When investing for your retirement, be sure of one thing; the investment should allow you to sleep well at night. When you build a retirement portfolio, the very first thing you want is to buy solid companies that will be there for the next 50 years. A classic quote from Warren Buffett was that he always pick shares of a company that he would feel good about even if the stock market had to close for 10 years. In other words; the world’s most successful investor doesn’t pick up the flavor of the day, he’s looking for companies that will outlive generations. This is the kind of company you want to buy when building your retirement fund. These companies are not easy to find, but you can usually find most of them among strong dividend payers.

By definition, a strong dividend payer is a company that has been able to increase both its revenues and earnings over time. Through a constant and increasing cash flow, management decides to reward shareholders with dividend payments. These distributions increase year after year backed by a strong business model. The increasing distributions are the foundation of any dividend growth investor portfolio.

As I know that many Canadians are afraid to invest in the US market for their RRSP due to the currency factor, I’ve picked 4 Canadian dividend growth stocks that I believe will continue to increase their payments for a while. But first, here’s a quick reminder of how an RRSP works:

RRSP Quick Facts

Maximum contribution for 2016: $26,010

Maximum contribution for 2015: $25,370

Date limit for the contribution (to be used against 2015 income): March 1st 2016 (after this date, your contribution will count against your 2016 income)

How much can you contribute to your RRSP? It is 18% of your earned revenue (doesn’t apply on interest, dividend or capital gains). The best way to find your RRSP contribution limit is to look for this information on your Notice of Assessment (NOA). This is the document you receive from the Canada Revenue Agency after completing your tax report.

How do you calculate your tax savings on your RRSP contribution? The tax saved will be in line with your marginal tax rate (the % of tax paid on your last dollar earned). You can find your marginal tax rate on most big accounting firm websites. I particularly like Ernst & Young tax calculator.

Royal Bank (RY.TO)

10 Year dividend growth per share: 10.12%

Payout ratio: 46.91%

Canadian banks in general seem like a good pick for your RRSP this year. Their shares have suffered in 2015 along with the oil industry. While financial results still point towards the sky, most investors are now on the back foot and are waiting to see how bad things will go once oil companies starts to default on their loans (this wave hasn’t really started yet) and how Canadians will keep their homes if they lose their high paid jobs in the oil industry. This should affect important housing markets such as Edmonton and Calgary. A national economic slowdown could also affect other housing markets such as Vancouver and Toronto. With this premise in mind, I can appreciated that you are not fully hyped to buy RY or any other banks. However, you must think about the long haul; do you think RBC will outlive your retirement? I think so (and I’m only 34! hahaha!).

Royal Bank shows double digit dividend growth over the past 10 years (based on dividends paid per share, source Ycharts). Over the past few years, the bank has diversified its activities by adding more resources to their wealth management division along with their capital market segment. The great thing about the capital market division is that they usually make money no matter what happens on the market. The reason? A part of their strategy is based on volatility (market making) instead of investing for the future in a classic way. Therefore, as long as there are lots of transactions on the market, there is profit to be made.

Royal Bank has a strong balance sheet and will go through an eventual Canadian recession. This is a long term play in a very solid company.

Emera (EMA.TO)

10 Year dividend growth per share: 5.30%

Payout ratio: 70.71%

In Canada, when we talk about an “energy company” we often think about the oil & gas industry. While this sector has been struggling for the past 2 years, other sectors are doing well. This is the case with Emera evolving in electricity generation, transmission and distribution, gas transmission and other utility services. We aren’t lucky enough to have several utility companies in Canada (as compared to the US market), but Emera is definitely one of the great companies. The utility sector is a great one for dividend growth investors. Most companies benefit from a stable demand for their services and limited competition. This sounds like a perfect business model to insure dividend growth through time.

Emera has made several strong moves in the past couple of years. Its most recent was to diversify its activity by buying an American energy company in Florida (Teco) for $10.4 billion. The company is the leader in energy transportation in Nova Scotia and will also benefit from a new Maritime Link in 2017.

Emera is not a superpowered dividend growth stock compared to the other on my list. The past 10 years growth is more “reasonable” at 5% CAGR. However, I think EMA current projects and acquisitions will give an additional boost to its share price.

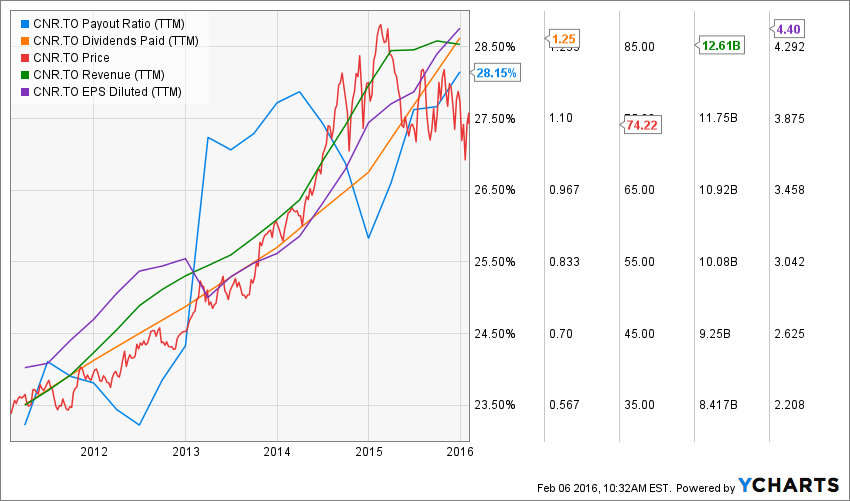

Canadian National Railway (CNR.TO)

