $0.56 per share, they were disappointed to see a special dividend at $0.10. This is on top of its quarterly dividend of $0.25. In 2015, the company paid a total of $1.575 per share for a yield of 8.70% based on a stock price of $18.11. The first dividend of 2016 is then $0.35 compared to $0.83 a year ago. Assets under management (AUM) are not doing so well with a reduction of 1% for $75 million of net outflows. However, the company shows a higher AUM in December 2015 ($8.307B) compared to December 2014 ($8.220B). As I previously mentioned, the stock price has taken a beating for the past 12 months and I think it is unjustified. The “hole” in their revenue ($69M vs $58M this year) is due to a drop of $10M in performance fees. It is hard to expect the company to outperform in such volatile markets when the Canadian market suffered in 2015. On the other hand, this makes GS a great contender for an acquisition by a larger wealth management firm…

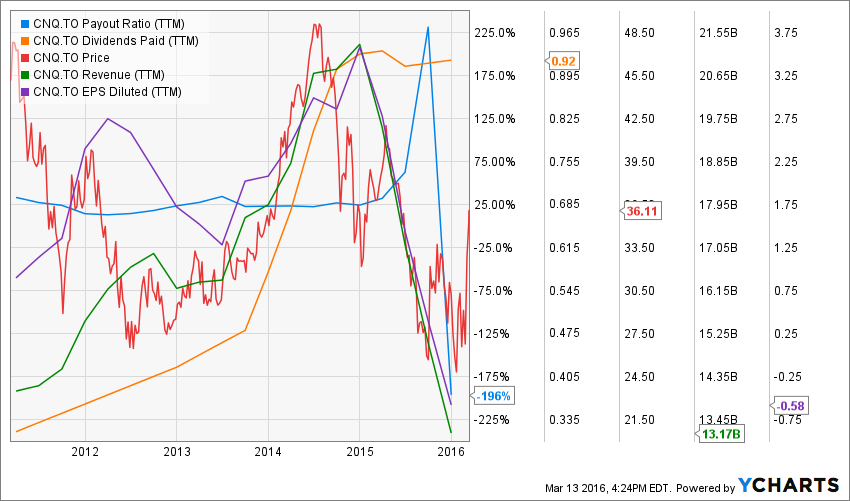

Canadian National Resources (CNQ.TO)

source: Ycharts

CNQ is one of Canada’s largest oil & gas exploration and production companies. The company shows a strong history of adapting to this ever changing environment and allocating capital accordingly. In order to support its cash flow, the company recently sold its third-party royalty assets to PrairieSky Royalty (PSK.TO) for $1.8 billion dollars. The Horizon oil sands project is expected to generate substantial and continuous cash flow for the company, securing at the same time its dividend payment even considering a very high payout ratio. As you can see, we are currently focusing on cash flow generation to support dividend payments rather than use a more classic metric in the payout ratio. Over the long run, this analysis is not sustainable (a company must make a profit at one point if it wants to keep increasing its dividend). However, while facing many headwinds, what remains the most important thing to analyze is a company’s ability to generate cash flow. This is the heart and blood of the company. CNQ is in a very good position to generate cash flow at the moment.

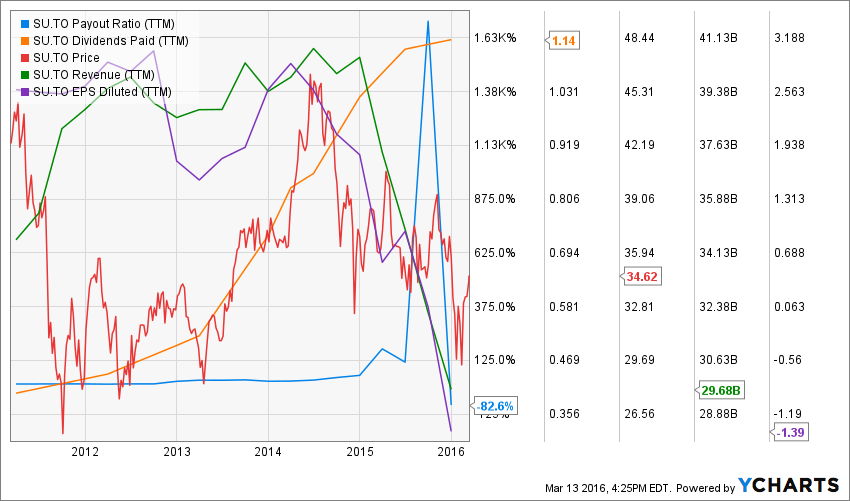

Suncor Energy (SU.TO)

source: Ycharts

Suncor Energy is Canada’s leading integrated oil and gas producer, generating superior refining margins and strong price realizations, which help offset higher-than-average operating costs at some of its upstream operations. Similar to COS, Suncor is sitting on a huge oil sand resource. It has the ability to produce barrels of oil for decades. This asset leads to low-cost plateau production. Such activity will continue to generate a consistent cash flow, securing future dividend payments despite a current payout ratio that is out of the norm. Suncor has become an integrated oil company with an enviable portfolio of oil sands assets. This is why its stock price hasn’t been affected too much over the past 2 years compared to its peers (only -10%). The company keeps pushing towards the top as they recently tried to acquire COS.TO with a hostile bid. Both companies finally agreed toward the end of January to a $4.2 billion deal.

I’m sure there is more! Now it’s your turn!

All right, I think I’ve shared enough for today. What do you think of my picks? Which other stocks do you have on your radar?

disclaimer: I hold shares of RY, CNR, AGU, GS, SCN in my Dividend Stocks Rock portfolios.

The opinions and the strategies of the author are not intended to ever be a recommendation to buy or sell a security. The strategy the author uses has worked for him and it is for you to decide if it could benefit your financial future. Please remember to do your own research and know your risk tolerance.