10 Year dividend growth per share: 17.76%

Payout ratio: 27.67%

In general, the train business is synonymous with perpetual cash flow. In fact, the train sector is more like a fountain of cash flow where all you have to do is to get served. The railways are the most solid asset any transportation company could own. While it is also demanding on cash due to the high maintenance costs, there is virtually no direct competition once you own the railroad. At one point in time, such as now, oil prices are low enough that truck transportation may take a part of the train companies’ market share. However, over the long haul, everybody needs to ship their merchandise on trains.

Canadian National Railway owns an incredibly vast railway network accessing 75% of the US and Canadian population and serving all major markets. They own over 32,000 km of track and operate 80 warehouse to facilitate shipping across North America.

CNR shows great experience in transporting a wide variety of goods ranging from chemicals to intermodal wholesale goods. Since they serve 10 different sectors, there is always demands that will compensate for another sector slowdown.

The company increases its dividend easily by over 10% each year and shows a very low payout ratio. This shareholder friendly policy is there to last… maybe forever.

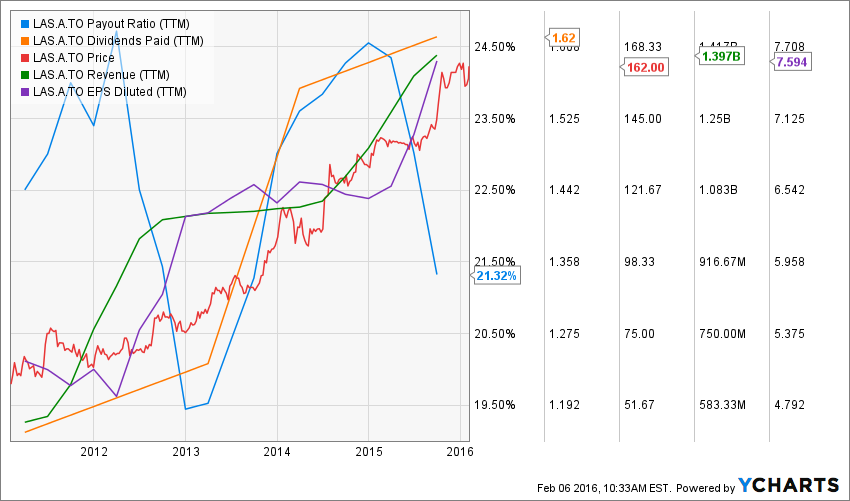

Lassonde Industries (LAS.A.TO)

10 Year dividend growth per share: 12.26%

Payout ratio: 21.32%

One thing I dislike about the Canadian market it is lack of great consumer companies. It is very rare to find companies increasing their dividends year after year in the consumer goods industry on this side of the border. I like the consumer sector as 60% of Canadian GDP and 71% of US GDP are coming from consumers. In other words; this is a cash flow rich sector.

This is why I was happy to take a look at Lassonde and appreciate its dividend growth potential. The company is a leader in the beverage industry in Canada and it is successfully entering the US market. Their most recent acquisitions (Apple & Eve’s) is a great mix with their current business model. On top of that, it helps the company manage its currency risk even better.

You may have noticed, but I didn’t discuss any dividend yield so far. Experienced investors will definitely tell me that both CRN and LAS.A are very low dividend yield stocks (usually around 1%, always below 2%). However, when you look at how strong their dividend growth is and how low their payout ratio remains, this tells you these companies will pay dividends forever. And this is what you are looking for when you invest in your retirement portfolio; stability and certainty. These companies meet both criteria.

How to build a Strong Retirement Portfolio

I agree with you, buying 4 stocks won’t build a strong retirement portfolio. There are several hours required to follow the market, analyze existing holdings and updating your watch list.

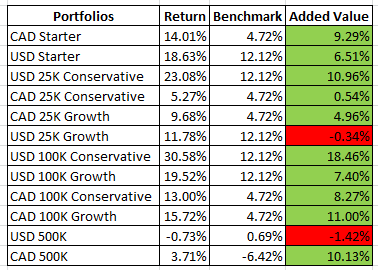

I’ve been working very hard on my dividend growth investing platform Dividend Stocks Rock and our portfolio models prove that we done a great job in building rock solid retirement portfolios. Here are our portfolio returns since October 31st 2013 (results don’t include dividends, as at February 5th 2016):

as you can see, we beat our benchmark (XDV and VIG) for 10 out of 12 portfolios while going through a bearish market. This is the type of portfolio you want for your retirement ;-).

disclaimer: We own RY.TO, EMA.TO, CNR.TO and LAS.A.TO in our Dividend Stocks Rock Porfolios. I personally own RY.TO, EMA.TO and CNR.TO